| Name | Price | Change | % Chg |

|---|---|---|---|

| Dow | 45,544.88 | -92.02 | -0.20% |

| S&P 500 | 6,460.26 | -41.6 | -0.64% |

| Nasdaq | 21,455.55 | -249.61 | -1.15% |

| VIX | 15.36 | 0.93 | 6.44% |

| Gold | 3,552.10 | 36 | 1.02% |

| Oil | 64.8 | 0.79 | 1.23% |

OVERVIEW OF THE US MARKET

Asian markets entered Tuesday on a cautious note, with attention focused on technology stocks and China after a sharp rally in Alibaba. Futures suggested modest gains for Japan, while contracts for Hong Kong and Australia pointed to muted moves. U.S. equity futures edged lower, with cash markets closed for Labor Day. Investors are also watching Japan’s 10-year bond auction amid speculation about Bank of Japan rate hikes and rising political uncertainty. Oil prices climbed, while the dollar remained flat.

Wall Street faces an important stretch, with payrolls, inflation, and the Federal Reserve’s September policy decision looming. Deutsche Bank noted the bar is high for the Fed to avoid cutting on September 17, though futures pricing suggests markets expect recession-level easing through 2026.

In Asia, sentiment improved as the MSCI Emerging Markets Index rose 0.7%, its best day in a week, led by Hong Kong-listed Alibaba, which surged 19% on strong AI-related revenues and cloud sales. This helped offset last week’s regional weakness following U.S. tech losses. However, Indonesian markets slumped, with equities recording their steepest drop in nearly five months, and bond yields spiking amid domestic unrest and political risks tied to President Prabowo Subianto canceling a China trip.

Geopolitical developments also loomed, with President Xi Jinping preparing to showcase China’s military and diplomatic strength at a parade marking World War II’s end, while U.S. President Trump said India agreed to lower tariffs following Washington’s recent levies on Russian oil-linked imports.

In Europe, political uncertainty persisted ahead of a French confidence vote, keeping the French-German 10-year spread near multi-month highs. Historically, September is the weakest month for long-dated government bonds, with median global losses of 2% over the past decade.

Corporate headlines added intrigue: Nestlé ousted CEO Laurent Freixe over a workplace affair, extending management turbulence. Meanwhile, Mizuho Financial Group outlined ambitions to dominate Asian investment banking by expanding equity and M&A services, building on U.S. momentum.

Market snapshots reflected caution: S&P 500 and Australian futures were steady, Hang Seng futures slipped, and major currencies held flat. Bitcoin fell slightly, ether ticked up, and WTI crude gained nearly 1% to $64.57. Gold was little changed, while bond yields rose modestly in Australia.

Overall, Asian markets opened subdued but closely tied to tech momentum, political risks, and looming global central bank decisions.

OVERVIEW OF THE AUSTRALIAN MARKET

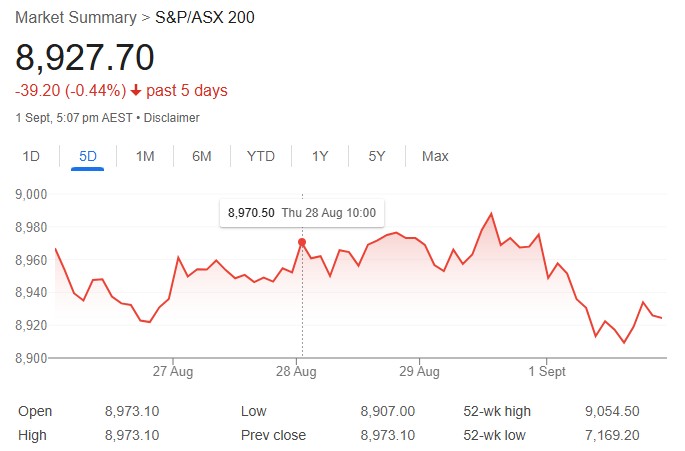

The Australian share market started September on the wrong foot on September 1, 2025, dragged by banks, miners, and tech amid global cues and a Trump post boosting gold, as investors parsed the volatile August earnings wrap-up.

The S&P/ASX 200 fell 0.51% to 8,927.7, 0.51% from its high and 0.21% from the low, while the broader All Ordinaries dropped 0.50% to 9,196.8. Small-caps bucked the trend with the Small Ords up 0.57%, though breadth leaned negative with advancers lagging decliners 114 to 163 in the ASX 300.

Consumer Staples edged up 0.35%, Communication Services gained 0.31%, and Utilities rose 0.30%, but Information Technology plunged 2.65% as Xero (-4.0%) and Wisetech Global (-3.4%) weighed. Consumer Discretionary fell 1.24% with Bapcor (-6.7%), Cettire (-6.3%), and Domino’s Pizza (-3.0%) in entrenched downtrends. Financials dropped 0.75%, led by big banks: CBA (-0.8%), NAB (-0.6%), Westpac (-0.9%), ANZ (-0.3%). Materials added 0.14% amid gold’s surge to $US3,552 all-time high after Trump’s inflation post, powering the Gold subsector (+5.8%)—Northern Star (+6.4%), Evolution Mining (+5.1%), Genesis Minerals (+11.5%), Capricorn Metals (+11.7%), Black Cat Syndicate (+11.7%).

Standout movers included 4DMedical (+36.0%) on FDA clearance, Rpmglobal (+22.8%) after NBIO from Caterpillar, Caprice Resources (+19.8%), Silver Mines (+16.7%), Mithril Resources (+15.3%), Rox Resources (+14.1%), Meeka Metals (+13.8%), Kaiser Reef (+13.2%), Fenix Resources (+10.9%), Unico Silver (+10.3%), Lotus Resources (+10.0%), Greatland Gold (+10.0%), Betmakers Technology Group (+9.7%), Andean Silver (+9.2%), Waratah Minerals (+9.1%), St George Mining (+8.9%), Polymetals Resources (+8.6%), St Barbara (+8.6%), Harvey Norman (+8.6%), Catalyst Metals (+8.6%), Sun Silver (+8.1%), Benz Mining (+8.0%), Westgold Resources (+7.8%), Alkane Resources (+7.1%), EDU (+7.1%), Ausgold (+7.1%), Resolute Mining (+7.0%), West Coast Silver (+6.8%), Vault Minerals (+6.5%), Ora Banda Mining (+6.5%). Laggards featured Energy Transition Minerals (-16.7%), EZZ Life Science (-13.6%), Dateline Resources (-13.2%), Green Critical Minerals (-11.1%), Lindian Resources (-9.1%), Generation Development Group (-8.7%), Bubs Australia (-8.3%), Mesoblast (-7.3%), Perpetual (-6.4%), Kina Securities (-6.3%).

The AUD/USD rose 0.05% to 0.6544.

August S&P Global Manufacturing PMI finalized at 53, signaling expansion, but building approvals dropped 8.2% in July (worse than -4% forecast). For August, the ASX 200 rose 2.6%—its best month since May’s 3.8%—fueled by strong sectors and earnings beats amid global volatility, though September seasonality and US tariff risks loom.

President Trump’s post claiming low US inflation spurred gold’s rally, indirectly lifting Aussie miners, but broader markets eyed Fed independence threats and tariff extensions.

Strategists note resilient earnings and AI tailwinds could propel gains, but Goldman Sachs warns tariffs may hurt even with deals, urging diversification amid high valuations.