| Name | Daily Close | Daily Change | Daily Change (%) |

|---|---|---|---|

| Dow | 40,524.79 | 312.08 | 0.78% |

| S&P 500 | 5,405.97 | 42.61 | 0.79% |

| Nasdaq | 16,831.48 | 107.03 | 0.64% |

| VIX | 30.89 | -6.67 | -17.76% |

| Gold | 3,228.80 | 2.5 | 0.08% |

| Oil | 61.59 | 0.06 | 0.10% |

US MARKET

Wall Street traders were hit by volatility again as most big techs fell, with the latest chapter of President Donald Trump’s trade war spurring fresh confusion for business leaders grappling with policy uncertainty while stoking inflation angst among consumers. As the equity market’s most-influential group erased gains, the S&P 500 trimmed a rally that had earlier been driven by White House’s softer tariff stance toward the technology sector. Carmakers, such as General Motors and Ford, climbed as Trump floated exceptions for auto parts facing 25% US tariffs.

At the close, the S&P 500 Index was up 0.8%, the Nasdaq 100 up 0.6%, and the Dow Jones Industrial Average up 0.8%. Consumer discretionary was the only sector that was in the red. Apple was up 2.2%, after being up as much as 7% intra-day. The VIX declined to the low 30s. However, bucking the day’s trend, the USD continued to slide for a 5th consecutive day.

Wall Street strategists expect the S&P 500 Index to rally through the remainder of 2025, despite the uncertainty and convulsions caused by President Donald Trump’s trade policies. Most strategists have adjusted their predictions for the S&P 500’s performance this year, with some cutting their targets, but the vast majority still expect equities to rise.

The trade chaos has stock market forecasters across Wall Street adjusting their predictions for where the S&P 500 will end 2025. Subramanian cut hers to 5,600 from 6,666, and colleagues at Oppenheimer & Co., Evercore ISI, Goldman Sachs Group Inc., Societe Generale SA and RBC Capital Markets have trimmed theirs as well. Ed Clissold at Ned Davis Research lowered his target to 5,550 from 6,600, reflecting a 50% chance of recession. But the vast majority still expect equities to rise from here. Only Berezin at 4,450 and JPMorgan Chase & Co.’s Dubravko Lakos-Bujas at 5,200 see the index finishing 2025 below where it closed Friday, 5,364.

That said, there’s little unity among the predictions. From Berezin’s target to Wells Fargo & Co.’s Chris Harvey at 7,007, the gap is more than 2,500 points, or 57%, which is the widest on record for this point in the year. The average of 6,067 represents a roughly 13% leap from Friday’s close. The biggest challenge for strategists trying to model where stocks are headed is Trump’s trade strategy seems to change by the day. Scott Chronert, Citigroup Inc.’s US equity strategist and managing director probably stated it at its simple best: “Holy moly! We weren’t prepared for this. People have been asking since last summer how to position on Trump’s tariff policy, but are you kidding me? I don’t know how to do that modelling.”

Fears of a slowing economy are at the heart of the uncertainty. Just six weeks ago, economists were expecting the US to post 2.3% growth in gross domestic product, but they’ve cut that 1.8% as Trump’s tariffs take hold. Which makes the generally bullish stance of most stock market strategists harder to justify.

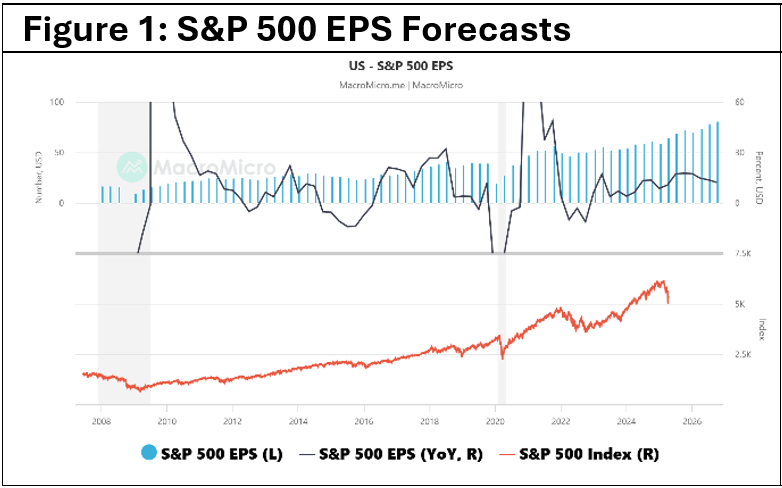

Regarding Figure 1, the EPS estimates for the coming year are based on S&P Global’s quarterly announced earnings forecasts, which draw from the quarterly earnings S&P 500 constituent companies reported.

