| Name | Daily Close | Daily Change | Daily Change (%) |

|---|---|---|---|

| Dow | 42,410.10 | 1160.72 | 2.81% |

| S&P 500 | 5,844.19 | 184.28 | 3.26% |

| Nasdaq | 18,708.34 | 779.43 | 4.35% |

| VIX | 18.58 | 0.16 | 0.82% |

| Gold | 3,259.00 | 31.3 | 0.95% |

| Oil | 62.44 | 0.5 | 0.87% |

US MARKET

Equities climbed toward the highest since February, the month that marked the S&P 500’s all-time high. Up about 1%, with chipmakers leading the charge as Nvidia Corp. and Advanced Micro Devices Inc. will supply semiconductors to Saudi Arabian firm Humain for a massive data-center project. The S&P 500 rose 1%. The Nasdaq 100 climbed 1.8%. The Dow Jones Industrial Average lost 0.3%. A closely watched gauge of chipmakers rallied 3.1%. The Magnificent Seven index of megacaps added 2.4%.

The Trump administration plans to overhaul regulations on the export of semiconductors used in artificial intelligence, tossing out a Biden-era approach that had drawn strenuous objections from America’s allies.

After mostly missing out on last month’s rebound, investors are likely to be forced to chase the stock rally sparked by this weekend’s US-China trade truce. A survey conducted before the trade talks in Geneva showed fund managers were a net 38% underweight on US stocks, the most in two years. The poll is bearish enough to suggest the pain trade is modestly higher given the US-China deal would prevent a recession or a shock in credit markets.

The negative earnings-growth momentum that plagued US equities for months is finally taking a turn for the better. A gauge of earnings revisions, based on the number of upgrades and downgrades, has turned positive for the first time in six months. And, 77% of S&P 500 members that reported surprised positively in the first quarter, the highest since the second quarter of last year. Meanwhile, earnings growth in the quarter is running at 13.1%, compared with just 6.6% expected before the start of the season. Last month, sell-side strategists were downgrading their forecasts for the S&P 500 at a furious pace. But since then, well, . . . ., forcing those same strategists to pull U-turns on their calls.

Wall Street veterans Ed Yardeni and David Kostin at Goldman Sachs are among the strategists changing course this week, calling for the S&P 500 to rally past 6,000 by December’s close. They also were among the first to slash their 2025 targets for the benchmark in April.

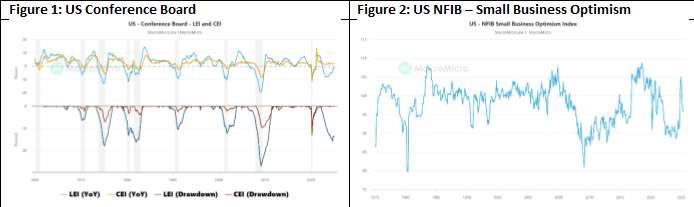

Well, Wall Street isn’t Main Street, right. Sentiment among US small businesses deteriorated for a fourth straight month in April due to concerns about the economic outlook and sales prospects amid higher tariffs. The National Federation of Independent Business (NFIB) optimism index dropped 1.6 points to 95.8, the weakest reading since October, with six of the survey’s 10 components decreasing (see figure 2).

Figure 1 displays the leading and coincident indicators published by the Conference Board (CB), both of which are key tools for assessing economic health. The Leading Economic Index (LEI) is derived from data such as average working hours, the number of initial unemployment benefit claims, new manufacturing orders, and the stock price index. It typically signals future economic trends. The Coincident Economic Index (CEI), in contrast, reflects the current state of the economy, based on data like employment, personal income excluding transfer payments, manufacturing and trade sales, and industrial production. The year-on-year growth rate is calculated by comparing the most recent value with the value from the same period last year. The drawdown is calculated by measuring the decline from the three-year

high to the most recent value. Historical data indicates that when both leading and coincident indicators show a significant decline, it often signals that the economy is either already in or on the verge of a recession.