| Close | Previous Close | Change | |

|---|---|---|---|

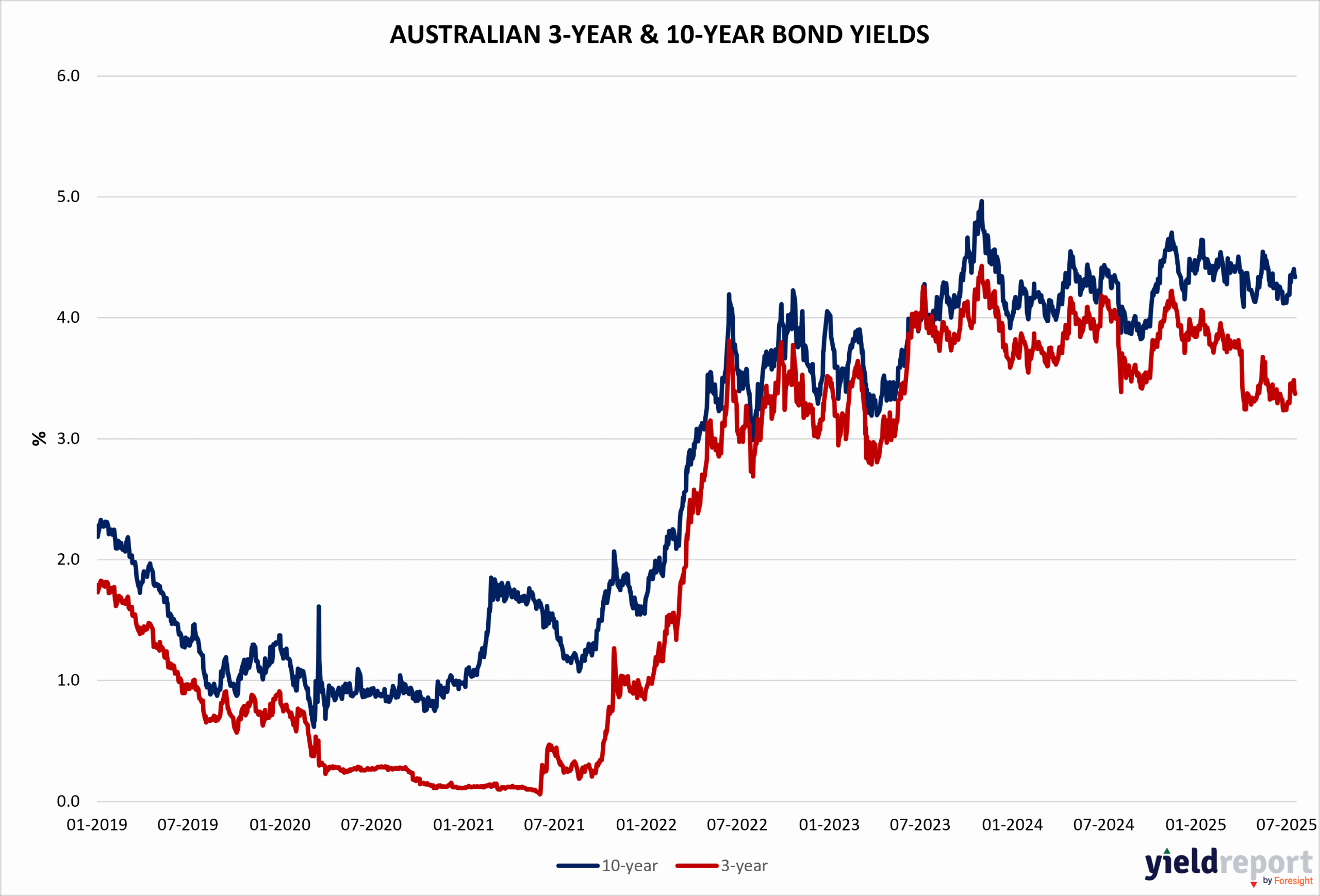

| Australian 3-year bond (%) | 3.362 | 3.362 | 0 |

| Australian 10-year bond (%) | 4.252 | 4.251 | 0.001 |

| Australian 30-year bond (%) | 4.978 | 4.975 | 0.003 |

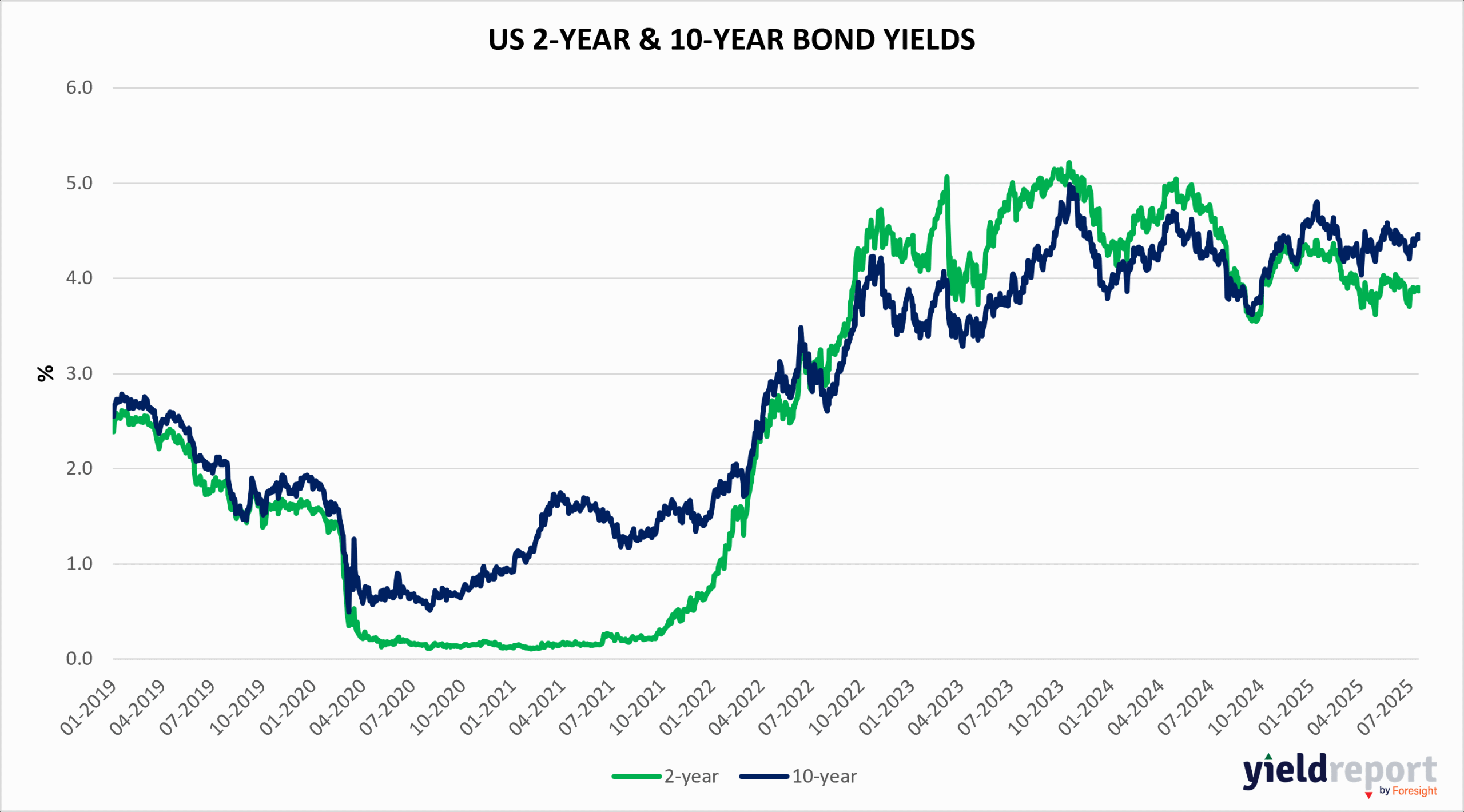

| United States 2-year bond (%) | 3.713 | 3.743 | -0.03 |

| United States 10-year bond (%) | 4.24 | 4.241 | -0.001 |

| United States 30-year bond (%) | 4.8191 | 4.8191 | 0 |

Overview of the Australian Bond Market

Australian government bond yields held steady on August 7, 2025, reflecting cautious market sentiment as investors awaited the RBA’s next moves. The 2-year yield remained at 3.34%, the 5-year at 3.64%, the 10-year at 4.25%, and the 15-year at 4.61%, with no daily changes recorded. Over the past month, yields have edged up, with the 10-year yield rising 7 basis points and the 15-year up 10 basis points, signaling persistent inflation concerns despite recent data showing Australia’s CPI stabilizing.

The robust trade surplus data released on August 7, showing exports up 6% and imports down 3.1% for June, has fueled speculation of an RBA rate cut as early as next week, though high bank valuations and margin pressures temper optimism for financial stocks. Meanwhile, global macro factors, including US-China tariff truce talks and a steady US Federal Reserve policy rate (4.25%–4.5%), continue to influence sentiment. The resilience of Australia’s economy, underscored by strong services (S&P Global Services PMI at 54.1) and composite PMI (53.8) readings for July, supports a cautiously optimistic outlook for bonds.

Bond traders are closely monitoring US developments, where Treasury yields dipped as markets priced in a 60% chance of a 25 basis-point Fed rate cut in September. Locally, the SPDR S&P/ASX Australian Bond Fund (BOND) showed muted performance, with no significant price movements reported, reflecting stable demand for fixed-rate bonds. With Australia’s economic indicators pointing to strength and global trade uncertainties easing, bond investors are maintaining balanced positions, though stretched equity valuations and potential tariff disruptions remain risks to watch.

