| Close | Previous Close | Change | |

|---|---|---|---|

| Australian 3-year bond (%) | 3.384 | 3.37 | 0.014 |

| Australian 10-year bond (%) | 4.296 | 4.298 | -0.002 |

| Australian 30-year bond (%) | 5.307 | 5.048 | 0.259 |

| United States 2-year bond (%) | 3.633 | 3.621 | 0.012 |

| United States 10-year bond (%) | 4.211 | 4.23 | -0.019 |

| United States 30-year bond (%) | 4.8836 | 4.908 | -0.0244 |

Overview of the Australian Bond Market

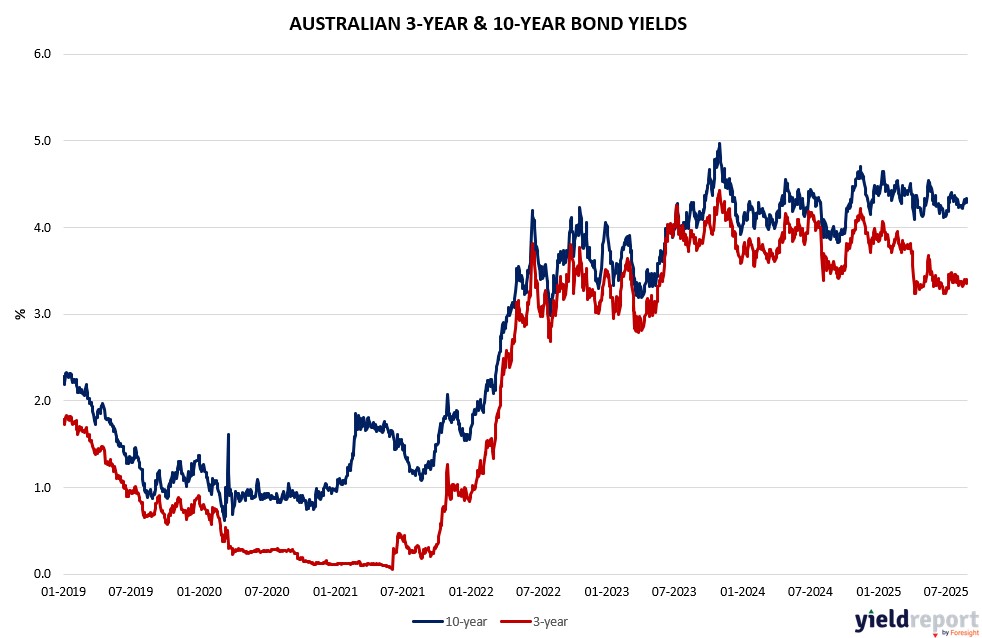

Australian government bonds were mixed on August 29, 2025, with yields edging slightly higher at the short end amid U.S. inflation alignment and global equity jitters, as earnings season wrapped and monthly gains solidified. The 10-year yield dipped 1 basis point to 4.27%, the 2-year rose 1 bp to 3.33%, the 5-year held at 3.64%, and the 15-year eased 2 bps to 4.64%. Month-to-date, yields declined 5-7 bps, reflecting dovish sentiment post-softer Q2 capex (0.2% vs. 0.7% expected) and July CPI surprise, though August’s equity rally tempers aggressive RBA cut bets.

U.S. PCE meeting forecasts—core YY at 2.9%, supporting Fed’s easing path—bolstered resilience views but fueled a tech-led selloff, amplifying tariff truce talks (U.S.-China extension eyed) and European duty reductions, potentially stabilizing flows yet heightening September correction risks from valuations and U.S. debt. Trump’s Fed independence challenge risks higher global borrowing costs, indirectly pressuring Aussie yields via commodity ties, as lithium and uranium surges highlight supply constraints. Bond traders eye next week’s jobless claims (230k expected) and Australia’s leading index for further RBA clues, with swaps implying ~60% September Fed cut chance influencing cross-currency dynamics.

Overview of the US Bond Market

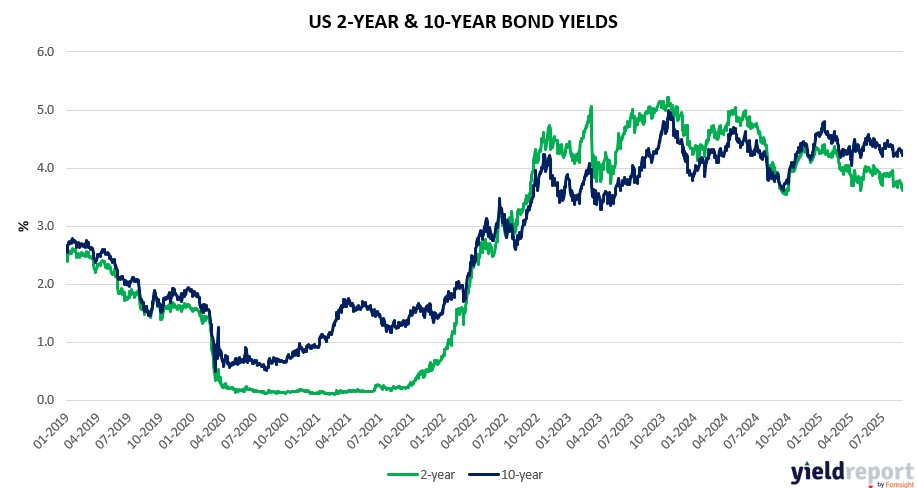

Bond traders pared aggressive easing bets on August 29, 2025, as in-line PCE data affirmed Fed caution, with yields dipping modestly amid end-of-month positioning and global policy jitters. The 10-year yield fell 14 basis points month-to-date to 4.23%, the 2-year dropped 32 bps to 3.62%, the 5-year eased 27 bps to 3.70%, and the 30-year rose 3 bps to 4.93%. Shorter maturities like the 3-month bill yield declined 20 bps to 4.14%, reflecting resilient growth signals.

A Treasuries rally moderated after solid auctions, with longer-dated bonds trimming gains as President Trump’s Fed interference—attempting to oust Governor Lisa Cook—fuels fears of politicized policy, potentially spiking inflation and borrowing costs globally. Treasury Secretary Scott Bessent noted ongoing U.S.-China tariff truce talks, with a 90-day extension option, amid European duty cuts, easing some trade war pressures but highlighting “significant political risk” in US assets per international managers.

On the economic front, PCE inflation matched forecasts—core YY at 2.9%—bolstering higher-for-longer views, while Q2 GDP at 3.3% and jobless claims at 229k underscore resilience against Trump’s agenda, including BLS overhaul risking data trust. JPMorgan’s client survey likely shows shrinking net longs ahead of September’s meeting, with swaps pricing a 60% chance of a 25 bps cut.

This shift reflects countervailing forces: Fed independence threats from Trump may invite dissent, edging yields lower short-term, but fiscal profligacy—worsened by tax cuts and deficits—threatens sustained pressure as deals with EU and Japan dissipate uncertainty. Asset managers trimmed longs across tenors per CFTC data, while leveraged funds pared shorts in longer bonds.

US government bond dealers expect steady coupon auction sizes for August-October, per April guidance, with 10- and 5-year issues up $1 billion.