Summary: ACGB yields up in Australia; ACGB 10-year spread to US Treasury yield fall to 21bps; 10-year bond yields up in US, UK, down in other major European markets; $1.65 billion of bonds issued by AOFM.

Locally, long-term ACGB yields started the week quietly enough but then jumped midweek following a large upward movement from US yields. Yield moved a little higher from there before falling back moderately at the end of the week. By this point, the 3-year ACGB yield had gained 9bps to 4.17%, the 10-year yield had added 6bps to 4.65% while the 20-year yield finished 3bps higher at 4.94%. The spread between US and Australian 10-year Treasury bond yields fell back from 28bps to 21bps.

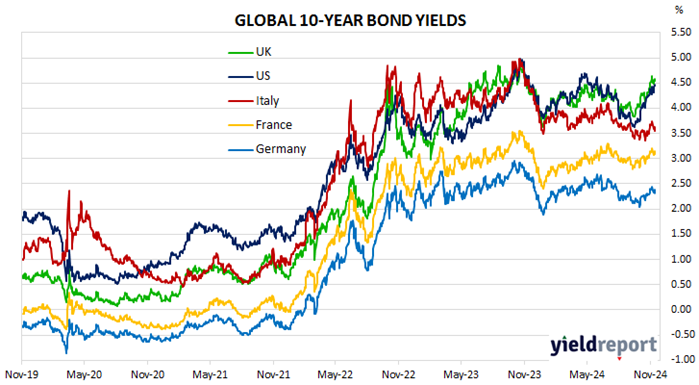

Over in the US, 10-year bond yields were quite stable through the shortened week with the exception of Tuesday when yields jumped.

There were no particularly notable US economic data releases until midweek when October CPI figures came out. The headline CPI increased by 0.2%, in line with expectations, taking the annual inflation rate from 2.4% to 2.6%. The annual core inflation rate remained unchanged at 3.3%.

October producer price indices were released the next day. The headline PPI also increased by 0.2% over the month, also in line with expectations, while the annual growth rate accelerated from 1.9% to 2.4%. The core annual growth rate ticked up from 3.0% to 3.1%.

October retail sales and October industrial production figures were released at the end of the week. Retail sales increased by 0.4% over the month, greater than the 0.3% rise which had been generally expected but less than September’s upwardly-revised 0.8% increase. October industrial production contracted by 0.3% over the month, a slightly larger fall than expected.

The New York Fed’s Nowcast model was also updated as usual. The December 2024 quarter forecast remained unchanged at 2.1% (annualised).

By this point, the US 2-year Treasury bond yield had added 6bps to 4.32%, the 10-year yield had gained 13bps to 4.44% while the 30-year yield finished 15bps higher at 4.62%.

In major euro-zone markets, 10-year bond yields see-sawed moderately throughout the week.

Germany’s ZEW November survey was published on Tuesday and it indicated the ZEW Economic Sentiment index had dropped back 13.1 points to 7.4 points. “Economic expectations for Germany have been overshadowed by Trump’s victory and the collapse of the German government coalition.” ZEW’s current conditions index decreased again, this time from -86.9 points to -91.4 points.

The euro-zone’s September industrial production figures came out on Thursday. Output fell by 2.0% over the month, worse than expected, and by 2.8% when compared to September 2023.

By the end of the week, the German 10-year bond yield had declined 2bps to 2.35% while the French 10-year OAT had lost 4bps to 3.09%. The Italian 10-year BTP yield lost 1bps to 3.55% over the week while the British 10-year gilt yield finished 4bps higher at 4.54%.

The AOFM held an index-linked bond (ILB) tender in addition to two vanilla bond tenders this week. $150 million of November 2032 ILBs were priced at a real yield of 2.05% while $800 million of May 2030s and $700 million of April 2027s were priced at nominal yields of 4.33% and 4.19% respectively. There were also two Treasury note tenders which raised $2.0 billion on a short-term basis.

The gross value of all bonds issued by the AOFM in the 2024/2025 financial year (not taking into account short-term Treasury note tenders) is $40.35 billion. There are currently $877.35 billion of Treasury bonds and $41.885 billion of Treasury index-linked bonds on issue. The next series to mature does so on 21 November 2024 when $41.30 billion worth of bonds are due. There are also $30.00 billion of short-term Treasury notes outstanding.