Summary: ACGB bond yields up in Australia; ACGB 10-year spread to US Treasury yield rises to 20bps; 10-year bond yield up in US, major European markets; $3.5 billion of bonds, notes issued by AOFM.

Locally, long-term ACGB yields started with a small decline, rose over the following three days before ending the week with another small decline. By this point, the 3-year ACGB yield had slipped 1bp to 3.42,%, the 10-year yield had gained 11bps to 3.94% while the 20-year yield finished 10bps higher at 4.33%. The spread between US and Australian 10-year Treasury bond yields increased from 18bps to 20bps.

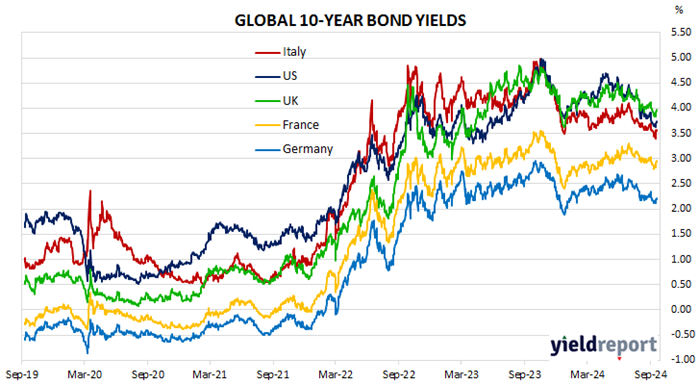

Over in the US, 10-year bond yields slipped at the start of the week and then increased steadily over the next four days.

August’s retail sales figures were released on Tuesday. Total sales increased by just 0.1%, in contrast with the expected fall but well down from July’s 1.1% jump.

August industrial production figures were also posted that day. Production expanded by 0.8% over the month, a larger increase than expected.

The Conference Board’s August reading of its Leading Index came out a couple of days later. The index posted a 0.2% fall, another decline in a long list of them since early 2022.

The New York Fed’s Nowcast model was also updated as usual at the end of the week. The September 2024 quarter forecast was raised from 2.6% (annualised) to 3.0%, while the December 2024 forecast was raised from 2.2% to 2.7%.

By this point, the US 2-year Treasury bond yield had added 2bps to 3.61%, the 10-year yield had gained 9bps to 3.74% while the 30-year yield finished 10bps higher at 4.08%.

In major euro-zone markets, 10-year bond yields moved in a similar fashion to their US counterpart.

Germany’s ZEW September survey was published on Tuesday and it indicated the ZEW Economic Sentiment index had fallen again, this time from 19.2 points to 3.6 points. ZEW’s current conditions index also decreased, from -77.3 points to -84.5 points. “The optimism in economic expectations that has been evident since November 2023 has thus almost completely dwindled.”

September’s euro-zone consumer sentiment report was released at the end of the week. The index indicated sentiment had improved modestly again, and is now not that far below its long-term average.

By the end of the week, the German 10-year bond yield had added 6bps to 2.21% and the French 10-year OAT had gained 12bps to 2.96%. The Italian 10-year BTP yield increased by 13bps to 3.57% over the week, as did the British 10-year gilt yield to 3.98%.

The AOFM held two vanilla bond tenders this week. $1.0 billion of April 2037s and $500 million of April 2029s were priced at nominal yields of 3.96% and 3.53% respectively. There were also two Treasury note tenders which raised $2.0 billion on a short-term basis.

The gross value of all bonds issued by the AOFM in the 2024/2025 financial year (not taking into account short-term Treasury note tenders) is $27.70 billion. There are currently $865.05 billion of Treasury bonds and $41.485 billion of Treasury index-linked bonds on issue. The next series to mature does so on 21 November 2024 when $41.30 billion worth of bonds are due. There are also $29.00 billion of short-term Treasury notes outstanding.