| Close | Previous Close | Change | |

|---|---|---|---|

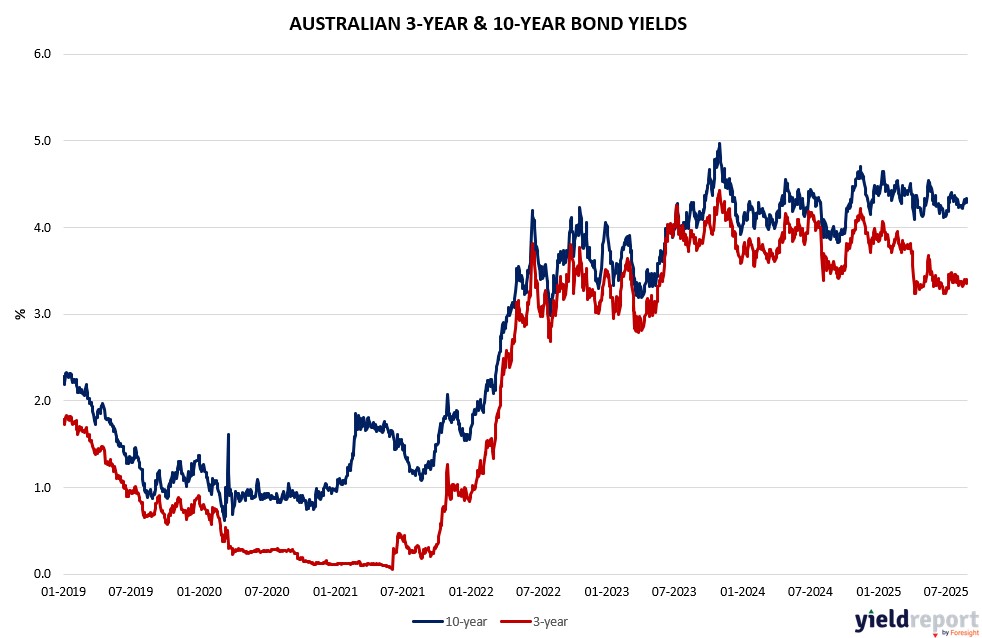

| Australian 3-year bond (%) | 3.37 | 3.4 | -0.03 |

| Australian 10-year bond (%) | 4.298 | 4.331 | -0.033 |

| Australian 30-year bond (%) | 5.048 | 5.088 | -0.04 |

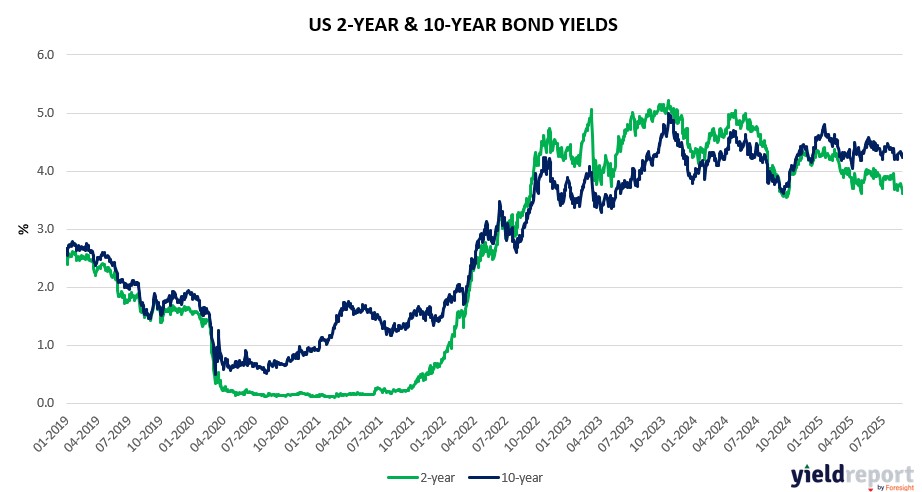

| United States 2-year bond (%) | 3.621 | 3.664 | -0.043 |

| United States 10-year bond (%) | 4.23 | 4.275 | -0.045 |

| United States 30-year bond (%) | 4.908 | 4.9295 | -0.0215 |

Overview of the Australian Bond Market

Australian government bonds rallied on August 28, 2025, with yields dropping across the curve as softer-than-expected capital expenditure data fueled rate cut speculation, countering resilient U.S. growth signals and ongoing global tariff uncertainties. The 10-year yield fell 5 basis points to 4.27%, the 2-year declined 4 bps to 3.32%, the 5-year dropped 4 bps to 3.63%, and the 15-year eased 6 bps to 4.64%. Month-to-date, yields have slid 5-10 bps, underscoring a dovish tilt amid domestic economic moderation.