Overview of the US Bond Market

Demand in a the 30-year auction declined a bit, fueling concerns sparked by yesterday’s lukewarm reception for 10-year notes. The bid-to-cover ratio of 2.27 was below the 2.38 six-month average, a narrower gap than seen in yesterday’s sale. Participation from indirect bidders, a group that includes foreign buyers, was little changed from July. High yield was 4.813%. The 30-year treasury yield rose to 4.8% from 4.79% right before the auction. Other maturities followed a similar pattern.

Markets fear investors may be growing reluctant to finance the U.S. budget. Meanwhile, jobless claims increase, supporting suspicions that the labor market could be cooling fast. Increased productivity in the 2Q is seen as a deflationary factor, supporting odds of an interest rate cut in September. Wall Street is already focusing on July CPI, due Tuesday. Signs of tariff-driven price increases are expected. The 10 US Treasury Bond yield rose 0.011 percentage point to 4.243% and the two year bonds added 0.032 p.p. to 3.732%.

Elsewhere, increases in U.K. government bond yields have largely been influenced by global developments, rather than domestic factors, the Bank of England says. Gilt yields have risen considerably from the levels in 2021, mainly due to subsequent interest-rate increases by the BOE but also due to concerns about the longer-term economic and fiscal outlooks. This trend has been evident globally as well as in the U.K., the BOE says. Higher gilt yields “partly reflects the impact of international developments, which can have a large influence on U.K. government bond yields,” it says. Thirty-year gilt yields hit their highest since the late 1990s in April after U.S. President Trump announced sweeping trade tariffs.