Summary: 10-year bond yields down in Australia, the US, up in most major European markets; ACGB 10-year spread to US Treasury yield widens from +52bps to +55bps; AOFM issues $3.0 billion worth of bonds, notes.

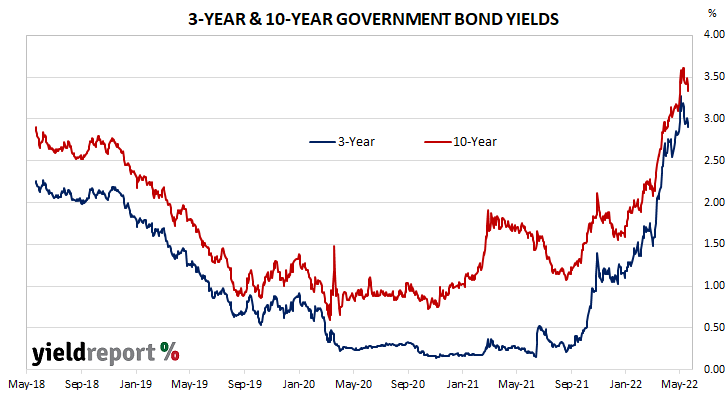

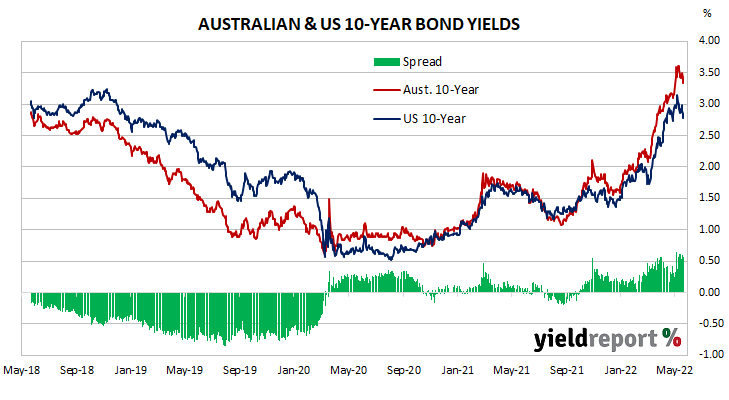

Locally, long-term ACGB yields rose over the first three days of the week before falling over the remainder of the week. By the end of it, the 3-year ACGB yield had lost 4bps to 2.90%, the 10-year yield had shed 11bps to 3.33% while the 20-year yield finished 5bps lower at 3.71%. The spread between US and Australian 10-year Treasury bond yields widened from +52bps to +55bps.

Over in the US, long-term bond yields fell over much of the week with a single short bounce in the middle of it.

April’s retail sales report was released on Tuesday. Sales grew by 0.9% over the month, just short of expectations, and by 8.2% over the year. Once again, economists noted price rises were the driving force behind the increase.

US industrial production numbers for April were released on the same day. The figures were better than expected and they implied an annual GDP growth rate of 4.7%.

The Conference Board’s April reading of its Leading Index came out on Thursday. The figure undershot expectations and The Conference Board cut its 2022 GDP forecast from 3.0% to 2.3%.

By the end of the week, the US 2-year Treasury bond yield had slipped 1bp to 2.57%, the 10-year yield had shed 14bps to 2.78% while the 30-year yield finished 9bps lower at 2.99%.

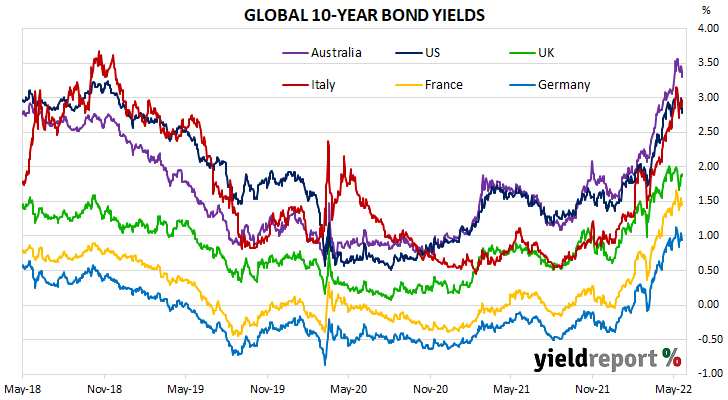

In major euro-zone markets, 10-year bond yields once again followed a broadly-similar pattern to their US counterparts. However, “down” days were smaller in magnitude.

The results of May’s consumer sentiment survey were released at the end of the week. They indicated euro-zone consumers had become a little less pessimistic for a second consecutive month.

