| Name | Price | Change | % Chg |

|---|---|---|---|

| Dow | 43,968.64 | -224.48 | -0.51% |

| S&P 500 | 6,340.00 | -5.06 | -0.08% |

| Nasdaq | 21,242.70 | 73.27 | 0.35% |

| VIX | 16.57 | -0.2 | -1.19% |

| Gold | 3,400.90 | 1.9 | 0.06% |

| Oil | 63.15 | -0.02 | -0.03% |

OVERVIEW OF THE US MARKET

All major US equity indexes climbed more than 1%, with the S&P 500 and the Nasdaq 100 hitting all-time highs. The Russell 2000 of smaller firms jumped 3%.

Underlying US inflation accelerated in July though the cost of tariff-exposed goods didn’t rise as much as feared, boosting expectations that Federal Reserve officials will lower interest rates when they meet next month.

The core consumer price index, which excludes the often volatile food and energy categories, increased 0.3% from June, the strongest pace since the start of the year, according to Bureau of Labor Statistics data out Tuesday. That was in line with economists’ forecasts, as was the overall CPI on a monthly basis.

Sentiment among US small businesses climbed to a five-month high in July as owners grew more upbeat about the economic outlook, fueling a pickup in expansion plans.

The National Federation of Independent Business optimism index increased 1.7 points last month to 100.3, according to data out Tuesday. Six of the 10 components that make up the gauge improved.

A net 36% of owners expect better business conditions, up 14 percentage points from a month earlier and the most this year. A net 16% said now is a good time to expand their business, the largest share since January.

The S&P 500 enjoyed broad-based gains, buoyed by market optimism over potential Federal Reserve interest rate cuts.

All eleven sectors closed higher, with Energy leading the pack, rising around 0.8%.

Airlines and Banks also posted strong gains as transportation costs surged and hopes for cheaper borrowing rose. Technology and Semiconductors performed particularly well, powered by big tech and favorable earnings.

OVERVIEW OF THE AUSTRALIAN MARKET

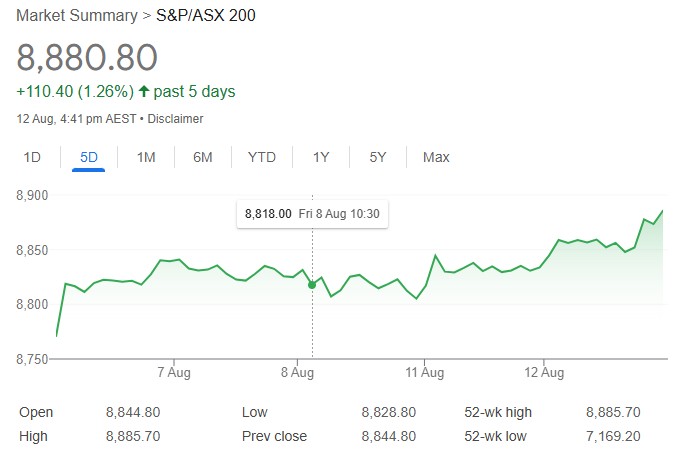

Australia’s share market soared to record highs on August 12, 2025, buoyed by the Reserve Bank of Australia’s third interest rate cut of the year, which lifted banks, consumer stocks, and overall sentiment. The S&P/ASX 200 climbed 0.41%, or 36 points, to 8,880.8, while the broader All Ordinaries rose 0.36% to 9,150.3. Despite the benchmark’s strength, market breadth was narrow, with advancers edging decliners 138 to 134 on the S&P/ASX 300—the second consecutive record-setting day without a decisive majority of winners.

The rally was driven by a classic formula: strong banks plus big resources. Eight of 11 sectors advanced, led by utilities (+0.84%), consumer discretionary (+0.83%), and financials (+0.83%). Communication services (+0.49%) and materials (+0.37%) also contributed, while industrials lagged with a 0.85% decline. The big four banks powered financials higher: ANZ surged 2.2% to $31.93, NAB and Westpac each gained 1% to $39.19 and $34.63, and CBA edged up 0.1% to $178.80 ahead of its full-year earnings on August 13. In materials, BHP rose 1% to $41.26, Rio Tinto added 1.2% to $116.72, and Fortescue climbed 1.2% to $19.66.

Standout performers included Lindian Resources (+37.0%) on continued positive momentum, Tuas (+29.6%) after completing an institutional placement, and The Star Entertainment Group (+23.6%) following a binding deal for its Queen’s Wharf stake. Rebounds in recent laggards boosted the index: JB Hi-Fi (+5.6%) recovered from Monday’s selloff, Light & Wonder (+6.0%) on ownership changes, and QBE Insurance (+2.1%). On the downside, Ioneer (-10.7%) and Liontown Resources (-8.0%) pulled back sharply after Monday’s lithium surge, though Pilbara Minerals (-0.87%) held a net 29% gain over three days. Gold stocks dipped 0.35% as prices fell on reports that gold would escape US tariffs.

The RBA’s unanimous 25 basis-point cut to 3.60% met unanimous economist expectations, with the board citing inflation near target but emphasizing caution amid high uncertainty and readiness to respond. Governor Michelle Bullock stressed a data-dependent approach in her press conference, noting forecasts include “a couple of more cash rate cuts” but no fixed endpoint, as the bank absorbs incoming data like July’s resilient PMIs (Services at 54.1) and June’s strong trade surplus (AUD 5,365 million). US CPI data released overnight aligned with polls (core monthly at 0.3%, headline yearly at 2.7%), reinforcing Fed cut expectations and global easing tailwinds.

AMP chief economist Shane Oliver views the cuts as share-positive if recession is averted, boosting profit growth and making equities more attractive than cash, though he warns of volatility from stretched valuations and President Trump’s trade wars. Investors now watch August 13’s Wage Price Index (poll 0.8% quarterly), which could signal wage pressures and influence further RBA moves.