Summary: ACGB bond yields rise in Australia; ACGB 10-year spread to US Treasury yield rises to -15bps; 10-year bond yields up in US, major European markets; $3.20 billion of bonds, notes issued by AOFM.

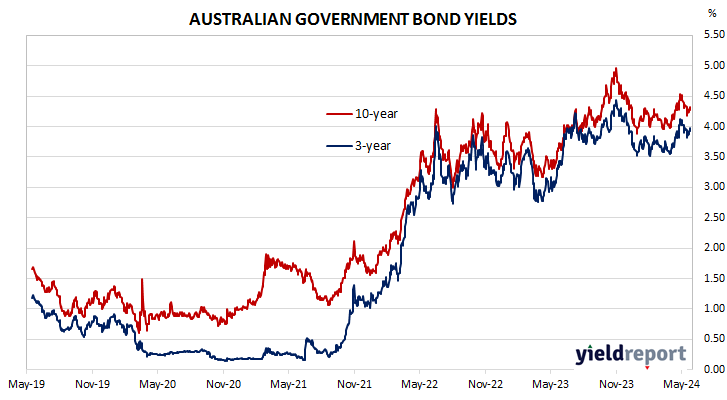

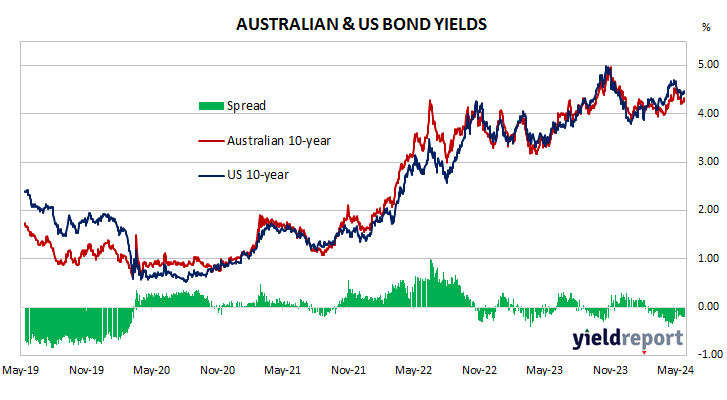

Locally, long-term ACGB yields moved up through much of the week with the exception of Thursday when yields pulled back moderately. By the end of the week, the 3-year ACGB yield had gained 14bps to 3.98% while 10-year and 20-year yields both finished 10bps higher at 4.22% and 4.62% respectively. The spread between US and Australian 10-year Treasury bond yields rose from -20bps to -15bps.

Over in the US, 10-year bond yields oscillated early in the week, stabilised midweek and then rose on Thursday before slipping back at the end of the week.

US economic reports were thin on the ground this week.

Minutes of the FOMC May meeting came out midweek. They indicated US policy rates were likely to stay where they are for longer than previously expected.

S&P Global Market Intelligence’s flash May reading of its US composite index came out on Thursday, posting a rise from 51.3 in April to 54.4. The manufacturing index increased from 50.0 to 50.9 while the services index increased by 3.5 to 54.8. S&P Global Market Intelligence Chief Business Economist Chris Williamson said, “The data put the US economy back on course for another solid GDP gain in the second quarter.”

The New York Fed’s Nowcast model was also updated at the end of the week. The June 2024 quarter forecast was raised from 1.9% (annualised) to 2.0%.

By this point, the US 2-year Treasury bond yield had gained 12bps to 4.95%, the 10-year yield had added 5bps to 4.47% while the 30-year yield finished 1bp higher at 4.57%.

In major euro-zone markets, 10-year bond yields followed a broadly-similar pattern to their US.

S&P Global Market Intelligence released its flash May PMI figures for the euro-zone on Thursday. The preliminary reading of the composite index was 52.3, up from April’s final reading of 51.7. “The PMI composite for May indicates growth for three months straight and that the eurozone’s economy is gathering further strength,” said Hamburg Commercial Bank Chief Economist Dr. Cyrus de la Rubia.

May’s consumer sentiment report was also released. The index indicated euro-zone sentiment had improved modestly again, although the index is still substantially below its long-term average.

By the end of the week, German and French 10-year yields had both gained 7bps to 2.58% and 3.06% respectively. The Italian 10-year BTP yield increased by 8bps to 3.88% over the week while the British 10-year gilt yield finished 13bps higher at 4.36%.

The AOFM held two tenders this week. $300 million of June 2054s and $900 million of November 2028s were priced at yields of 4.60% and 3.97% respectively. There were also two Treasury note tenders which raised $2.0 billion on a short-term basis.

The gross value of all bonds issued by the AOFM in the 2023/2024 financial year (not taking into account short-term Treasury note tenders) is $39.70 billion. There are currently $826.65 billion of Treasury bonds and $40.585 billion of Treasury index-linked bonds on issue. The next series to mature does so on 21 November 2024 when $41.30 billion worth of bonds are due. There are also $26.00 billion of short-term Treasury notes outstanding.