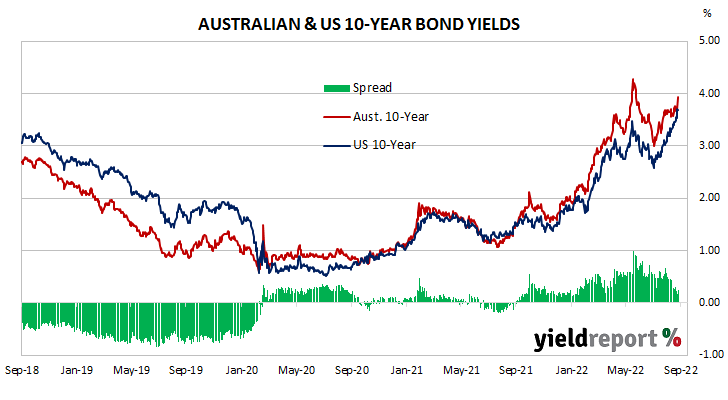

Summary: Bond yields higher in Australia; ACGB 10-year spread to US Treasury yield narrows from +31bps to +25bps; 10-year bond yields up in US, major European markets; AOFM issues $1.5 billion worth of bonds.

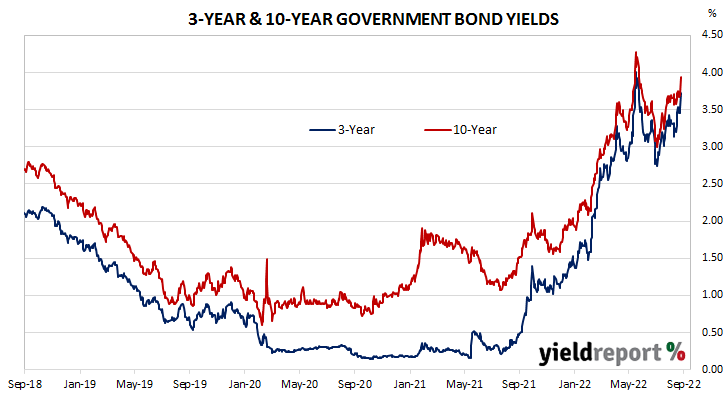

Locally, long-term ACGB yields declined over the first two days of the week before reversing course midweek and then jumping by an unusually large amount on Friday. By this point, 3-year and 10-year ACGB yields had both gained 18bps to 3.72% and 3.94% while the 20-year yield finished 14bps higher at 4.16%. The spread between US and Australian 10-year Treasury bond yields narrowed from +31bps to +25bps.

Over in the US, long-term bond yields increased for the first couple of days, declined modestly midweek, then jumped on Thursday before pulling back a little at the end of the week.

The Atlanta Fed’s Nowcast model was updated on Tuesday. The September quarter GDP growth estimate was lowered to 0.3% annualised, or a 0.1% expansion over the quarter.

The FOMC’s two-day meeting ended on Wednesday and another 75bps increase to its target range for the federal funds rate was announced. Again, the decision was in line with expectations and more increases are expected.

The Conference Board’s August reading of its Leading Index came out the next day. The figure undershot expectations again and it marks the sixth consecutive monthly fall.

IHS Markit’s latest flash reading of its composite index was released at the end of the week, with the index rising from August’s final reading of 44.6 to 49.3. The manufacturing index increased from 43.7 to 49.2 and the services index gained 0.3 points to 51.8. S&P Global’s Chris Williamson noted order books were “returning to modest growth, allaying some concerns about the depth of the current downturn.”

By this point, the US 2-year Treasury bond yield had gained 35bps to 4.21%, the 10-year yield had increased by 24bps to 3.69% while the 30-year yield finished 9bps higher at 3.61%.

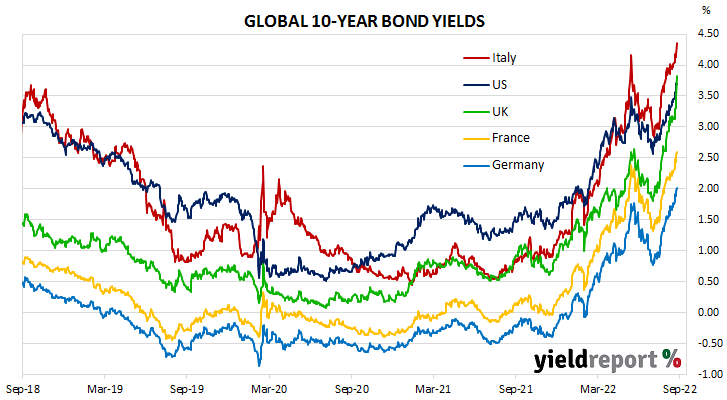

In major euro-zone markets, 10-year bond yields rose through the week with the exception of Wednesday when yield declined moderately.

