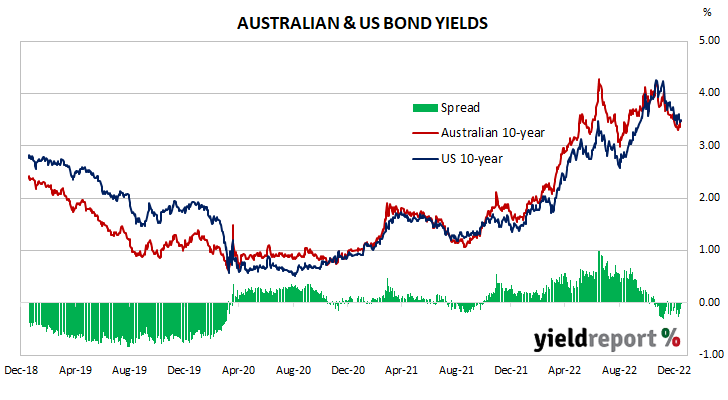

Summary: Bond yields lower in Australia; ACGB 10-year spread to US Treasury yield rose from -28bps to -2bps; 10-year bond yields drop slightly in US while increased in major European markets.

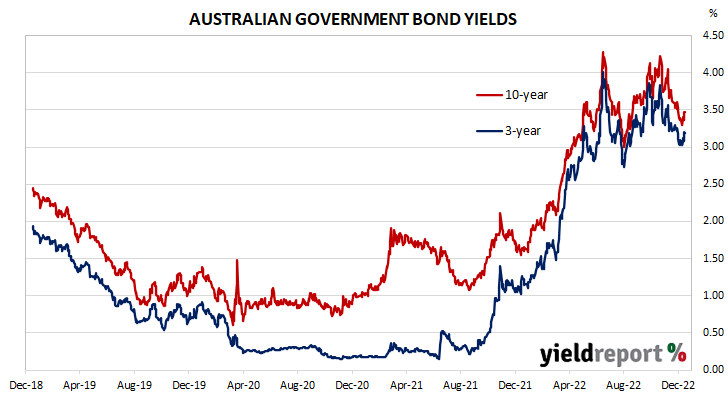

By the end of the week, the 3-year ACGB yield had rose 16bp to 3.19%, the 10-year yield had increased 17bps to 3.47% while the 20-year yield finished 21bps higher at 3.82%.

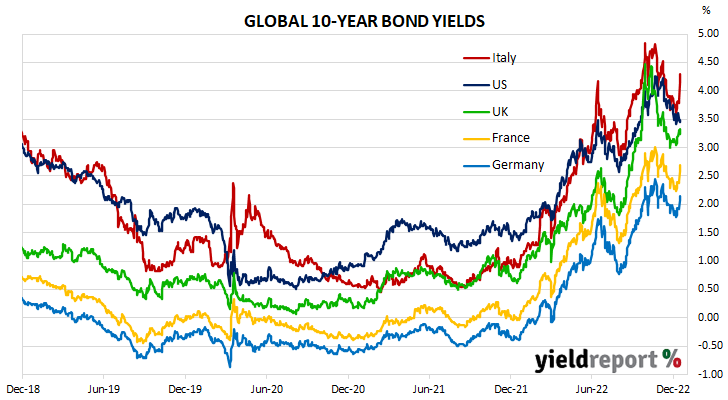

Over in the US, 10-year bond yields rose a touch on Monday, then fell for the rest of the week until a small rebound on Friday.

By this point, the US 2-year Treasury bond yield had dropped 16bps to 4.20%, the 10-year yield had decreased 9bps to 3.49% while the 30-year yield finished 2bp lower at 3.54%.

In major euro-zone markets, 10-year bond yields see-sawed through the week but the rises were larger in magnitude than the falls.

By the end of the week the German 10-year bund yield had added 29bps to 2.15% and the French 10-year OAT yield had gained 30bps to 2.69%. The Italian 10-year BTP yield added substantial 50bps over the week to 4.30% while the British 10-year gilt yield finished 15bps higher at 3.33%.

