Summary: ACGB bond yields fall in Australia; ACGB 10-year spread to US Treasury yield falls to +5bps; 10-year bond yields up in US, mixed in major European markets; $3.5 billion of bonds, notes issued by AOFM.

Locally, long-term ACGB yields started the week with a modest rise which was followed the next day with a significant fall. Yields then remained pretty steady for a couple of days before rising moderately at the end of the week. By this point, the 3-year ACGB yield had lost 5bps to 3.97%, the 10-year yield had shed 4bps to 4.29% while the 20-year yield finished 2bps lower at 4.64%. The spread between US and Australian 10-year Treasury bond yields fell from +15bps to +5bps.

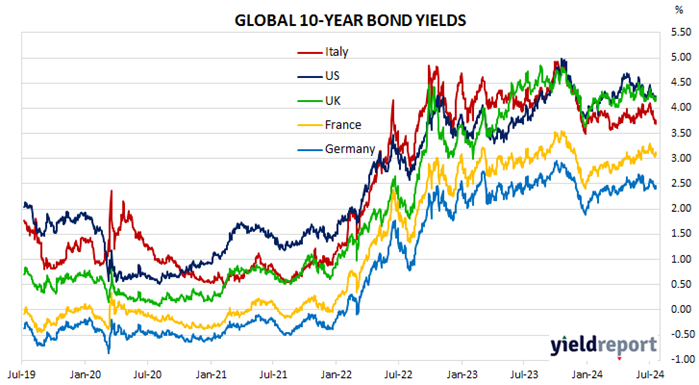

Over in the US, 10-year bond yields see-sawed early in the week, stabilised and then rose moderately on Thursday and Friday.

June’s retail sales report was released on Tuesday. Total sales were flat, more than expected, but down from May’s upwardly revised figure.

June industrial production figures were posted the next day. Production increased by 0.6% over the month, more than expected.

The Conference Board’s June reading of its Leading Index posted a 0.2% fall on Thursday, another decline in a long list of them since early 2022.

The New York Fed’s Nowcast model was updated as usual at the end of the week. The June 2024 quarter forecast was increased from 1.80% (annualised) to 2.0%, while the September 2024 quarter forecast rose from 2.20% to 2.70%.

By this point, US 2-year and 10-year Treasury bond yields had both gained 6bps to 4.51% and 4.24% respectively while the 30-year yield finished 5bps higher at 4.45%.

In major euro-zone markets, 10-year bond yields moved in a broadly-similar fashion to their US counterpart.

Germany’s ZEW July survey was published on Tuesday and it indicated the ZEW Economic Sentiment index had fallen back from June’s reading of 47.5 to 41.8. ZEW’s current conditions index increased, however, from -73.8 to -68.9. “For the first time in a year, economic expectations for Germany are falling.”

The ECB policy meeting on Thursday decided to leave the ECB’s various policy rates unchanged. However, the September meeting has been flagged as “live”.

By the end of the week, the German 10-year bund yield had returned to its starting point at 2.47% while the French 10-year OAT yield had gained 4bps to 3.13%. The Italian 10-year BTP yield lost 2bps to 3.77% over the week while the British 10-year gilt yield finished 2bps higher at 4.23%.

The AOFM held three tenders this week. $300 million of June 2051s, $500 million of November 2033s and $700 million of November 2027s were priced at yields of 4.74%, 4.22% and 3.98% respectively. There were also two Treasury note tenders which raised $2.0 billion on a short-term basis.

The gross value of all bonds issued by the AOFM in the 2024/2025 financial year (not taking into account short-term Treasury note tenders) is $4.60 billion. There are currently $842.35 billion of Treasury bonds and $41.085 billion of Treasury index-linked bonds on issue. The next series to mature does so on 21 November 2024 when $41.30 billion worth of bonds are due. There are also $30.00 billion of short-term Treasury notes outstanding.