| Name | Price | Change | % Chg |

|---|---|---|---|

| Dow | 46,602.98 | -91.99 | -0.20% |

| S&P 500 | 6,714.59 | -25.69 | -0.38% |

| Nasdaq | 22,788.36 | -153.3 | -0.67% |

| VIX | 17.24 | 0.87 | 5.31% |

| Gold | 4,013.60 | 9.2 | 0.23% |

| Oil | 62.15 | 0.42 | 0.68% |

OVERVIEW OF THE US MARKET

Wall Street closed lower on October 7, 2025, as concerns over buyer exhaustion and stretched valuations in the tech sector weighed on sentiment following a $16 trillion surge in the S&P 500 from April lows. The S&P 500 slipped 0.38% to 6,714.59, the Nasdaq Composite fell 0.67% to 22,788.36, and the Dow Jones Industrial Average declined 0.20% to 46,602.98. Tech giants like Oracle, which dropped 2.5% amid reports of lower-than-expected cloud margins, and Tesla, down 4.4% after unveiling new models under $40,000, dragged on the indices. Dell Technologies bucked the trend, climbing 3.5% on raised estimates driven by AI demand.

Sector performance was mixed, with consumer staples up 0.86% and utilities gaining 0.42%, while consumer discretionary sank 1.43% and communication services lost 0.73%. Active stocks included Connexa Sports Technologies plunging 92.83% on heavy volume, and Trilogy Metals soaring 211% amid market volatility. Investors parsed Fed comments, with Governor Stephen Miran advocating for forward-looking easing despite tariff risks, while Minneapolis Fed President Neel Kashkari cautioned against aggressive cuts to avoid inflation spikes.

Dot-com bubble fears resurfaced as AMD extended gains from an OpenAI deal, adding to concerns of circular AI investments and rapid market cap swings exceeding $100 billion. Strategists at Citigroup noted elevated profit-taking risks, particularly for Nasdaq, while Piper Sandler highlighted diverging momentum but remained optimistic on macro tailwinds. JPMorgan’s Jamie Dimon emphasized AI’s cost savings potential, matching annual investments at $2 billion.

Corporate highlights included IBM integrating Anthropic’s AI tech, Salesforce refusing a hacker’s ransom demand, and DraftKings falling on NYSE’s Polymarket investment news. Johnson & Johnson faced a $966 million verdict over baby powder litigation. Looking ahead, traders eye Thursday’s non-farm payrolls, expected at 50,000 jobs added with unemployment steady at 4.3%, which could influence Fed rate cut bets amid ongoing shutdown tensions where President Trump signaled potential blocks on back pay for some furloughed workers.

OVERVIEW OF THE AUSTRALIAN MARKET

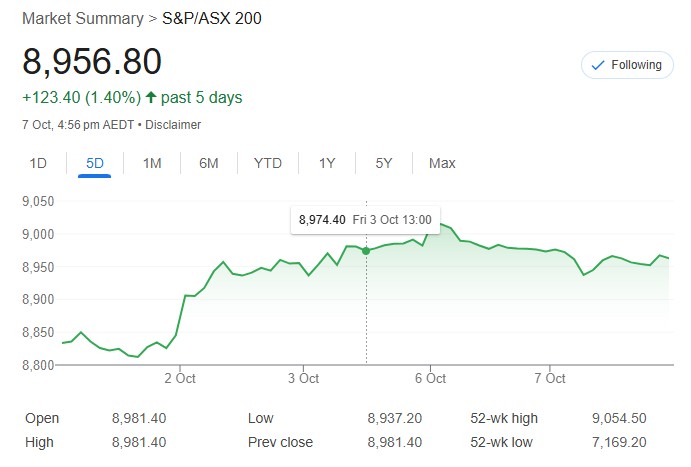

Australia’s share market closed lower on October 7, 2025, extending losses for a second session as rate-sensitive sectors faced pressure from rising bond yields and muted economic data. The S&P/ASX 200 fell 0.27% to 8,956.8, while the All Ordinaries dropped 0.28% to 9,253.6. Consumer discretionary led declines at 1.16%, followed by communication services down 1.08% and real estate off 0.46%, with REA Group sliding 2.1% and Car Group tumbling 3.8%. Materials eked out a 0.05% gain, buoyed by miners like Rio Tinto up 0.5% on a West Angelas extension.

Gold miners showed resilience as spot gold rose 0.5% to $3,981.41 an ounce, with Greatland Gold surging 9.6% on a quarterly update. Small caps outperformed, with the Small Ordinaries up 0.12%, highlighting a bull market divergence from large caps hesitant near 9,000. Westpac consumer sentiment dropped 3.5% to 92.1 in October, and ANZ job ads fell 3.3% month-over-month in September, underscoring caution on rate cuts.

Standouts included Ionic Rare Earths jumping 29.4% on critical minerals strength and Ioneer up 22.2% following US lithium project investment. Laggards featured European Lithium down 34% after a share sale and Brisbane Broncos dropping 16% post-rally. ASX fell 1.3% on Cboe’s listing approval, while CBA dipped 0.3% amid a NZ subsidiary settlement.

With China markets closed for holidays, focus shifts to Wednesday’s expected 25 basis point cut by New Zealand’s central bank to 2.75%, potentially influencing Aussie rate expectations.