The ABS’s Q2 capex rise of 0.2%—half a point below forecasts—reinforces the RBA’s cautious stance post-July’s 2.8% CPI jump, but signals potential for earlier easing if growth softens further, blending with bond buying. U.S. Q2 GDP upgraded to 3.3% (above 3.1% poll) and initial jobless claims at 229k (better than 230k) highlight economic strength, bolstering higher-for-longer rate views, yet President Trump’s push against Fed independence via Governor Cook’s ouster risks inflationary spillovers and erodes Treasury appeal, indirectly supporting Aussie bonds as a relative safe haven. Ongoing U.S.-China tariff truce negotiations (possible 90-day extension) and Europe-U.S. duty removals on industrial goods ease some trade fears, but India’s exposure to new duties adds caution. Bond positioning remains watchful ahead of tomorrow’s PCE data (core MM 0.3%, YY 2.9% expected), which could sway Fed September cut probabilities around 60% and influence RBA expectations via currency channels.

Overview of the US Bond Market

Short-maturity US Treasuries slipped on Thursday after stronger-than-expected economic data raised doubts about the extent of Federal Reserve rate cuts. Yields on two- to five-year notes climbed at least two basis points, with the two-year rising to 3.64% after GDP growth was revised up to 3.3% for Q2 and weekly jobless claims fell more than anticipated, signaling continued labor market strength. Analysts said the figures underscored consumer resilience despite tariff pressures, complicating the Fed’s dovish tilt.

Despite the move, shorter-dated yields remain near their lowest levels since early May, following a rally on growing expectations for policy easing. Swap contracts still price in a quarter-point Fed cut by October and a second by year-end, with about an 80% chance of a September reduction. Citigroup economists cautioned, however, that underlying demand outside a few sectors is weakening and that growth should slow further as tariffs weigh and labor conditions soften.

Political developments are also influencing expectations. President Donald Trump’s push to accelerate Fed appointments has bolstered market bets on cuts, with his nominee Miran expected to be confirmed before the September meeting.

Longer-dated Treasuries, in contrast, rallied after a seven-year note auction, sending yields to session lows and narrowing the yield curve. The two- to 10-year spread shrank to 57 basis points from 62, while the five- to 30-year gap fell to about 118 from 122. Recent steep curve levels prompted traders to unwind positions.

Auctions earlier this week also reflected strong demand: two- and five-year sales cleared at the lowest yields since September 2024, before rallying further in secondary markets. End-of-month bond index rebalancing, particularly large in August, also supported demand for new issues.

Overall, markets remain split between strong near-term data supporting higher yields and expectations that tariff-driven inflation and labor softness will push the Fed toward easing.

The US economy grew more strongly than initially estimated in the second quarter of 2025, with revised figures showing a 3.3% annualized expansion compared with the 3% originally reported. The upward revision was driven by robust business investment and a historic boost from trade. Business spending rose 5.7%, well above the prior estimate of 1.9%, with notable gains in transportation equipment and the strongest growth in intellectual property products in four years.

The trade sector provided an extraordinary lift, with net exports contributing nearly five percentage points to GDP, the largest on record after weighing on growth in the first quarter. This reflected both a rebound from earlier import surges tied to tariff anticipation and stronger overseas demand for US goods. Consumer spending, the backbone of the economy, grew at a modest 1.6%, slightly above initial estimates but still sluggish compared with past expansions. Retailers like Walmart and Home Depot remain optimistic about consumer resilience, though tariff-driven price increases are beginning to filter into stores.

Corporate profits improved in Q2, rising 1.7% after suffering their sharpest decline since 2020 earlier in the year. Margins, measured as after-tax profits for nonfinancial firms relative to gross value added, held steady at 15.7% although elevated by historical standards. Economists caution, however, that whether firms pass tariff costs to consumers or absorb them will shape profit trajectories and inflation pressures going forward.

Gross domestic income (GDI), an alternative gauge of economic activity, surged 4.8% in Q2 after barely growing in Q1, reinforcing the picture of stronger momentum. Still, analysts warn underlying demand outside specific sectors remains subdued, with labor market weakness and higher tariff costs likely to restrain activity in the months ahead. Final sales to private domestic purchasers, a cleaner measure of household and business demand, rose just 1.9%, suggesting slowing core momentum beneath the headline GDP figure.

Inflation dynamics remain central to the outlook. The Fed’s preferred core PCE index rose at 2.5% in Q2, unchanged from the earlier estimate. Policymakers are closely monitoring whether tariffs will further pressure prices. Chair Jerome Powell, speaking at Jackson Hole, acknowledged tariff-driven inflation but highlighted labor market risks as a potential justification for a September rate cut. Markets are still pricing in easing, with traders betting on at least one cut before year-end.

In addition to the GDP revision, the Commerce Department announced it will begin distributing GDP data via public blockchains, aligning with the Trump administration’s push for greater adoption of digital technologies. Meanwhile, labor market signals remain mixed, with jobless claims falling in mid-August even as concerns mount about broader hiring trends.