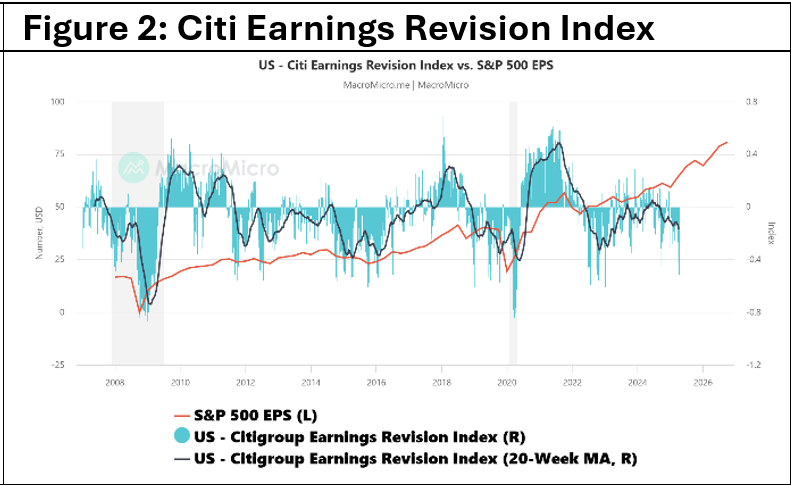

Regarding Figure 2, the Citigroup Earnings Revision Index is calculated as the proportion of listed companies that have received upward EPS revisions minus the proportion of those with downward EPS revisions. When the index reading is above zero, it means that analysts on average are optimistic about the outlook for corporate earnings, which means a higher possibility for the S&P 500 to post strong performance. A decline below zero in the index usually precedes an EPS revision by about 1~2 quarters. The index is thus considered a leading indicator for corporate earnings adjustments.

Meanwhile, China’s latest move to counter Donald Trump’s chaotic trade war is to increase restrictions on the supply of key rare earths and high-performance rare earth magnets crucial to US manufacturing, electronics and defence industries. The suspension of shipments from Chinese ports subject to the start of a new licensing regime is officially in reaction to the escalation of US tariffs on Chinese exports this month.

Finally, Citi and BoA report earnings tomorrow. This comes after JPMorgan on Friday and Goldman’s today. To date, there has not been significant guidance. And why would there be. On Friday morning before the JPMorgan earnings call, Jamie Dimon had to call his chief economist just to check what the house recession call was, such is the flux we are in. But it is really going to the smaller to mid cap companies that are really going to struggle with guidance.

AUSTRALIAN EQUITY MARKET WRAP

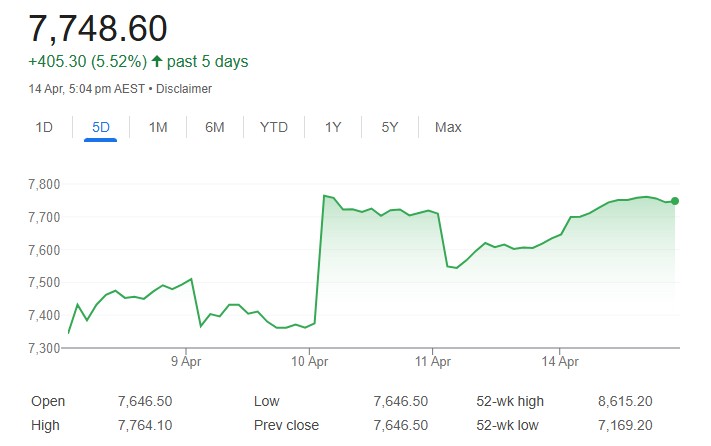

The S&P/ASX 200 Index climbed 1.34% to close at 7,749 on Monday, recovering from the previous session’s losses as stronger commodity prices boosted mining and energy stocks. Australian equities also mirrored gains in global markets after US President Donald Trump announced exemptions for consumer electronics from newly imposed “reciprocal” tariffs, lifting overall risk appetite.