There was not much in the way of notable data until Thursday when the results of September’s consumer sentiment survey were released. Unsurprisingly, they indicated euro-zone sentiment had hit a new post-GFC low.

The Bank of England raised its Bank Rate by 50bps on the same day. It also announced it would begin selling its bond holdings from early October.

S&P Global Market Intelligence released its September flash PMI figures for the euro-zone at the end of the week. The preliminary reading of the composite index was 48.9, down from August’s final reading of 49.2. S&P Global’s Chris Williamson said “…the survey’s forward-looking indicators point to a steepening economic decline for the euro-zone in the fourth quarter, adding to the likelihood of the region falling into recession.”

By this stage, the German 10-year bund yield had gained 27bps to 2.02% while the French 10-year OAT yield had added 29bps to 2.60%. The Italian 10-year BTP yield increased by 32bps to 4.35% over the week while the British 10-year gilt yield finished 69bps higher at 3.82%.

The AOFM held two bond tenders during the week. $700 million of September 2026s and $800 million of April 2033s were priced at yields of 3.46% and 3.73%. There were no Treasury note tenders.

The gross value of all bonds issued by the AOFM in the 2022/2023 financial year-to-date (not taking into account buy-backs or short-term Treasury note tenders) is $17.65 billion. There are currently $823.05 billion of Treasury bonds and $37.586 billion of Treasury index-linked bonds on issue. The next series to mature does so on 21 November when $26.50 billion worth of bonds are due. There are also $24.00 billion of short-term Treasury notes currently outstanding after $2.5 billion matured on Friday.

AUSTRALIAN GOVERNMENT BONDS

| MATURITY | COUPON (%) | ISSUE SIZE ($M) | CLOSING YIELD | Δ WEEK | Δ MONTH |

|---|---|---|---|---|---|

| 21-Nov-22 | 2.25 | 26,500 | 2.90 | 0.26 | 0.62 |

| 21-Apr-23 | 5.50 | 34,200 | 3.17 | 0.15 | 0.43 |

| 21-Apr-24 | 2.75 | 35,900 | 3.37 | 0.18 | 0.49 |

| 21-Nov-24 | 0.25 | 41,300 | 3.52 | 0.18 | 0.53 |

| 21-Apr-25 | 3.25 | 40,100 | 3.59 | 0.18 | 0.49 |

| 21-Nov-25 | 0.25 | 37,300 | 3.65 | 0.19 | 0.51 |

| 21-Apr-26 | 4.25 | 38,100 | 3.66 | 0.18 | 0.51 |

| 21-Sep-26 | 0.50 | 36,700 | 3.68 | 0.18 | 0.50 |

| 21-Apr-27 | 4.75 | 36,000 | 3.69 | 0.19 | 0.51 |

| 21-Nov-27 | 2.75 | 31,400 | 3.73 | 0.19 | 0.51 |

| 21-May-28 | 2.25 | 29,700 | 3.75 | 0.20 | 0.52 |

| 21-Nov-28 | 2.75 | 32,600 | 3.77 | 0.20 | 0.52 |

| 21-Apr-29 | 3.25 | 33,700 | 3.79 | 0.20 | 0.52 |

| 21-Nov-29 | 2.75 | 33,400 | 3.82 | 0.20 | 0.51 |

| 21-May-30 | 2.50 | 37,100 | 3.84 | 0.20 | 0.51 |

| 21-Dec-30 | 1.00 | 38,700 | 3.88 | 0.20 | 0.52 |

| 21-Jun-31 | 1.50 | 38,100 | 3.90 | 0.20 | 0.51 |

| 21-Nov-31 | 1.00 | 21,000 | 3.91 | 0.20 | 0.51 |

| 21-May-32 | 1.25 | 37,600 | 3.91 | 0.19 | 0.51 |

| 21-Nov-32 | 1.75 | 26,200 | 3.92 | 0.19 | 3.92 |

| 21-Apr-33 | 4.50 | 22,200 | 3.92 | 0.19 | 0.50 |

| 21-Nov-22 | 3.00 | 16,800 | 3.95 | 0.19 | 3.95 |

| 21-Jun-35 | 2.75 | 9,550 | 4.04 | 0.18 | 0.49 |

| 21-Apr-37 | 3.75 | 12,300 | 4.09 | 0.17 | 0.45 |

| 21-Jun-39 | 3.25 | 10,300 | 4.13 | 0.16 | 0.41 |

| 21-May-41 | 2.75 | 13,500 | 4.15 | 0.15 | 0.39 |

| 21-Mar-47 | 3.00 | 13,600 | 4.14 | 0.13 | 0.35 |

| 21-Jun-51 | 1.75 | 18,400 | 4.10 | 0.12 | 0.33 |