Summary: ACGB bond yields up in Australia; ACGB 10-year spread to US Treasury yield falls to +7bps; 10-year bond yields up in US, major European markets; $3.6 billion of bonds, notes issued by AOFM.

Locally, long-term ACGB yields started with a moderate fall before rising through the remaining days of the week. By the end of it, the 3-year ACGB yield had inched 1bp higher to 3.54% while 10-year and 20-year yields both finished 4bps higher at 3.97% and 4.36% respectively. The spread between US and Australian 10-year Treasury bond yields fell from +13bps to +7bps.

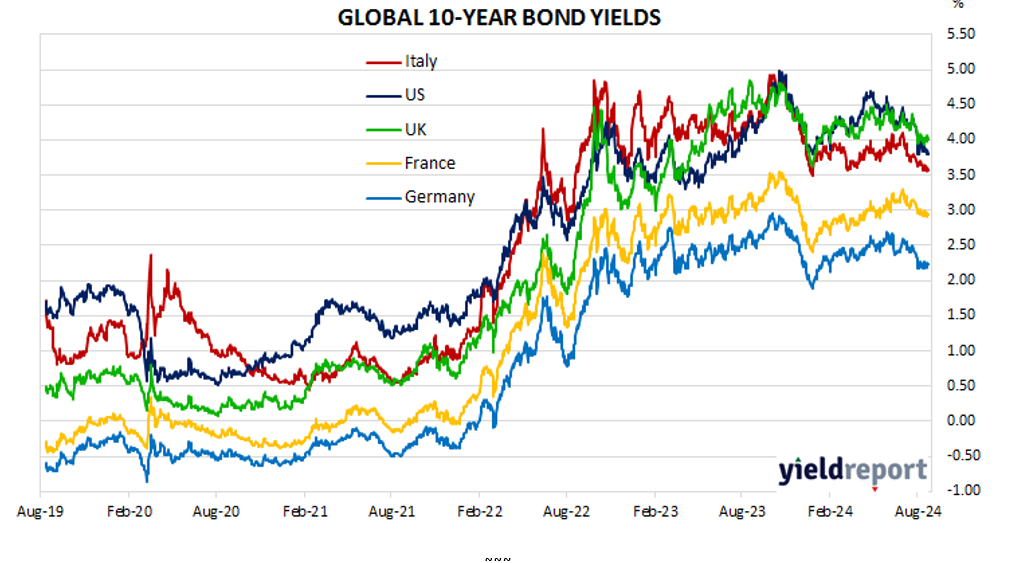

Over in the US, 10-year bond yields rose modestly each day of the week.

There was not a lot of “primary” US data posted during the week and no particularly notable data was released until Friday when the latest report on personal consumption expenditures came out. Core PCE price inflation increased by 0.2% in July and by 2.6% on an annual basis, unchanged from June’s comparable figure.

The New York Fed’s Nowcast model was also updated as usual. The September 2024 quarter forecast was raised from 1.9% (annualised) to 2.5%.

By this point, the US 2-year Treasury bond yield had returned to its starting point at 3.91% while 10-year and 30-year yields had both gained 10bps to 3.90% and 4.19% respectively.

In major euro-zone markets, 10-year bond yields moved in a broadly-similar fashion to their US counterpart except they declined midweek.

Germany’s ifo Institute released the August reading of its business climate index at the start of the week. The index declined again as German firms’ views of current conditions and the short-term outlook both deteriorated.

The latest reading of the euro-zone’s Economic Sentiment Indicator (ESI) was posted on Thursday. The index improved slightly in August and remains noticeably under its long-term average. This indicator has a solid correlation with euro-zone GDP and it implied a year-to-August growth rate of 0.8%.

The “flash” August consumer price index (CPI) report was released at the end of the week. The euro-zone CPI increased by 0.2% over the month and by 2.2% over the year, down from 2.6% in July. Annual core CPI slowed from 2.9% to 2.8%.

By this stage, the German 10-year bund yield had gained 7bps to 2.30% while the French 10-year OAT yield had increased by 8bps to 3.01%. The Italian 10-year BTP yield added 11bps to 3.68% over the week while the British 10-year gilt yield finished 8bps higher at 4.09%.

The AOFM held an index-linked bond (ILB) tender as well as two vanilla tenders this week. $100 million of February 2050 ILBs were priced at a real yield of 1.51% while $800 million of December 2034s and $700 million of November 2029s were priced at nominal yields of 3.91% and 3.64% respectively. There were also two Treasury note tenders which raised $2.0 billion on a short-term basis.

The gross value of all bonds issued by the AOFM in the 2024/2025 financial year (not taking into account short-term Treasury note tenders) is $23.90 billion. There are currently $861.35 billion of Treasury bonds and $41.385 billion of Treasury index-linked bonds on issue. The next series to mature does so on 21 November 2024 when $41.30 billion worth of bonds are due. There are also $28.00 billion of short-term Treasury notes outstanding.