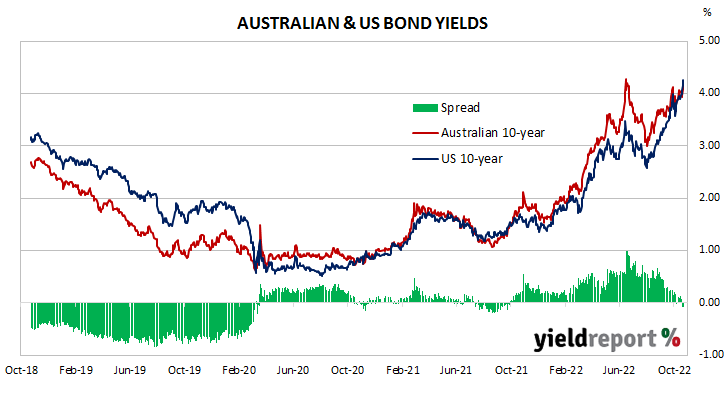

Summary: Bond yields higher in Australia; ACGB 10-year spread to US Treasury yield tightens from +13bps to -3bps; 10-year bond yields up in US, major European markets; AOFM issues $3.5 billion worth of bonds, notes.

Locally, long-term ACGB yields rose through much of the week except for a pullback on Tuesday. By the end of the week, the 3-year ACGB yield had gained 21bps to 3.83%, the 10-year yield had added 19bps to 4.22% while the 20-year yield finished 22bps higher at 4.53%. The spread between US and Australian 10-year Treasury bond yields tightened from +13bps to -3bps.

Over in the US, 10-year bond yields rose consistently over the week and ran up noticeably towards the end of it.

Industrial production numbers for September were released on Tuesday. There was an increase of 0.4%, in contrast with the expected 0.1%% decline. This latest reading implied an annual GDP growth rate of 4.2%.

The Conference Board’s September reading of its Leading Index came out the next day. The figure again undershot expectations and it marks the seventh consecutive monthly fall.

One of the two major measures of US consumer sentiment, the University of Michigan’s Consumer sentiment index was published at the end of the week. The index improved a little further again, rising from September’s final reading of 58.6 to 59.8, still well below its long-term average.

The Atlanta Fed’s Nowcast model was updated at the end of the week. The September quarter GDP growth estimate was raised to 2.8% annualised, or a 0.7% expansion over the quarter.

By this point, the US 2-year Treasury bond yield had gained 19bps to 4.61%, the 10-year yield had added 35bps to 4.25% while the 30-year yield finished 39bps higher at 4.27%.

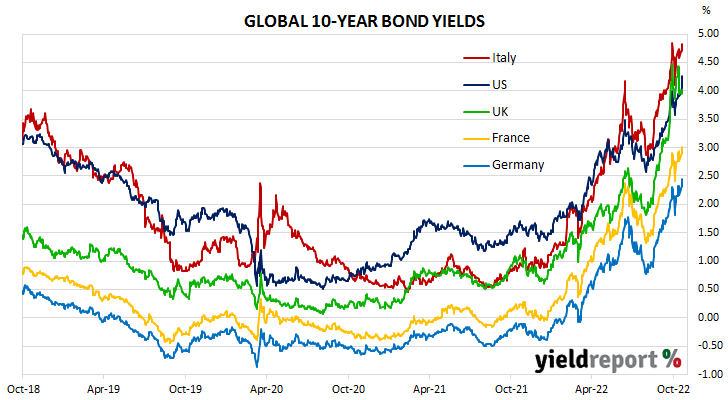

In major euro-zone markets, 10-year bond yields followed similar paths to their US counterpart, rising consisntly through the week.

On Tuesday night (AEST), Germany’s ZEW October survey indicated its Economic Sentiment index rose from September’s reading of -61.9 to -59.2, higher than the -66.5 which had been generally expected. However, ZEW’s current conditions index fell from -60.5 to -72.2. “Despite the slight rise in expectations, the economic outlook for Germany has thus deteriorated significantly.”

The results of October’s consumer sentiment survey were released on Friday and they indicated euro-zone sentiment had bounced off its post-GFC low, rising by 1.2 points to -27.6 points. The long-term average reading is -11.8 points.

By this stage, the German 10-year bund yield gained 28bps to 2.45% and the French 10-year OAT yield had added 25bps to 3.02%y. The Italian 10-year BTP yield also increased by 25bps to 4.82% while the British 10-year gilt yield finished 5bps higher at 3.99%.

The AOFM held two vanilla bond tenders during the week. $800 million of April 2029s and $700 million of April 2025s were priced at yields of 3.74% and 3.61% respectively. There were also three Treasury note tenders which raised a total of $2.0 billion on a short-term basis.

