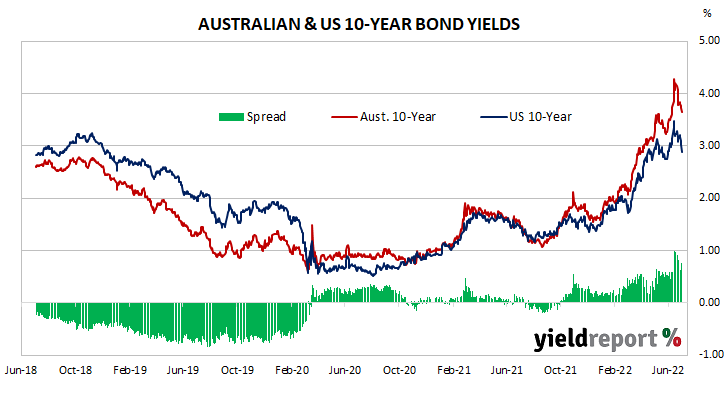

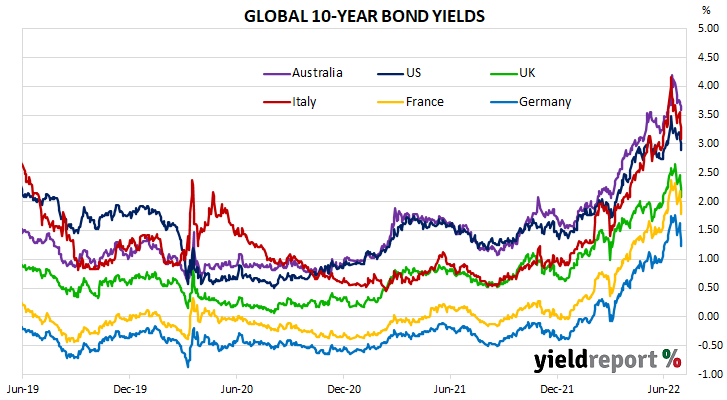

Summary: Bond yields down in Australia; ACGB 10-year spread to US Treasury yield widens from +66bps to +76bps; 10-year bond yields down in US, major European markets; AOFM issues $3.25 billion worth of bonds, notes.

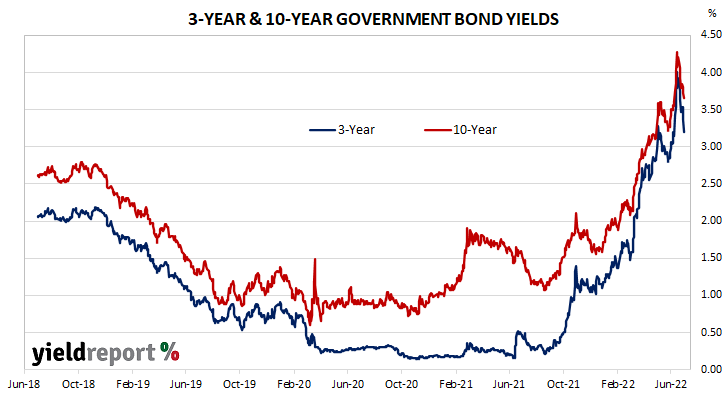

Locally, long-term ACGB yields started the week with a moderate rise but then declined through the remainder of the week. By the end of it, the 3-year ACGB yield had lost 27bps to 3.20%, the 10-year yield had shed 14bps to 3.65% while the 20-year yield finished 10bps lower at 3.86%. The spread between US and Australian 10-year Treasury bond yields widened from +66bps to +76bps.

Over in the US, long-term bond yields started the shortened week with a moderate rise before falling over the remainder of the week.

The Conference Board’s June reading of its Consumer Sentiment Index was released on Tuesday. The index deteriorated again but is still slightly above its long-term average.

A couple of days later, the latest report on personal consumption expenditures indicated core PCE price inflation increased by 0.3% in May and by 4.7% on annual basis, down from 4.9% in April.

The ISM’s June Manufacturing PMI was released at the end of the week. While it recorded a reading which signifies expansion, it moved noticeably closer to neutral.

By this point, US 2-year and 10-year Treasury bond yields had both lost 24bps to 2.83% and 2.89% respectively while the 30-year yield finished 14bps lower at 3.12%.

In major euro-zone markets, 10-year bond yields followed similar paths to their US counterparts.

The latest euro-zone’s Economic Sentiment Indicator (ESI) was released midweek. It continued its recent slide in June but remained above the long-term average. This indicator has a solid correlation with euro-zone GDP and it implied a year-to-June growth rate of 2.4%.

At the end of the week, the “flash” June consumer price index (CPI) report produced an annual inflation rate of 8.6% in the euro-zone, slightly above expectations and higher than May’s final reading of 8.1%. Food and energy prices had the largest effects during the month. Core annual CPI eased from 3.8% to 3.7%.

