Summary: ACGB bond yields down in Australia; ACGB 10-year spread to US Treasury yield steady at +18bps; 10-year bond yields down in US, major European markets; $3.1 billion of bonds, notes issued by AOFM.

Locally, long-term ACGB yields started with a noticeable rise before falling back through most of the remaining days of the week. By the end of it, 3-year and 10-year ACGB yields had both lost 6bps to 3.43% and 3.83% respectively while the 20-year yield finished 9bps lower at 4.23%. The spread between US and Australian 10-year Treasury bond yields remained steady at +18bps.

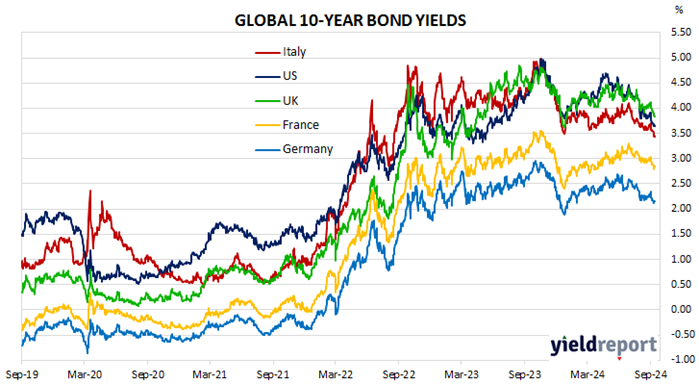

Over in the US, 10-year bond yields declined early in the week before stabilising in the latter part of it.

August CPI figures came out on Wednesday. The headline CPI increased by 0.2%, in line with expectations, slowing the annual inflation rate from 2.9% to 2.6% while the core inflation rate ticked up from 3.2% to 3.3%.

August producer price indices were released on Tuesday. The headline PPI increased by 0.2% over the month, slightly above expectations, while the annual growth rate slowed from 2.2% to 1.8%.

The University of Michigan’s September reading of its consumer sentiment index came out at the end of the week. It produced another modestly higher figure, slightly above expectations. Short-term inflation expectations declined from 2.9% to 2.7%.

The New York Fed’s Nowcast model was also updated as usual. The September 2024 quarter forecast remained steady at 2.6% (annualised), as did the December 2024 forecast at 2.2%.

By this point, US 2-year and 10-year Treasury bond yields had both lost 6bps to 3.59% and 3.65% while the 30-year yield finished 4bps lower at 3.98%.

In major euro-zone markets, 10-year bond yields moved in a vaguely similar fashion to their US counterpart.

The ECB policy meeting took place on Thursday. The ECB’s various policy rates were each lowered by 25bps, as expected.

The euro-zone’s July industrial production figures were released at the end of the week. Output fell by 0.3% over the month, in line with expectations, and was 2.2% lower than in July 2023.

By the end of the week, the German 10-year bond yield had lost 2bps to 2.15% and the French 10-year OAT had shed 4bps to 2.84%. The Italian 10-year BTP yield shed 11bps to 3.44% over the week while the British 10-year gilt yield finished another 12bps lower at 3.85%.

The AOFM held one vanilla bond tender and an index-linked bond (ILB) tender this week. $1.0 billion of November 2027s were priced at a nominal yield of 3.99% while the November 2027 ILBs were priced at a real yield of 1.18%. There were also two Treasury note tenders which raised $2.0 billion on a short-term basis.

The gross value of all bonds issued by the AOFM in the 2024/2025 financial year (not taking into account short-term Treasury note tenders) is $25.10 billion. There are currently $863.55 billion of Treasury bonds and $41.485 billion of Treasury index-linked bonds on issue. The next series to mature does so on 21 November 2024 when $41.30 billion worth of bonds are due. There are also $27.00 billion of short-term Treasury notes outstanding.