The gross value of all bonds issued by the AOFM in the 2022/2023 financial year-to-date (not taking into account buy-backs or short-term Treasury note tenders) is $23.85 billion. There are currently $829.05 billion of Treasury bonds and $37.786 billion of Treasury index-linked bonds on issue. The next series to mature does so on 21 November when $26.50 billion worth of bonds are due. There are also $25.00 billion of short-term Treasury notes currently outstanding after $4 billion matured on Friday.

AUSTRALIAN GOVERNMENT BONDS

| MATURITY | COUPON (%) | ISSUE SIZE ($M) | CLOSING YIELD | Δ WEEK | Δ MONTH | WEEK HIGH | WEEK LOW |

|---|---|---|---|---|---|---|---|

| 21-Nov-22 | 2.25 | 26,500 | 2.75 | 0.06 | 0.11 | 2.79 | 2.69 |

| 21-Apr-23 | 5.50 | 34,200 | 3.23 | 0.17 | 0.20 | 3.23 | 3.08 |

| 21-Apr-24 | 2.75 | 35,900 | 3.46 | 0.29 | 0.27 | 3.46 | 3.14 |

| 21-Nov-24 | 0.25 | 41,300 | 3.65 | 0.26 | 0.31 | 3.65 | 3.32 |

| 21-Apr-25 | 3.25 | 40,800 | 3.67 | 0.21 | 0.27 | 3.67 | 3.38 |

| 21-Nov-25 | 0.25 | 38,000 | 3.76 | 0.21 | 0.30 | 3.76 | 3.46 |

| 21-Apr-26 | 4.25 | 38,100 | 3.79 | 0.22 | 0.31 | 3.79 | 3.49 |

| 21-Sep-26 | 0.50 | 36,700 | 3.83 | 0.22 | 0.34 | 3.83 | 3.53 |

| 21-Apr-27 | 4.75 | 36,700 | 3.86 | 0.22 | 0.36 | 3.86 | 3.56 |

| 21-Nov-27 | 2.75 | 31,400 | 3.92 | 0.22 | 0.38 | 3.92 | 3.61 |

| 21-May-28 | 2.25 | 29,700 | 3.95 | 0.21 | 0.40 | 3.95 | 3.66 |

| 21-Nov-28 | 2.75 | 33,300 | 3.99 | 0.20 | 0.42 | 3.99 | 3.70 |

| 21-Apr-29 | 3.25 | 34,500 | 4.02 | 0.20 | 0.43 | 4.02 | 3.73 |

| 21-Nov-29 | 2.75 | 33,400 | 4.07 | 0.20 | 0.44 | 4.07 | 3.78 |

| 21-May-30 | 2.50 | 37,100 | 4.10 | 0.19 | 0.45 | 4.10 | 3.82 |

| 21-Dec-30 | 1.00 | 38,700 | 4.14 | 0.19 | 0.46 | 4.14 | 3.86 |

| 21-Jun-31 | 1.50 | 38,100 | 4.16 | 0.19 | 0.46 | 4.16 | 3.88 |

| 21-Nov-31 | 1.00 | 21,000 | 4.18 | 0.19 | 0.47 | 4.18 | 3.90 |

| 21-May-32 | 1.25 | 38,400 | 4.18 | 0.19 | 0.46 | 4.18 | 3.90 |

| 21-Nov-32 | 1.75 | 27,000 | 4.20 | 0.19 | 0.46 | 4.20 | 3.92 |

| 21-Apr-33 | 4.50 | 22,200 | 4.20 | 0.19 | 0.46 | 4.20 | 3.92 |

| 21-Nov-22 | 3.00 | 17,600 | 4.24 | 0.19 | 0.47 | 4.24 | 3.96 |

| 21-Jun-35 | 2.75 | 9,550 | 4.34 | 0.20 | 0.49 | 4.34 | 4.06 |

| 21-Apr-37 | 3.75 | 12,300 | 4.42 | 0.20 | 0.50 | 4.42 | 4.14 |

| 21-Jun-39 | 3.25 | 10,300 | 4.49 | 0.20 | 0.52 | 4.49 | 4.22 |

| 21-May-41 | 2.75 | 13,500 | 4.53 | 0.21 | 0.53 | 4.53 | 4.26 |

| 21-Mar-47 | 3.00 | 13,600 | 4.51 | 0.21 | 0.50 | 4.51 | 4.25 |

| 21-Jun-51 | 1.75 | 18,400 | 4.48 | 0.21 | 0.49 | 4.48 | 4.21 |