By this point, the German 10-year bund yield had slipped 1bp to 0.94% while the French 10-year OAT yield had gained 7bps to 1.47%. The Italian 10-year BTP yield added 12bps to 2.97% over the week and the British 10-year gilt yield finished 15bps higher at 1.89%.

The AOFM held two vanilla bond tenders during the week. $800 million of November 2032s and $700 million of April 2027s were priced at yields of 3.49% and 3.29% respectively. There were also two Treasury note tenders which raised $1.5 billion on a short-term basis.

The gross value of all bonds issued by the AOFM in the 2021/2022 financial year-to-date (not taking into account buy-backs or short-term Treasury note tenders) is $96.05 billion. There are currently $824.713 billion of Treasury bonds and $36.836 billion of Treasury index-linked bonds on issue. The next series to mature does so on 15 July when $24.763 billion worth of bonds are due. There are also $27 billion of short-term Treasury notes currently outstanding.

| MATURITY | COUPON (%) | ISSUE SIZE ($M) | CLOSING YIELD | Δ WEEK | Δ MONTH | WEEK HIGH | WEEK LOW |

|---|---|---|---|---|---|---|---|

| 21-Nov-22 | 2.25 | 26,500 | 1.29 | -0.02 | 0.59 | 1.36 | 1.29 |

| 21-Apr-23 | 5.50 | 34,200 | 1.92 | -0.05 | 0.66 | 2.03 | 1.92 |

| 21-Apr-24 | 2.75 | 35,900 | 2.48 | -0.07 | 0.46 | 2.61 | 2.48 |

| 21-Nov-24 | 0.25 | 40,600 | 2.69 | -0.03 | 0.47 | 2.80 | 2.69 |

| 21-Apr-25 | 3.25 | 38,100 | 2.79 | -0.02 | 0.43 | 2.89 | 2.79 |

| 21-Nov-25 | 0.25 | 22,000 | 2.89 | -0.03 | 0.40 | 3.00 | 2.89 |

| 21-Apr-26 | 4.25 | 38,100 | 2.92 | -0.03 | 0.39 | 3.03 | 2.92 |

| 21-Sep-26 | 0.50 | 33,800 | 2.97 | -0.04 | 0.37 | 3.08 | 2.97 |

| 21-Apr-27 | 4.75 | 33,900 | 3.00 | -0.04 | 0.38 | 3.11 | 3.00 |

| 21-Nov-27 | 2.75 | 30,700 | 3.06 | -0.05 | 0.37 | 3.18 | 3.06 |

| 21-May-28 | 2.25 | 29,700 | 3.11 | -0.06 | 0.36 | 3.23 | 3.11 |

| 21-Nov-28 | 2.75 | 32,600 | 3.15 | -0.06 | 0.36 | 3.27 | 3.15 |

| 21-Apr-29 | 3.25 | 33,000 | 3.17 | -0.06 | 0.36 | 3.30 | 3.17 |

| 21-Nov-29 | 2.75 | 33,400 | 3.21 | -0.07 | 0.36 | 3.34 | 3.21 |

| 21-May-30 | 2.50 | 37,100 | 3.24 | -0.07 | 0.35 | 3.37 | 3.24 |

| 21-Dec-30 | 1.00 | 24,700 | 3.27 | -0.08 | 0.34 | 3.41 | 3.27 |

| 21-Jun-31 | 1.50 | 37,300 | 3.29 | -0.09 | 0.35 | 3.43 | 3.29 |

| 21-Nov-31 | 1.00 | 21,000 | 3.30 | -0.09 | 0.34 | 3.45 | 3.30 |

| 21-May-32 | 1.25 | 34,200 | 3.31 | -0.09 | 0.34 | 3.46 | 3.31 |

| 21-Apr-33 | 4.50 | 19,800 | 3.33 | -0.09 | 0.35 | 3.48 | 3.33 |

| 21-Jun-35 | 2.75 | 9,550 | 3.46 | -0.09 | 0.36 | 3.60 | 3.46 |

| 21-Apr-37 | 3.75 | 12,000 | 3.54 | -0.07 | 0.38 | 3.68 | 3.54 |

| 21-Jun-39 | 3.25 | 10,300 | 3.63 | -0.07 | 0.37 | 3.76 | 3.63 |

| 21-May-41 | 2.75 | 13,500 | 3.69 | -0.06 | 0.36 | 3.81 | 3.69 |

| 21-Mar-47 | 3.00 | 13,300 | 3.72 | -0.06 | 0.33 | 3.84 | 3.72 |

| 21-Jun-51 | 1.75 | 15,000 | 3.70 | -0.06 | 0.30 | 3.81 | 3.70 |