AUSTRALIAN GOVERNMENT BONDS

| MATURITY | COUPON (%) | ISSUE SIZE ($M) | CLOSING YIELD | Δ WEEK | Δ MONTH | WEEK HIGH | WEEK LOW |

|---|---|---|---|---|---|---|---|

| 21-Apr-23 | 5.50 | 34,200 | 3.15 | 0.02 | -0.06 | 3.16 | 3.14 |

| 21-Apr-24 | 2.75 | 35,900 | 3.15 | 0.08 | -0.14 | 3.16 | 3.09 |

| 21-Nov-24 | 0.25 | 41,300 | 3.13 | 0.09 | -0.25 | 3.14 | 3.08 |

| 21-Apr-25 | 3.25 | 41,500 | 3.11 | 0.13 | -0.30 | 3.12 | 3.02 |

| 21-Nov-25 | 0.25 | 38,700 | 3.13 | 0.12 | -0.33 | 3.15 | 3.06 |

| 21-Apr-26 | 4.25 | 38,100 | 3.17 | 0.12 | -0.32 | 3.18 | 3.10 |

| 21-Sep-26 | 0.50 | 37,300 | 3.19 | 0.12 | -0.34 | 3.21 | 3.13 |

| 21-Apr-27 | 4.75 | 36,700 | 3.21 | 0.12 | -0.36 | 3.23 | 3.15 |

| 21-Nov-27 | 2.75 | 31,400 | 3.23 | 0.12 | -0.39 | 3.25 | 3.18 |

| 21-May-28 | 2.25 | 29,700 | 3.25 | 0.12 | -0.41 | 3.27 | 3.20 |

| 21-Nov-28 | 2.75 | 34,100 | 3.28 | 0.13 | -0.43 | 3.29 | 3.22 |

| 21-Apr-29 | 3.25 | 34,500 | 3.31 | 0.14 | -0.43 | 3.31 | 3.23 |

| 21-Nov-29 | 2.75 | 34,100 | 3.34 | 0.14 | -0.44 | 3.34 | 3.26 |

| 21-May-30 | 2.50 | 37,100 | 3.37 | 0.15 | -0.45 | 3.37 | 3.29 |

| 21-Dec-30 | 1.00 | 38,700 | 3.41 | 0.15 | -0.45 | 3.41 | 3.32 |

| 21-Jun-31 | 1.50 | 38,100 | 3.42 | 0.16 | -0.45 | 3.43 | 3.34 |

| 21-Nov-31 | 1.00 | 21,000 | 3.44 | 0.16 | -0.46 | 3.44 | 3.35 |

| 21-May-32 | 1.25 | 39,300 | 3.44 | 0.16 | -0.46 | 3.44 | 3.35 |

| 21-Nov-32 | 1.75 | 27,800 | 3.45 | 0.16 | -0.47 | 3.46 | 3.36 |

| 21-Apr-33 | 4.50 | 22,900 | 3.46 | 0.16 | -0.47 | 3.46 | 3.37 |

| 21-Nov-33 | 3.00 | 19,400 | 3.49 | 0.16 | -0.48 | 3.49 | 3.40 |

| 21-Jun-35 | 2.75 | 9,550 | 3.61 | 0.17 | -0.47 | 3.61 | 3.51 |

| 21-Apr-37 | 3.75 | 12,300 | 3.69 | 0.18 | -0.47 | 3.70 | 3.60 |

| 21-Jun-39 | 3.25 | 10,300 | 3.76 | 0.18 | -0.48 | 3.78 | 3.68 |

| 21-May-41 | 2.75 | 13,500 | 3.81 | 0.18 | -0.49 | 3.84 | 3.73 |

| 21-Mar-47 | 3.00 | 13,900 | 3.83 | 0.20 | -0.46 | 3.87 | 3.75 |

| 21-Jun-51 | 1.75 | 18,700 | 3.78 | 0.18 | -0.47 | 3.82 | 3.70 |