Summary: 10-year bond yields drop in Australia; ACGB 10-year spread to US Treasury yield tightens from +98bps to +66bps; 10-year bond yields down in the US, major European markets; AOFM issues $3 billion worth of bonds, notes.

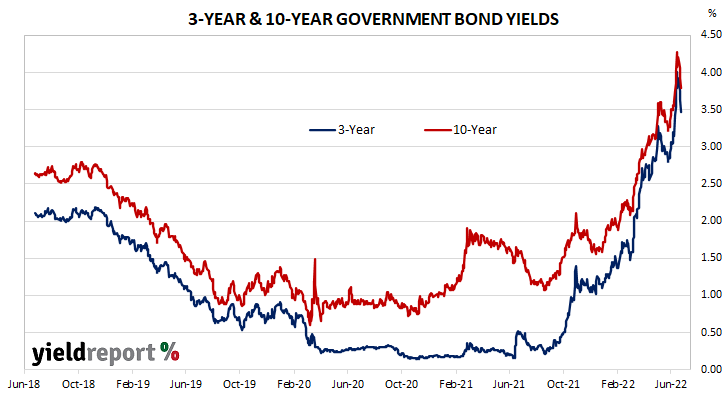

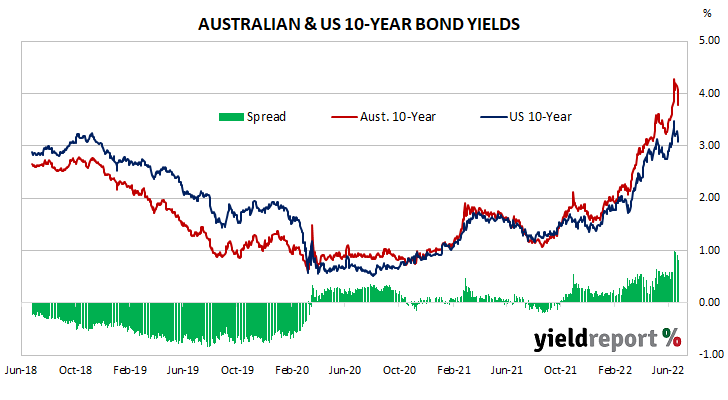

Locally, long-term ACGB yields started the week with a moderate fall and then continued to decrease through the week. By the end of it, the 3-year ACGB yield had dropped by 45bps to 3.47%, the 10-year yield had shed 42bps to 3.79% while the 20-year yield finished 46bps lower at 3.96%. The spread between US and Australian 10-year Treasury bond yields tightened from +98bps to +66bps.

Over in the US, long-term bond yields started the shortened week with a moderate rise before falling materially over the next two days. Yields then moved moderately higher at the end of the week.

Fed chief Jerome Powell provide testimony to the lower and upper houses of the US Congress on Wednesday and Thursday. He made it clear the US Fed was set on reducing inflation.

IHS Markit’s latest flash reading of its composite index was released on Thursday, with the index falling from May’s final reading of 53.6 to 51.2. The manufacturing index dropped from 57.0 to 52.4 and the services index lost 4.6 points to 52.4. “The pace of US economic growth has slowed sharply in June, with deteriorating forward-looking indicators setting the scene for an economic contraction in the third quarter,” according to IHS Markit’s Chris Williamson.

By the end of the week, the US 2-year Treasury bond yield had lost 7bps to 3.12%, the 10-year yield had shed 10bps to 3.13% while the 30-year yield finished 2bps lower at 3.26%.

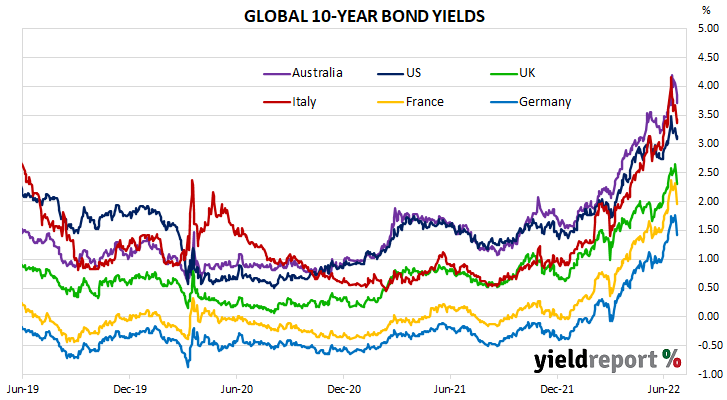

In major euro-zone markets, 10-year bond yields followed similar paths to their US counterparts, except the falls on Wednesday and Thursday were markedly larger.

The results of June’s consumer sentiment survey were released midweek. They indicated euro-zone consumers had become as pessimistic as they were at the beginning of the pandemic in April 2020.

IHS Markit released its June flash PMI figures for the euro-zone the next day. The preliminary reading of the composite index was 51.9, down from May’s final reading of 54.8. IHS Markit’s Chris Williamson described euro-zone growth as “showing signs of faltering” as pent-up demand fades.

