Summary: 10-year bond yield up in Australia; ACGB 10-year spread to US Treasury yield rises to +9bps; 10-year bond yields up in US, major European markets; $2.8 billion of bonds, notes issued by AOFM.

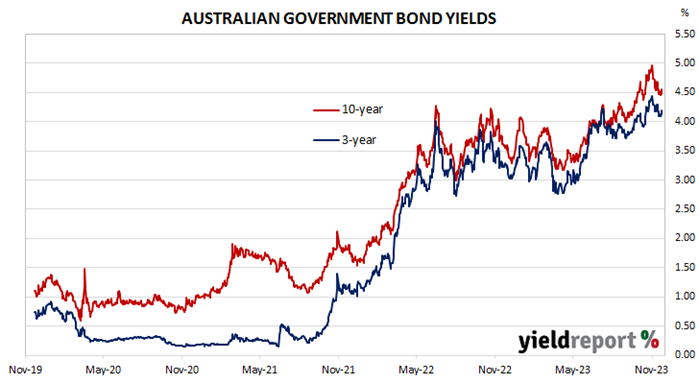

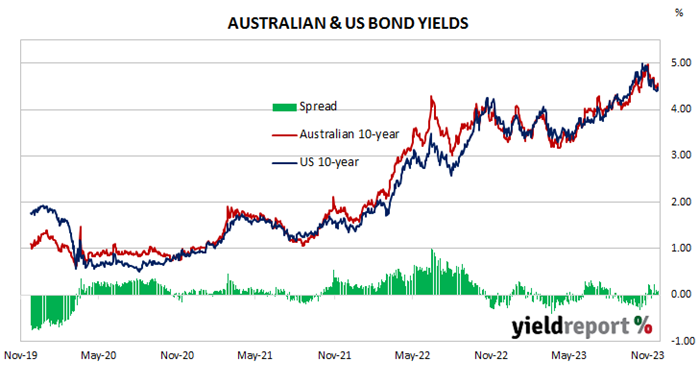

Locally, long-term ACGB yields rose moderately at the start of the week before falling noticeably the next day. Yields then rose until the end of the week. By this point, the 3-year ACGB yield had gained 11bps to 4.20%, the 10-year yield had added 9bps to 4.56% while the 20-year yield finished 3bps higher at 4.82%. The spread between US and Australian 10-year Treasury bond yields rose from 3bps to 9bps.

Over in the US, 10-year bond yields declined modestly for the first two days of the week and then rose a little before the Thanksgiving holiday. Yields then rose more noticeably at the end of the week.

The Conference Board’s October reading of its Leading Index posted a 0.8% fall at the start of the week, its eighteenth consecutive fall.

Minutes of the FOMC November meeting came out the next day.

S&P Global Market Intelligence’s latest flash reading of its composite index was released on Friday, with the index remaining steady at September’s final reading of 50.7. The manufacturing index declined from 50.0 to 49.4 while the services index gained 0.2 to 50.8.

The US Fed’s Nowcast model was also updated. The December quarter GDP growth forecast was lowered from 2.5% to 2.2% annualised, or a 0.5% expansion over the quarter.

By this point, the US 2-year Treasury bond yield had gained 5bps to 4.95%, the 10-year yield had added 3bps to 4.47% while the 30-year yield finished 1bp higher at 4.60%.

S&P Global Market Intelligence released its November flash PMI figures for the euro-zone on Thursday. The preliminary reading of the composite index was 47.1, up from October’s final reading of 46.5. “Over the last four to five months, the manufacturing and services sectors have both been experiencing a relatively constant contraction pace,” said Dr. Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank. “Considering the flash PMI numbers for November in our nowcast model indicates the potential for a second consecutive quarter of shrinking GDP.”

Germany’s ifo Institute released the November reading of its business climate index at the end of the week. The index increased for a third consecutive month as firms’ views of current conditions and the short-term outlook both improved.

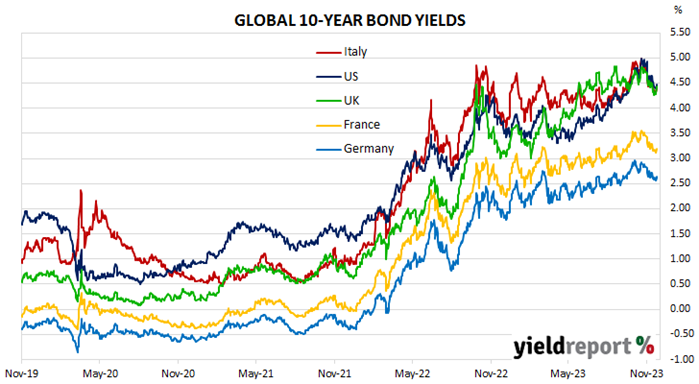

By this point, the German 10-year bund yield had gained 6bps to 2.64% and the French 10-year OAT yield had added 4bps to 3.20%. The Italian 10-year BTP yield increased by 3bps to 4.39% while the British 10-year gilt yield finished 17bps higher at 4.44%.

The AOFM held just the usual vanilla bond tender this week; $800 million of December 2034s were priced at a nominal yield of 4.45%. There were also two Treasury note tenders which raised $2.0 billion on a short-term basis.

The gross value of all bonds issued by the AOFM in the 2023/2024 financial year (not taking into account buy-backs or short-term Treasury note tenders) is $23.10 billion. There are currently $845.95 billion of Treasury bonds and $40.436 billion of Treasury index-linked bonds on issue. The next series to mature does so on 21 April 2024 when $35.90 billion worth of bonds are due. There are also $26.00 billion of short-term Treasury notes outstanding.