Summary: Bond yields mostly lower in Australia; ACGB 10-year spread to US Treasury yield rises from -22bps to -11bps; 10-year bond yields down in US, major European markets; AOFM issues $4.25 billion worth of bonds, notes.

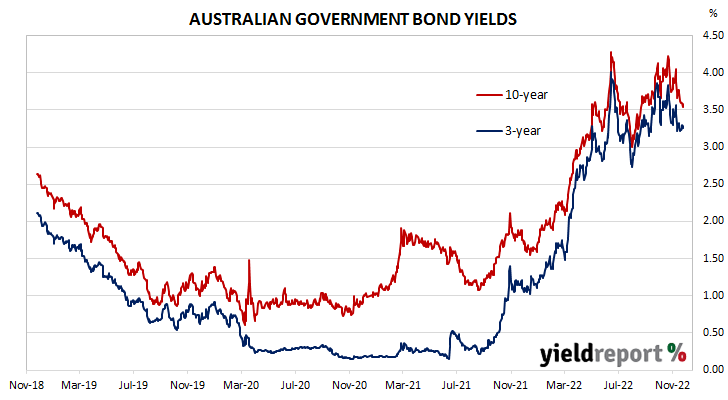

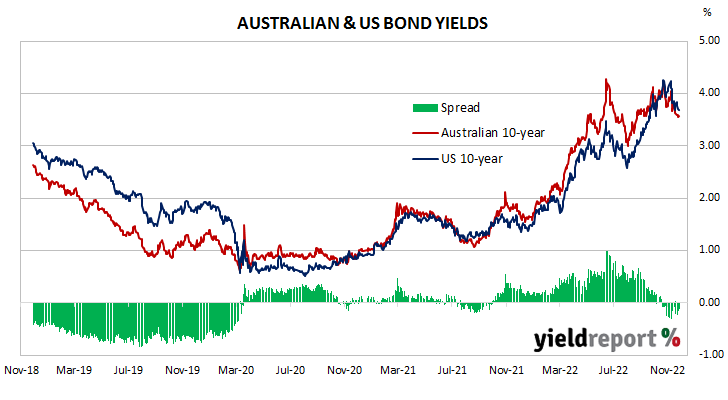

Locally, long-term ACGB yields fell modestly on Monday and then trend lower through the remainder of the week. By the end of the week, the 3-year ACGB yield had added 4bps to 3.28%, the 10-year yield had lost 3bps to 3.58% while the 20-year yield finished 9bps lower at 3.96%. The spread between US and Australian 10-year Treasury bond yields “widened” from -22bps to -11bps.

Over in the US, 10-year bond yields rose a touch on Monday and then fell over the remainder of the shortened week.

The Atlanta Fed’s Nowcast model was updated midweek. The December quarter GDP growth estimate was raised to 4.3% annualised, or a 1.1% expansion over the quarter.

S&P Global Market Intelligence’s latest flash reading of its composite index was also released, with the index falling from October’s final reading of 48.2 to 46.3. The manufacturing index decreased from 50.4 to 47.6 and the services index lost 1.7 points to 46.1. S&P Global’s Chris Williamson said, “output and demand [are] falling at increased rates, consistent with the economy contracting at an annualised rate of 1%.”

The minutes from the FOMC’s last meeting were released a day later. The general reaction seemed to be that the minutes suggest the FOMC is close to reducing the pace of increases.

By the end of the week, the US 2-year Treasury bond yield had lost 3bps to 4.48%, the 10-year yield had shed 14bps to 3.69% while the 30-year yield finished 18bps lower at 3.74%.

In major euro-zone markets, 10-year bond yields fell through the week until Friday when they shot up noticeably.

The results of November’s consumer sentiment survey were released on Tuesday and they indicated euro-zone sentiment had improved for a second consecutive month. However, the index is still well below the long-term average.

Germany’s ifo Institute released the November reading of its business climate index on Thursday. The index improved albeit to a still-depressed level. German firms’ views of current conditions declined a little while the short-term outlook improved.

The minutes of the ECB’s October meeting were published the same day. They provided no surprises and economists expect another 75bps increase in December.

By the end of the week, the German 10-year bund yield had lost 4bps to 1.97% and the French 10-year OAT yield had shed 5bps to 2.43%. The Italian 10-year BTP yield lost 4bps over the week to 3.85% while the British 10-year gilt yield finished 12bps lower at 3.12%.

