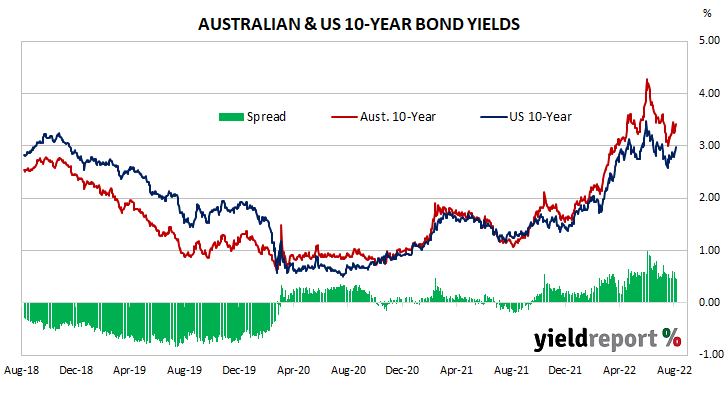

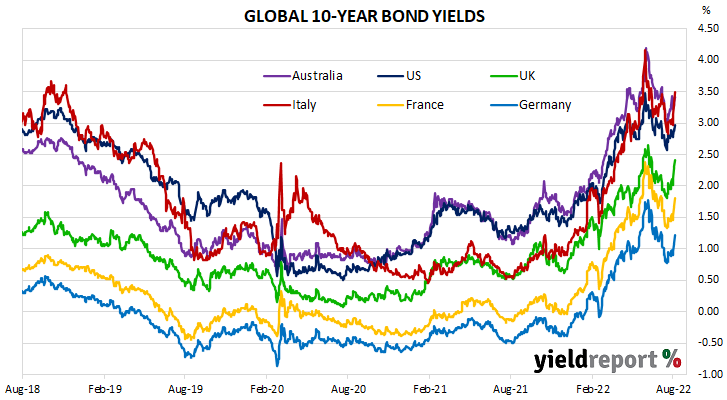

Summary: Bond yields down modestly in Australia; ACGB 10-year spread to US Treasury yield tightens from +62bps to +45bps; 10-year bond yields up in US, major European markets; AOFM issues $4.0 billion worth of bonds, notes.

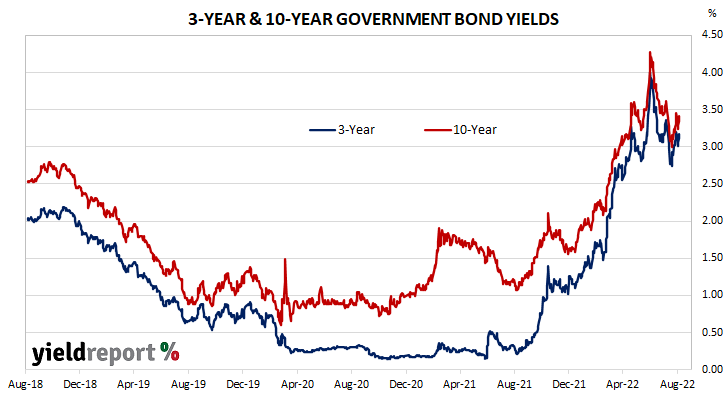

Locally, long-term ACGB yields started the week with a moderate fall which was then followed by a large drop on Tuesday. However, yields then rose through the remainder of the week. By the end of it, the 3-year ACGB yield had shed 2bps to 3.17% while 10-year and 20-year yield each finished 3bps lower at 3.42% and 3.77% respectively. The spread between US and Australian 10-year Treasury bond yields tightened from +62bps to +45bps.

Over in the US, long-term bond yields fell moderately at the start of the week before reversing course on Tuesday and rising noticeably midweek. A modest decline on Thursday was followed by another noticeable rise at the end of the week.

The first notable US economic report was released by the US Fed on Tuesday night (AEST). US industrial production numbers for July posted a 0.6% expansion, double the 0.3% expected. The latest reading implied an annual GDP growth rate of 3.6%.

The next day, July’s retail sales report indicated total sales remained flat over the month, slightly less than the expected 0.1%. Lower sales of vehicles and fuel were offset by higher sales in other retail segments.

The latest reading of the Atlanta Fed’s Nowcast model was also released. The September quarter GDP growth estimate was lowered to 1.6% annualised, or a 0.4% expansion over the quarter.

The minutes of the Fed’s July FOMC meeting were published that afternoon. The minutes provided further indications of the tension between keeping inflation expectations from solidifying at a higher, unacceptable level and the desire not to trigger a recession by raising the federal funds rate too high.

By the end of the week, the US 2-year Treasury bond yield had lost 3bps to 3.22%, the 10-year yield had gained 14bps to 2.97% while the 30-year yield finished 10bps higher at 3.21%.

In major euro-zone markets, 10-year bond yields followed a similar path to their US counterparts except their rises on Wednesday and Friday were larger and there was little in the way of significant economic data.