Ten of 11 sectors were higher, led by materials and technology. A cautious rise in ASX 200 technology stocks had gathered steam by lunchtime with the sector 2.2% t higher, buoyed by WiseTech and TechnologyOne, up 2.8% and 2.7% respectively. Mining and energy stocks also led the charge, with notable gains from BHP Group (+2.6%), Fortescue Metals (+1.1%), Northern Star Resources (+1.2%), Woodside Energy (+1%), and Santos (+2.1%). Other key sectors also contributed to the advance, including financials, and healthcare. However, ongoing trade tensions between the US and China continued to cast a shadow, given Australia’s economic exposure to Chinese demand and export markets.

The All Ordinaries also rose by 1%. Ten of 11 sectors were higher, led by materials and technology. A cautious rise in ASX 200 technology stocks had gathered steam by lunchtime with the sector 2.2% t higher, buoyed by WiseTech and TechnologyOne, up 2.8% and 2.7% respectively. Miners tracked an early rally in the iron ore price, buoyed by hopes for a China-US trade deal. Index bellwether BHP jumped 2.5% and Mineral Resources 7.4%. Gold miners continued Friday’s rally after the price for the precious metal set a record late last week, with Newmont jumping more than 4.8%.

Semblance restored? Well, let’s not get ahead of ourselves. Monday was always going to be an up day given it was comforting words from a Fed official on Friday that led to an up day, and an up day that by the very degree of the up was comforting. Friday was in complete contrast to what happened on Wednesday last week, which was nothing short of a fool’s paradise. And then over the weekend, we heard that the likes of Apple and Nvidia were getting an exemption. Classic. Tariffs are just a regressive tax for the poor.

Notwithstanding Friday’s developments, where the Fed stated it will step in if required in relation to what was a creaking bond market, the equities market have two massive issues: 1) China isn’t going to play ball and both leaders have immense pride; 2) yes, the Fed may have reassured markets, but the US Government bond market is nuts currently. Just because the Fed said they may intervene, that doesn’t mean they won’t tolerate a high degree of yield widening before they do. US treasuries have gone from risk-free to not risk-free.

Foreign investors own 33% of US Treasuries, 27% of US corporate bonds and 18% of US stocks. And they are turning away – the USD moves last week were probably the give away. And it’s why volatility indices across bonds and stocks have not retreated. And it’s why the benchmark 10-year US Treasury yield remains stuck near 4.5%, up from 3.99% just 10 days ago. As they say, ‘Houston, we have a problem’.

As we noted in our Weekly note, believe the hype on selling the US. Despite President Trump’s pause on broad tariffs, investors are still looking to shun US assets in favour of Europe and other developed markets, according to the latest MLIV Pulse survey. Of the 203 respondents to a poll conducted April 9-11, after Trump announced a 90-day reprieve on levies for most countries, 81% plan to either keep their exposure to US assets the same or decrease it. More than a quarter of respondents said they’re curbing their investment more than they had anticipated before the president unveiled global tariffs of as much as 50% earlier this month. As per our last Thursday daily headline, from US exceptionalism to sell everything US. What’s the reflex trade – the Deutsche Bund, Swiss Franc, Japanese Yen, and gold.

China is not about to back down. This is their moment. We have a huge problem. One country issuing the death rattles of a country, maybe not an economy, but a country by all other measures is on the slide. China will push. And they know they are in a position of strength. The good news – this could benefit Australia, at least in first order effects (cheaper imports, if we ignore the AUD move impacts).

Why do we mention all this in relation to the ASX. Well, anyone that thought the Australian market would skirt the turmoil probably hasn’t lived through the GFC and March 2020 or, at the very least, were engaging in wishful thinking. We love a positive attitude, unless you are managing my money. In a financial markets crisis, cross equities markets correlation go to circa one, with the US being the lead. Now, the Australian market has a lower market beta than the Tech sector led US market (the US, along with the Netherlands, being the highest in the world), which means the move aren’t to the same degree. But a loss is a loss and, by definition, it means the up swings are likely to be less.

Think about that market beta concept and the US market, with the S&P 500 having a market beta of circa 2.0. We all know about market concentration regarding the Mag 7, etc. But was anyone thinking about the high beta risk concentration?? Google market betas by index – good luck. And now start to think about that high beta in the context of portfolio allocation. Ok, maybe I get +4% yoy out of the S&P 500 over the ASX 200. But I damn side need it, because the risk is higher, without even throwing currency into the mix.