| Name | Daily Close | Daily Change | Daily Change (%) |

|---|---|---|---|

| Dow | 46,519.72 | 78.62 | 0.17% |

| S&P 500 | 6,715.35 | 4.15 | 0.06% |

| Nasdaq | 22,844.05 | 88.89 | 0.39% |

| VIX | 16.28 | -0.35 | -2.10% |

| Gold | 3,885.60 | 17.5 | 0.45% |

| Oil | 60.95 | 0.47 | 0.78% |

OVERVIEW OF THE US MARKET

Wall Street closed mixed on October 3, 2025, as a late-day selloff in technology shares offset gains in health care and utilities amid ongoing concerns over the US government shutdown and delayed economic data. The S&P 500 eked out a fractional gain of 0.01%, while the Nasdaq Composite fell 0.28% and the Dow Jones Industrial Average rose 0.51%. Health care stocks led advancers, with the sector up 1.13% on resilient earnings prospects, but big tech names like Palantir tumbled 7.5% after reports of flaws in its systems, pulling the information technology sector down 0.32%.

Plug Power surged 34.63% amid renewed interest in alternative energy, while Lithium Americas jumped 31.78% on commodity strength. Snap rose 3.89%, but Rocket Companies slid 3.10%. The market shrugged off stalled service-sector activity from ISM data, with swaps traders still pricing in a quarter-point Fed cut in October despite the data blackout from the shutdown. President Donald Trump’s warnings on Hamas and plans to lay off government workers added to uncertainty, though Hamas’s partial agreement to terms eased some geopolitical tensions.

Bitcoin hit a new all-time high above $125,000, fueled by the “debasement trade” narrative around the shutdown and safe-haven flows, extending its year-to-date gain to over 30%. In corporate news, Rivian reworked vehicle designs over safety concerns, and Boeing delayed its 777X launch to 2027, potentially facing billions in charges. AI enthusiasm persisted with deals like Global Infrastructure Partners eyeing Aligned Data Centers at $40 billion, but warnings of a trillion-dollar bubble grew, with Bain & Co. forecasting a revenue shortfall for AI firms by 2030.

Consumer confidence data earlier in the week showed a slight dip to 94.2 in September, below expectations, while ISM manufacturing PMI edged up to 49.1, signaling contraction but better than forecast. Investors are eyeing delayed nonfarm payrolls, now expected Friday amid the shutdown, with polls anticipating 50,000 job ads and a steady 4.3% unemployment rate.

OVERVIEW OF THE AUSTRALIAN MARKET

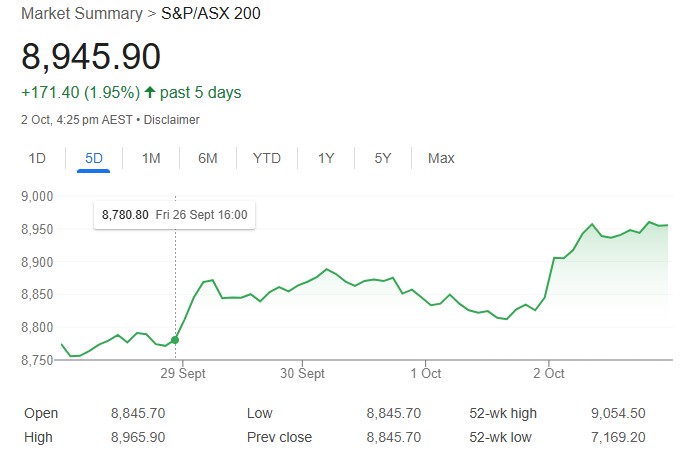

Australia’s share market closed higher on October 3, 2025, nearing record highs as positive US cues and resilient economic data boosted sentiment despite softer building approvals. The S&P/ASX 200 rose 0.46% to 8,987.4, while the All Ordinaries gained 0.52% to 9,288.1. Information technology led with a 1.63% advance, mirroring Nasdaq rebounds, followed by health care up 1.04% and consumer discretionary up 1.02%.

Finder Energy surged 31.0% on performance rights vesting, Cettire rose 27.3% in its uptrend, and European Lithium jumped 22.2% after announcing a share buy-back. Clarity Pharmaceuticals climbed 19.3% on upcoming data presentations, but Race Oncology fell 12.6% after a sharp prior rally. The market benefited from a “Goldilocks” scenario of stronger private-sector growth justifying fewer rate cuts, with the index up 2.3% for the week.

Building approvals dropped 6% in August, worse than the 3% poll, while goods exports fell 7.8%, dragging the trade surplus to A$1.825 billion, below expectations. RBA held its cash rate at 3.6%, and S&P Global manufacturing PMI finalized at 51.4, indicating expansion. The Aussie dollar edged up to 0.6602 against the US dollar.