Summary: ACGB yields up in Australia; ACGB 10-year spread to US Treasury yield rises to 14bps; 10-year bond yields up in US, major European markets; $1.5 billion of bonds issued by AOFM.

Locally, long-term ACGB yields moved higher throughout the entire (shortened for some states) week. By the end of it, the 3-year ACGB yield had gained 18bps to 3.74,%, the 10-year yield had added 16bps to 4.24% while the 20-year yield finished 15bps higher at 4.64%. The spread between US and Australian 10-year Treasury bond yields increased from 12bps to 14bps.

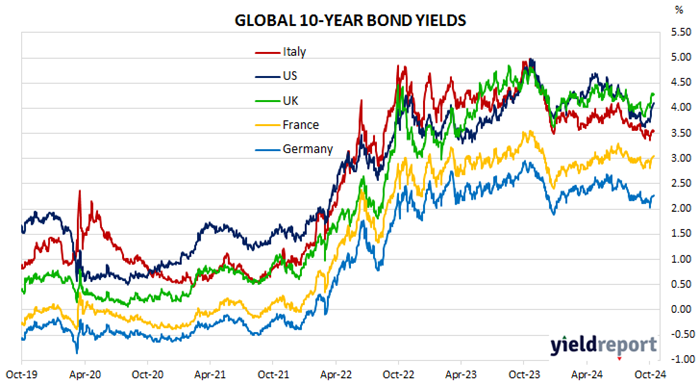

Over in the US, 10-year bond yields see-sawed through the week but the rises were greater in magnitude than the falls.

There were no particularly notable US economic data releases until Thursday when September CPI figures came out. The headline CPI increased by 0.2%, above expectations, but the annual inflation rate still slowed from 2.6% to 2.4%. The annual core inflation rate remained unchanged at 3.3%.

September producer price indices were released at the end of the week. The headline PPI remained

unchanged over the month, slightly below expectations, while the annual growth rate slowed from 1.9% after revisions to 1.8%. However, the core annual growth rate increased from 2.7% to 2.8%.

The University of Michigan’s October reading of its consumer sentiment index came out that same day. It produced a small decline, slightly below expectations. Short-term inflation expectations increased from 2.7% to 2.9%.

The New York Fed’s Nowcast model was also updated as usual. The September 2024 quarter forecast remained unchanged at 3.1% (annualised) as did the December 2024 forecast at 2.8%.

By this stage, the US 2-year Treasury bond yield had added 4bps to 3.96%, the 10-year yield had gained 14bps to 4.10% while the 30-year yield finished 17bps higher at 4.41%.

In major euro-zone markets, 10-year bond yields moved in a fairly similar fashion to their US counterpart.

By the end of the week, the German 10-year bond yield had added 5bps to 2.26% and the French 10-year OAT had gained 6bps to 3.05%. The Italian 10-year BTP yield increased by 5bps to 3.56% over the week while the British 10-year gilt yield finished 6bps higher at 4.28%.

The AOFM held two bond tenders this week. $1 billion of June 2039s and $500 million of November 2028s were priced at nominal yields of 4.39% and 3.78% respectively. There were also two Treasury note tenders which raised $2.0 billion on a short-term basis.

The gross value of all bonds issued by the AOFM in the 2024/2025 financial year (not taking into account short-term Treasury note tenders) is $30.85 billion. There are currently $869.55 billion of Treasury bonds and $41.635 billion of Treasury index-linked bonds on issue. The next series to mature does so on 21 November 2024 when $41.30 billion worth of bonds are due. There are also $25.00 billion of short-term Treasury notes outstanding.