| Name | Daily Close | Daily Change | Daily Change (%) |

|---|---|---|---|

| Dow | 44401.93 | -240.59 | -0.54% |

| S&P 500 | 6052.85 | -37.42 | -0.61% |

| Nasdaq | 19736.69 | -123.08 | -0.62% |

| VIX | 14.19 | 1.42 | 11.12% |

| Gold | 2683.00 | 23.40 | 0.88% |

| Oil | 68.15 | 0.95 | 1.41% |

US MARKET

The S&P 500 pulled back from overbought levels after reaching record highs, driven by a sell-off in Nvidia following a Chinese anti-monopoly probe. U.S.-listed Chinese stocks surged as Beijing signalled stronger monetary easing and support for domestic consumption. Key inflation data due Wednesday could influence the Federal Reserve’s upcoming policy decision, with concerns that a surprise uptick may halt recent rate cuts. However, favorable technicals and seasonal trends continue to support equity gains.

Market outlooks vary, with Oppenheimer Asset Management projecting the S&P 500 to reach 7,100 by the end of 2024, while Citigroup predicts modest mid-single-digit gains for 2025 amid heightened volatility. Seasonal trends and post-election optimism are driving equities higher, supported by resilient economic data. Hedge funds have increased net buying, particularly in technology stocks, although industrials faced significant short selling.

Corporate developments include Macy’s facing activist investor pressure, Mondelez exploring a Hershey acquisition, and MicroStrategy continuing its aggressive Bitcoin purchases. Apollo Global Management and Workday are joining the S&P 500, replacing Qorvo and Amentum. Warner Bros. Discovery renewed its Comcast deal, while Nippon Steel clarified its U.S. investment plans, highlighting ongoing shifts in major sectors.

LOCAL MARKET

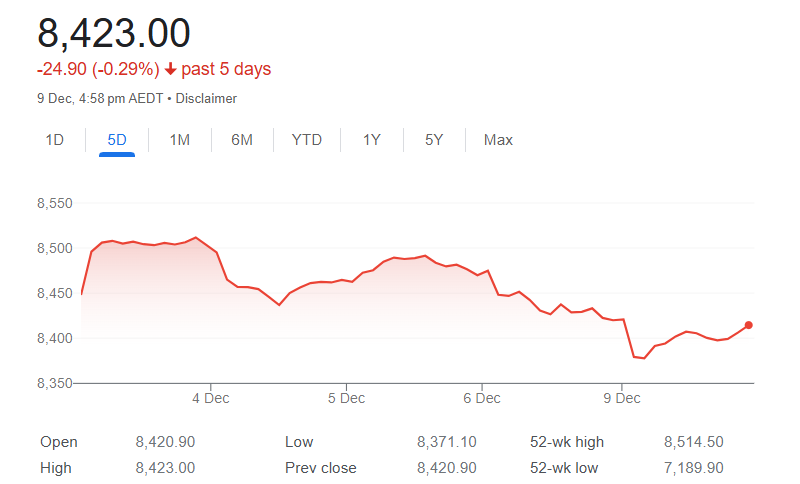

The Australian share market is set to edge higher today, with ASX futures up by 3 points to 8447 points, driven by a rally in commodity prices. This optimism follows China’s announcement of plans to implement stronger economic support measures. However, gains were tempered by a late sell-off in the U.S. technology sector as traders reacted to news of a Chinese probe into Nvidia, which dampened sentiment on Wall Street.

China’s Politburo has fuelled market optimism by signalling a “moderately loose” monetary policy and a “more proactive” fiscal approach for 2024. The Australian dollar and commodity prices, including iron ore and base metals, saw a notable rise of more than 1% following the announcement. These measures, which include the potential widening of China’s fiscal deficit beyond 3%, are expected to be reinforced at the upcoming Central Economic Work Conference, with analysts forecasting more concrete demand-side stimulus measures early next year.

In domestic developments, the Reserve Bank of Australia is expected to hold the cash rate steady at 4.35% for the ninth consecutive meeting. Meanwhile, specific stocks are drawing attention, including Myer, which is holding its annual general meeting, and Premier Investments, trading ex-dividend. IAG has announced plans to defend itself against a class-action lawsuit, while Platinum Asset Management remains in focus after its stock plummeted more than 14% due to a failed takeover deal with Regal Partners. Additionally, Perpetual faces a potential increase in its tax obligations after a query by the Australian Tax Office regarding its asset sale to private equity firm KKR.