By this point, the German 10-year bund yield had shed 21bps to 1.23% while the French 10-year OAT yield had lost 18bps to 1.79%. The Italian 10-year BTP yield shed 35bps to 3.09% over the week while the British 10-year gilt yield finished 22bps lower at 2.08%.

The AOFM held one vanilla bond tender and one index-linked bond (ILB) tender during the week. $600 million of June 2051s were priced at a yield of 3.85% while $150 million of September 2025 ILBs were priced at a real yield of -0.34%.

There were also two Treasury note tenders which raised $2.5 billion on a short-term basis.

The gross value of all bonds issued by the AOFM in the 2021/2022 financial year (not taking into account buy-backs or short-term Treasury note tenders) is $102.25 billion. There are currently $831.213 billion of Treasury bonds and $37.236 billion of Treasury index-linked bonds on issue. The next series to mature does so on 15 July when $24.763 billion worth of bonds are due. There are also $27.5 billion of short-term Treasury notes currently outstanding.

| MATURITY | COUPON (%) | ISSUE SIZE ($M) | CLOSING YIELD | Δ WEEK | Δ MONTH | WEEK HIGH | WEEK LOW |

|---|---|---|---|---|---|---|---|

| 21-Nov-22 | 2.25 | 26,500 | 1.83 | 0.04 | 0.51 | 1.96 | 1.83 |

| 21-Apr-23 | 5.50 | 34,200 | 2.31 | -0.08 | 0.42 | 2.63 | 2.31 |

| 21-Apr-24 | 2.75 | 35,900 | 2.49 | -0.25 | 0.10 | 3.04 | 2.49 |

| 21-Nov-24 | 0.25 | 40,600 | 2.78 | -0.25 | 0.16 | 3.46 | 2.78 |

| 21-Apr-25 | 3.25 | 40,100 | 2.97 | -0.24 | 0.23 | 3.44 | 2.97 |

| 21-Nov-25 | 0.25 | 22,000 | 3.08 | -0.23 | 0.22 | 3.71 | 3.08 |

| 21-Apr-26 | 4.25 | 38,100 | 3.12 | -0.22 | 0.25 | 3.58 | 3.12 |

| 21-Sep-26 | 0.50 | 34,600 | 3.17 | -0.21 | 0.24 | 3.62 | 3.17 |

| 21-Apr-27 | 4.75 | 34,600 | 3.21 | -0.20 | 0.26 | 3.65 | 3.21 |

| 21-Nov-27 | 2.75 | 30,700 | 3.28 | -0.20 | 0.27 | 3.70 | 3.28 |

| 21-May-28 | 2.25 | 29,700 | 3.34 | -0.18 | 0.28 | 3.73 | 3.34 |

| 21-Nov-28 | 2.75 | 32,600 | 3.38 | -0.17 | 0.29 | 3.76 | 3.38 |

| 21-Apr-29 | 3.25 | 33,000 | 3.41 | -0.16 | 0.31 | 3.78 | 3.41 |

| 21-Nov-29 | 2.75 | 33,400 | 3.46 | -0.16 | 0.32 | 3.82 | 3.46 |

| 21-May-30 | 2.50 | 37,100 | 3.50 | -0.15 | 0.34 | 3.86 | 3.50 |

| 21-Dec-30 | 1.00 | 24,700 | 3.55 | -0.14 | 0.33 | 4.04 | 3.55 |

| 21-Jun-31 | 1.50 | 38,100 | 3.57 | -0.13 | 0.34 | 4.06 | 3.57 |

| 21-Nov-31 | 1.00 | 21,000 | 3.59 | -0.13 | 0.35 | 4.06 | 3.59 |

| 21-May-32 | 1.25 | 35,200 | 3.59 | -0.13 | 0.34 | 4.07 | 3.59 |

| 21-Apr-33 | 4.50 | 19,800 | 3.61 | -0.13 | 0.34 | 4.09 | 3.61 |

| 21-Jun-35 | 2.75 | 9,550 | 3.72 | -0.12 | 0.35 | 4.04 | 3.72 |

| 21-Apr-37 | 3.75 | 12,000 | 3.75 | -0.11 | 0.32 | 4.07 | 3.75 |

| 21-Jun-39 | 3.25 | 10,300 | 3.79 | -0.11 | 0.28 | 4.11 | 3.79 |

| 21-May-41 | 2.75 | 13,500 | 3.81 | -0.12 | 0.25 | 4.15 | 3.81 |

| 21-Mar-47 | 3.00 | 13,300 | 3.83 | -0.08 | 0.25 | 4.13 | 3.83 |

| 21-Jun-51 | 1.75 | 15,000 | 3.81 | -0.03 | 0.26 | 4.09 | 3.81 |