The AOFM held two vanilla bond tenders during the week, plus an index-linked bond (ILB) tender. $900 million of May 2032s and $700 million of April 2029s were priced at yields of 3.53% and 3.17% respectively while $150 million of September 2030 ILBs were priced with a real yield of 1.17%. There were also three Treasury note tenders which raised a total of $2.5 billion on a short-term basis.

The gross value of all bonds issued by the AOFM in the 2022/2023 financial year-to-date (not taking into account buy-backs or short-term Treasury note tenders) is $43.25 billion. There are currently $821.65 billion of Treasury bonds and $38.086 billion of Treasury index-linked bonds on issue. The next series to mature does so on 21 April 2023 when $34.20 billion worth of bonds are due. There are also $27.00 billion of short-term Treasury notes currently outstanding.

AUSTRALIAN GOVERNMENT BONDS

| MATURITY | COUPON (%) | ISSUE SIZE ($M) | CLOSING YIELD | Δ WEEK | Δ MONTH | WEEK HIGH | WEEK LOW |

|---|---|---|---|---|---|---|---|

| 21-Apr-23 | 5.50 | 34,200 | 3.11 | 0.01 | -0.12 | 3.12 | 3.08 |

| 21-Apr-24 | 2.75 | 35,900 | 3.26 | 0.15 | -0.20 | 3.26 | 3.10 |

| 21-Nov-24 | 0.25 | 41,300 | 3.22 | 0.10 | -0.43 | 3.22 | 3.11 |

| 21-Apr-25 | 3.25 | 40,800 | 3.26 | 0.13 | -0.41 | 3.26 | 3.13 |

| 21-Nov-25 | 0.25 | 38,000 | 3.30 | 0.10 | -0.45 | 3.30 | 3.20 |

| 21-Apr-26 | 4.25 | 38,100 | 3.33 | 0.08 | -0.46 | 3.33 | 3.24 |

| 21-Sep-26 | 0.50 | 36,700 | 3.34 | 0.06 | -0.49 | 3.34 | 3.28 |

| 21-Apr-27 | 4.75 | 36,700 | 3.36 | 0.05 | -0.50 | 3.36 | 3.30 |

| 21-Nov-27 | 2.75 | 31,400 | 3.38 | 0.03 | -0.54 | 3.38 | 3.34 |

| 21-May-28 | 2.25 | 29,700 | 3.40 | 0.01 | -0.55 | 3.40 | 3.36 |

| 21-Nov-28 | 2.75 | 34,100 | 3.42 | 0.01 | -0.57 | 3.43 | 3.39 |

| 21-Apr-29 | 3.25 | 34,500 | 3.44 | 0.00 | -0.58 | 3.45 | 3.41 |

| 21-Nov-29 | 2.75 | 34,100 | 3.47 | -0.02 | -0.60 | 3.48 | 3.44 |

| 21-May-30 | 2.50 | 37,100 | 3.49 | -0.03 | -0.61 | 3.50 | 3.46 |

| 21-Dec-30 | 1.00 | 38,700 | 3.53 | -0.02 | -0.61 | 3.54 | 3.50 |

| 21-Jun-31 | 1.50 | 38,100 | 3.55 | -0.02 | -0.61 | 3.56 | 3.51 |

| 21-Nov-31 | 1.00 | 21,000 | 3.58 | -0.01 | -0.60 | 3.58 | 3.52 |

| 21-May-32 | 1.25 | 39,300 | 3.60 | 0.01 | -0.58 | 3.60 | 3.53 |

| 21-Nov-32 | 1.75 | 27,800 | 3.63 | 0.01 | -0.57 | 3.63 | 3.54 |

| 21-Apr-33 | 4.50 | 22,200 | 3.62 | 0.01 | -0.57 | 3.62 | 3.55 |

| 21-Nov-33 | 3.00 | 18,500 | 3.66 | 0.01 | -0.58 | 3.66 | 3.58 |

| 21-Jun-35 | 2.75 | 9,550 | 3.73 | -0.04 | -0.61 | 3.74 | 3.70 |

| 21-Apr-37 | 3.75 | 12,300 | 3.78 | -0.10 | -0.64 | 3.85 | 3.78 |

| 21-Jun-39 | 3.25 | 10,300 | 3.84 | -0.15 | -0.65 | 3.96 | 3.84 |

| 21-May-41 | 2.75 | 13,500 | 3.89 | -0.17 | -0.64 | 4.02 | 3.89 |

| 21-Mar-47 | 3.00 | 13,600 | 3.97 | -0.09 | -0.54 | 4.01 | 3.94 |

| 21-Jun-51 | 1.75 | 18,700 | 4.04 | 0.02 | -0.44 | 4.04 | 3.90 |