On Tuesday night (AEST), Germany’s ZEW August survey indicated its Economic Sentiment index slipped from July’s reading of -53.8 to -55.3, lower than the -52.7 which had been generally expected. ZEW’s current conditions index declined from -45.8 to -47.6.

By the end of the week, the German 10-year bund yield had gained 24bps to 1.23% while the French 10-year OAT yield had added 26bps to 1.81%. The Italian 10-year BTP yield jumped by 42ps to 3.49% over the week while the British 10-year gilt yield finished 30bps higher at 2.41%.

The AOFM held two vanilla bond tenders during the week. $800 million of May 2032s and $700 million of November 2027s were priced at yields of 3.54% and 3.13% respectively. There were also three Treasury note tenders which raised $2.5 billion on a short-term basis.

The gross value of all bonds issued by the AOFM in the 2022/2023 financial year-to-date (not taking into account buy-backs or short-term Treasury note tenders) is $10.7 billion. There are currently $816.35 billion of Treasury bonds and $37.336 billion of Treasury index-linked bonds on issue. The next series to mature does so on 21 November when $26.50 billion worth of bonds are due. There are also $28.00 billion of short-term Treasury notes currently outstanding.

| MATURITY | COUPON (%) | ISSUE SIZE ($M) | CLOSING YIELD | Δ WEEK | Δ MONTH | WEEK HIGH | WEEK LOW |

|---|---|---|---|---|---|---|---|

| 21-Nov-22 | 2.25 | 26,500 | 2.28 | 0.00 | 0.12 | 2.28 | 2.21 |

| 21-Apr-23 | 5.50 | 34,200 | 2.74 | -0.11 | 0.30 | 2.79 | 2.70 |

| 21-Apr-24 | 2.75 | 35,900 | 2.88 | 0.00 | 0.30 | 2.88 | 2.72 |

| 21-Nov-24 | 0.25 | 41,300 | 2.98 | -0.03 | 0.18 | 2.98 | 2.83 |

| 21-Apr-25 | 3.25 | 40,100 | 3.09 | -0.01 | 0.12 | 3.09 | 2.93 |

| 21-Nov-25 | 0.25 | 22,000 | 3.14 | -0.01 | 0.06 | 3.14 | 2.98 |

| 21-Apr-26 | 4.25 | 38,100 | 3.16 | -0.01 | 0.06 | 3.16 | 2.99 |

| 21-Sep-26 | 0.50 | 36,000 | 3.18 | -0.02 | 0.05 | 3.18 | 3.01 |

| 21-Apr-27 | 4.75 | 36,000 | 3.18 | -0.02 | 0.04 | 3.18 | 3.02 |

| 21-Nov-27 | 2.75 | 31,400 | 3.22 | -0.02 | 0.03 | 3.22 | 3.05 |

| 21-May-28 | 2.25 | 29,700 | 3.23 | -0.04 | 0.02 | 3.23 | 3.08 |

| 21-Nov-28 | 2.75 | 32,600 | 3.26 | -0.04 | 0.01 | 3.26 | 3.10 |

| 21-Apr-29 | 3.25 | 33,000 | 3.28 | -0.03 | 0.01 | 3.28 | 3.11 |

| 21-Nov-29 | 2.75 | 33,400 | 3.31 | -0.03 | 0.00 | 3.31 | 3.14 |

| 21-May-30 | 2.50 | 37,100 | 3.33 | -0.03 | -0.01 | 3.33 | 3.16 |

| 21-Dec-30 | 1.00 | 24,700 | 3.37 | -0.03 | -0.02 | 3.37 | 3.20 |

| 21-Jun-31 | 1.50 | 38,100 | 3.39 | -0.02 | -0.01 | 3.39 | 3.21 |

| 21-Nov-31 | 1.00 | 21,000 | 3.40 | -0.02 | -0.01 | 3.40 | 3.22 |

| 21-May-32 | 1.25 | 36,800 | 3.40 | -0.02 | 0.00 | 3.40 | 3.23 |

| 21-Apr-33 | 4.50 | 20,600 | 3.43 | -0.03 | 0.00 | 3.43 | 3.25 |

| 21-Jun-35 | 2.75 | 9,550 | 3.55 | -0.02 | 0.02 | 3.55 | 3.37 |

| 21-Apr-37 | 3.75 | 12,300 | 3.63 | -0.02 | 0.05 | 3.63 | 3.45 |

| 21-Jun-39 | 3.25 | 10,300 | 3.71 | -0.02 | 0.09 | 3.71 | 3.54 |

| 21-May-41 | 2.75 | 13,500 | 3.77 | -0.03 | 0.11 | 3.77 | 3.60 |

| 21-Mar-47 | 3.00 | 13,600 | 3.79 | -0.03 | 0.14 | 3.79 | 3.63 |

| 21-Jun-51 | 1.75 | 15,000 | 3.77 | -0.02 | 0.14 | 3.77 | 3.60 |