Germany’s ifo Institute released the June reading of its business climate index at the end of the week. The index declined a little as German firms’ views of current conditions deteriorated somewhat and their expectations “turned markedly more pessimistic.”

By this point, the German 10-year bund yield had shed 21bps to 1.44% while the French 10-year OAT yield had lost 23bps to 1.97%. The Italian 10-year BTP yield lost 14bps to 3.44% over the week while the British 10-year gilt yield finished 20bps lower at 2.30%.

The AOFM held just the one bond tender during the week, with $1 billion of April 2025s priced at a yield of 3.48%.

There were also two Treasury note tenders which raised $2.0 billion on a short-term basis.

The gross value of all bonds issued by the AOFM in the 2021/2022 financial year-to-date (not taking into account buy-backs or short-term Treasury note tenders) is $101.5 billion. There are currently $830.913 billion of Treasury bonds and $37.086 billion of Treasury index-linked bonds on issue. The next series to mature does so on 15 July when $24.763 billion worth of bonds are due. There are also $23.5 billion of short-term Treasury notes currently outstanding after $4.25 billion matured on Friday.

| MATURITY | COUPON (%) | ISSUE SIZE ($M) | CLOSING YIELD | Δ WEEK | Δ MONTH | WEEK HIGH | WEEK LOW |

|---|---|---|---|---|---|---|---|

| 21-Nov-22 | 2.25 | 26,500 | 1.79 | -0.24 | 0.50 | 2.02 | 1.79 |

| 21-Apr-23 | 5.50 | 34,200 | 2.39 | -0.44 | 0.47 | 2.82 | 2.39 |

| 21-Apr-24 | 2.75 | 35,900 | 2.75 | -0.57 | 0.26 | 3.31 | 2.75 |

| 21-Nov-24 | 0.25 | 40,600 | 3.04 | -0.45 | 0.34 | 3.48 | 3.04 |

| 21-Apr-25 | 3.25 | 40,100 | 3.20 | -0.43 | 0.41 | 3.63 | 3.20 |

| 21-Nov-25 | 0.25 | 22,000 | 3.31 | -0.43 | 0.41 | 3.73 | 3.31 |

| 21-Apr-26 | 4.25 | 38,100 | 3.34 | -0.42 | 0.42 | 3.76 | 3.34 |

| 21-Sep-26 | 0.50 | 34,600 | 3.38 | -0.42 | 0.41 | 3.81 | 3.38 |

| 21-Apr-27 | 4.75 | 34,600 | 3.42 | -0.42 | 0.42 | 3.84 | 3.42 |

| 21-Nov-27 | 2.75 | 30,700 | 3.48 | -0.41 | 0.41 | 3.90 | 3.48 |

| 21-May-28 | 2.25 | 29,700 | 3.52 | -0.41 | 0.40 | 3.92 | 3.52 |

| 21-Nov-28 | 2.75 | 32,600 | 3.55 | -0.41 | 0.40 | 3.95 | 3.55 |

| 21-Apr-29 | 3.25 | 33,000 | 3.58 | -0.40 | 0.40 | 3.98 | 3.58 |

| 21-Nov-29 | 2.75 | 33,400 | 3.62 | -0.40 | 0.41 | 4.02 | 3.62 |

| 21-May-30 | 2.50 | 37,100 | 3.65 | -0.41 | 0.41 | 4.06 | 3.65 |

| 21-Dec-30 | 1.00 | 24,700 | 3.69 | -0.42 | 0.42 | 4.10 | 3.69 |

| 21-Jun-31 | 1.50 | 38,100 | 3.70 | -0.41 | 0.42 | 4.12 | 3.70 |

| 21-Nov-31 | 1.00 | 21,000 | 3.71 | -0.41 | 0.42 | 4.12 | 3.71 |

| 21-May-32 | 1.25 | 35,200 | 3.72 | -0.41 | 0.41 | 4.13 | 3.72 |

| 21-Apr-33 | 4.50 | 19,800 | 3.74 | -0.41 | 0.41 | 4.15 | 3.74 |

| 21-Jun-35 | 2.75 | 9,550 | 3.84 | -0.41 | 0.38 | 4.25 | 3.84 |

| 21-Apr-37 | 3.75 | 12,000 | 3.86 | -0.42 | 0.32 | 4.28 | 3.86 |

| 21-Jun-39 | 3.25 | 10,300 | 3.90 | -0.44 | 0.27 | 4.34 | 3.90 |

| 21-May-41 | 2.75 | 13,500 | 3.93 | -0.44 | 0.25 | 4.38 | 3.93 |

| 21-Mar-47 | 3.00 | 13,300 | 3.91 | -0.48 | 0.19 | 4.28 | 3.91 |

| 21-Jun-51 | 1.75 | 15,000 | 3.84 | -0.51 | 0.14 | 4.35 | 3.84 |