| Close | Previous Close | Change | |

|---|---|---|---|

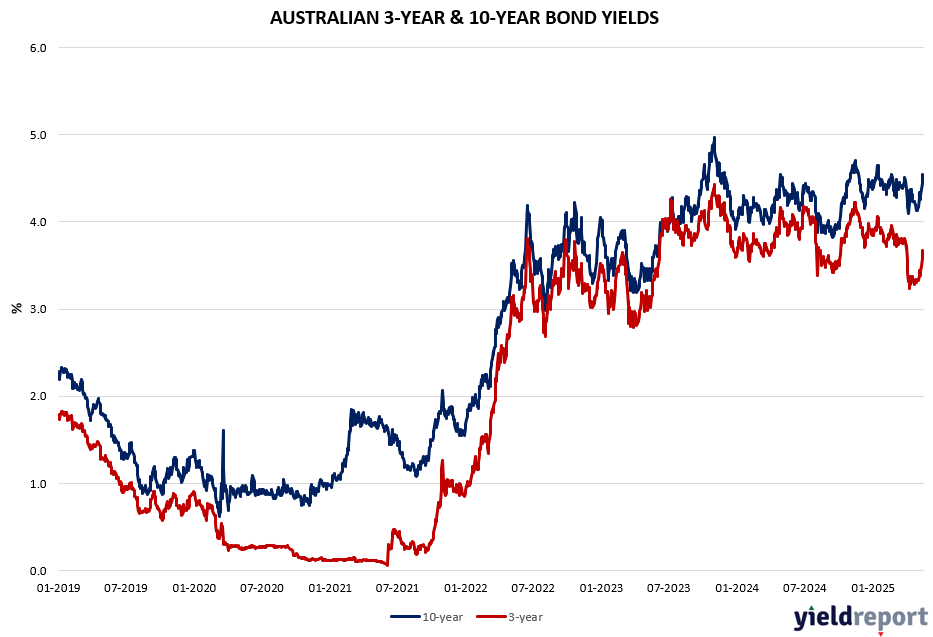

| Australian 3-year bond (%) | 3.629 | 3.676 | -0.047 |

| Australian 10-year bond (%) | 4.475 | 4.546 | -0.071 |

| Australian 30-year bond (%) | 5.111 | 5.169 | -0.058 |

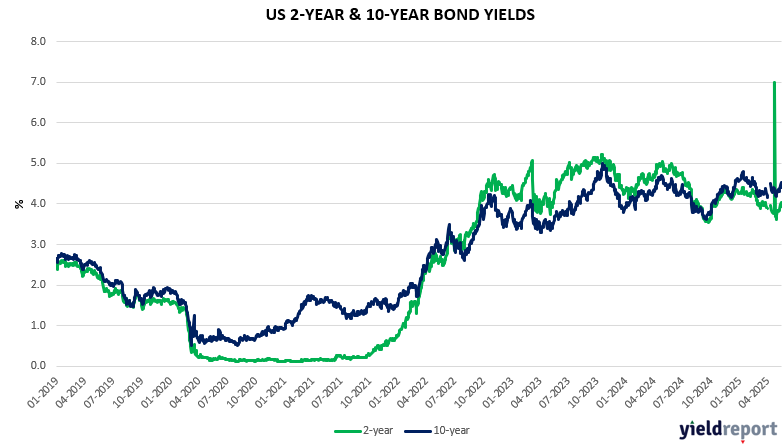

| United States 2-year bond (%) | 3.9446 | 4.028 | -0.0834 |

| United States 10-year bond (%) | 4.4079 | 4.517 | -0.1091 |

| United States 30-year bond (%) | 4.8695 | 4.957 | -0.0875 |

LOCAL BOND MARKETS

Australian bond traders shrugged off stronger-than-expected labour force data on Thursday and doubled down on bets the Reserve Bank of Australia will cut the policy rate on Tuesday. In good news for equities, money markets are almost fully priced for a quarter-point rate cut.

About 89,000 people found work in April, the Australian Bureau of Statistics said on Thursday, beating expectations for modest gains of 22,500. Despite the unexpectedly strong rise in employment, the unemployment rate held steady at 4.1 per cent as the share of the working-age population with a job or looking for one climbed to a near-record high of 67.1 per cent. Financial markets are almost certain the RBA board will cut the cash rate to 3.85% from 4.1% when it meets next Monday and Tuesday, amid little evidence that low unemployment is causing unsustainable wage pressures. But economists said the jobs figures reinforced the Reserve Bank’s view that the labour market was either stabilising or strengthening, creating the possibility that inflationary pressures could re-emerge.

Meanwhile, former RBA board member Warwick McKibbin said Australia’s “very large” fiscal stimulus at a time when monetary policy is around neutral — neither stimulating nor slowing economic activity — suggests the RBA should keep interest rates unchanged next week.

US BOND MARKETS

The yield on the 10-year US Treasury was at 4.45%, inching lower from the three-month high of 4.55% touched earlier this session as wholesale costs in the US fell for a second month. The headline producer price index dropped by 0.5% in April, aligned with the softer trend for consumer inflation. Also, the control group for retail sales unexpectedly contracted as consumers heeded to tariffs. Still, yields remained over 35bps higher since the start of the month as improved trade flows lifted the outlook for growth and interest rates.

The US and China jointly lowered their tariffs against each other for the next 90 days to ease concerns that trade barriers would cause a recession, triggering a sharp rebound in risk sentiment and long-dated US Treasury yields. Consequently, rate traders reconsidered positions that reflected aggressive easing by the Federal Reserve this year, moving to price two rate cuts by December instead of four cuts priced last week.