Summary: Bond yields lower in Australia; ACGB 10-year spread to US Treasury yield tightens from +46bps to +29bps; 10-year bond yields up in US, major European markets; AOFM issues $3.1 billion worth of bonds, notes.

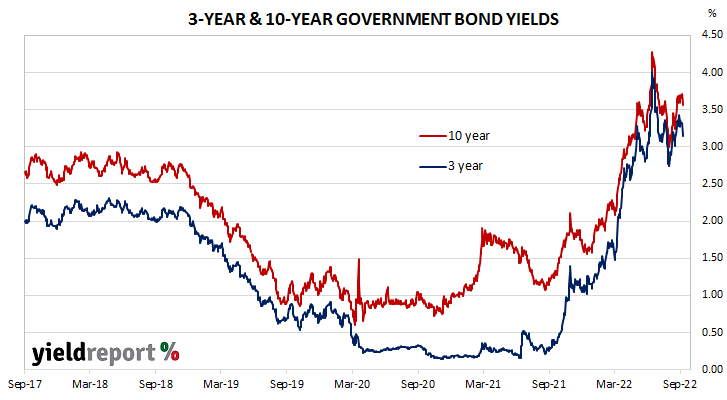

Locally, long-term ACGB yields again started the week with little change until Wednesday. There was a substantial fall on Thursday after RBA chief Lowe gave his annual speech to the Anika Foundation which was then followed by a quiet day on Friday. By this point, the 3-year ACGB yield had shed 15bps to 3.17%, the 10-year yield had lost 9bps to 3.57% while the 20-year yield finished 3bps lower at 3.87%. The spread between US and Australian 10-year Treasury bond yields tightened from +46bps to +29bps.

Over in the US, long-term bond yields increased through most of the shortened week with the exception of a moderate fall on Thursday.

About the only report of note was the release of the ISM’s August Services PMI on Tuesday. The index increased from 56.7 to 56.9, above the generally expected figure of 55.2.

The Atlanta Fed’s Nowcast model was updated again on Friday. The September quarter GDP growth estimate was lowered to 1.3% annualised, or a 0.3% expansion over the quarter.

By this point, the US 2-year Treasury bond yield had gained 7bps to 3.47%, the 10-year yield had increased by 8bps to 3.28% while the 30-year yield finished 10bps higher at 3.45%.

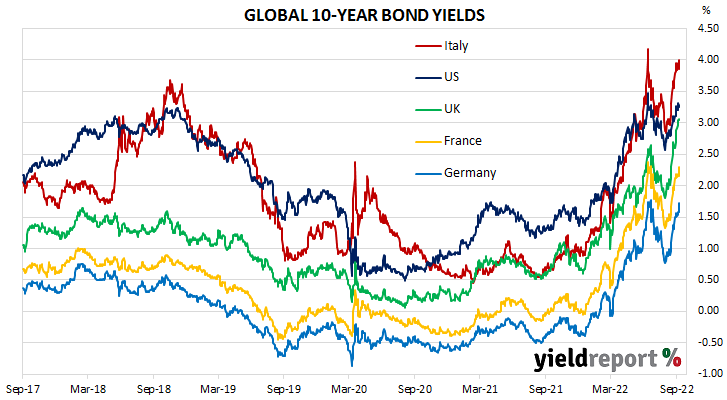

In major euro-zone markets, 10-year bond yields took a different path to their US counterparts, with modest changes each day until Friday when yields jumped.

There were no particularly notable reports during the week, although the ECB had a policy meeting on Thursday. As expected, the ECB raised its three policy rates, all by 75bps.

By the end of the week, the German 10-year bund yield had gained 18bps to 1.70% while the French 10-year OAT yield had added 12bps to 2.26%. The Italian 10-year BTP yield increased by 18bps to 4.01% over the week while the British 10-year gilt yield finished 18bps higher at 3.09%.

The AOFM held two bond tenders during the week. $300 million of June 2051s and $800 million of April 2033s were priced at yields of 3.90% and 3.74% respectively. There were also three Treasury note tenders which raised $2.0 billion on a short-term basis.

The gross value of all bonds issued by the AOFM in the 2022/2023 financial year-to-date (not taking into account buy-backs or short-term Treasury note tenders) is $15.25 billion. There are currently $820.75 billion of Treasury bonds and $37.486 billion of Treasury index-linked bonds on issue. The next series to mature does so on 21 November when $26.50 billion worth of bonds are due. There are also $25.00 billion of short-term Treasury notes currently outstanding after $4 billion matured on Friday.

| MATURITY | COUPON (%) | ISSUE SIZE ($M) | CLOSING YIELD | Δ WEEK | Δ MONTH |

|---|---|---|---|---|---|

| 21-Nov-22 | 2.25 | 26,500 | 2.45 | 0.03 | 0.17 |

| 21-Apr-23 | 5.50 | 34,200 | 2.82 | 0.04 | 0.20 |

| 21-Apr-24 | 2.75 | 35,900 | 2.93 | -0.09 | 0.31 |

| 21-Nov-24 | 0.25 | 41,300 | 3.05 | -0.09 | 0.32 |

| 21-Apr-25 | 3.25 | 40,100 | 3.12 | -0.13 | 0.31 |

| 21-Nov-25 | 0.25 | 37,300 | 3.18 | -0.15 | 0.32 |

| 21-Apr-26 | 4.25 | 38,100 | 3.19 | -0.14 | 0.33 |

| 21-Sep-26 | 0.50 | 36,000 | 3.22 | -0.12 | 0.35 |

| 21-Apr-27 | 4.75 | 36,000 | 3.24 | -0.12 | 0.36 |

| 21-Nov-27 | 2.75 | 31,400 | 3.29 | -0.12 | 0.38 |

| 21-May-28 | 2.25 | 29,700 | 3.32 | -0.12 | 0.39 |

| 21-Nov-28 | 2.75 | 32,600 | 3.35 | -0.12 | 0.40 |

| 21-Apr-29 | 3.25 | 33,700 | 3.39 | -0.11 | 0.42 |

| 21-Nov-29 | 2.75 | 33,400 | 3.43 | -0.11 | 0.43 |

| 21-May-30 | 2.50 | 37,100 | 3.47 | -0.10 | 0.44 |

| 21-Dec-30 | 1.00 | 38,700 | 3.51 | -0.10 | 0.45 |

| 21-Jun-31 | 1.50 | 38,100 | 3.53 | -0.09 | 0.46 |

| 21-Nov-31 | 1.00 | 21,000 | 3.55 | -0.09 | 0.47 |

| 21-May-32 | 1.25 | 36,800 | 3.56 | -0.09 | 0.48 |

| 21-Nov-32 | 1.75 | 26,200 | 3.57 | -0.09 | 3.57 |

| 21-Apr-33 | 4.50 | 21,400 | 3.58 | -0.09 | 0.47 |

| 21-Nov-22 | 3.00 | 16,800 | 3.61 | -0.08 | 3.61 |

| 21-Jun-35 | 2.75 | 9,550 | 3.71 | -0.08 | 0.48 |

| 21-Apr-37 | 3.75 | 12,300 | 3.77 | -0.08 | 0.47 |

| 21-Jun-39 | 3.25 | 10,300 | 3.83 | -0.08 | 0.45 |

| 21-May-41 | 2.75 | 13,500 | 3.87 | -0.07 | 0.41 |

| 21-Mar-47 | 3.00 | 13,600 | 3.87 | -0.06 | 0.39 |

| 21-Jun-51 | 1.75 | 18,400 | 3.83 | -0.05 | 0.37 |