| Name | Daily Close | Daily Change | Daily Change (%) |

|---|---|---|---|

| Dow | 42518.28 | 221.16 | 0.52% |

| S&P 500 | 5842.91 | 6.69 | 0.11% |

| Nasdaq | 19044.39 | -43.71 | -0.23% |

| VIX | 18.71 | -0.48 | -2.50% |

| Gold | 2693.1 | 14.5 | 0.54% |

| Oil | 78.09 | -0.73 | -0.93% |

US MARKET

The U.S. markets experienced a mixed day, with the S&P 500 inching up 0.1% to close above its 100-day moving average after briefly dipping below it. The Nasdaq 100 fell by 0.1%, weighed down by pressure on big tech stocks, while the Dow Jones Industrial Average gained 0.5%. Small-cap stocks outperformed, with the Russell 2000 rising 1.1%.

Investors are closely watching the Consumer Price Index (CPI) report set for Wednesday, which is expected to be pivotal for inflation expectations and market sentiment. Options traders anticipate a potential 1% move in either direction based on the report. Economists predict core CPI for December will increase by 0.2% month-over-month and 3.3% year-over-year, in line with recent trends. A strong reading could reinforce expectations that the Federal Reserve will hold off on rate cuts in 2025 or possibly implement another hike, while a weaker reading might alleviate market concerns about the Fed’s policy stance.

Recent Producer Price Index (PPI) data showed an unexpected cooling in December due to lower food costs and flat services prices. However, components feeding into the Fed’s preferred Personal Consumption Expenditures (PCE) inflation gauge were mixed, leaving markets vulnerable to volatility around the CPI release.

Corporate earnings are also in focus, with major banks like JPMorgan, Wells Fargo, and Goldman Sachs kicking off the season. Analysts expect gains in trading and investment banking to offset challenges from higher deposits and sluggish loan demand. Results will be closely scrutinized for insights into net interest income and broader economic trends.

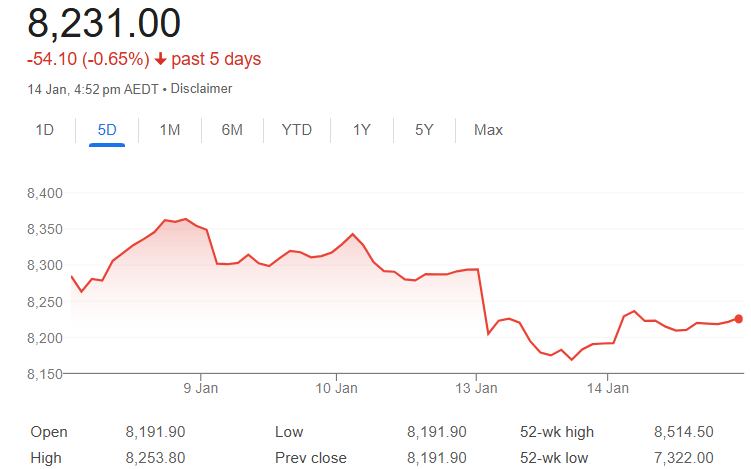

Australian shares are expected to open slightly higher, with ASX futures rising 5 points (0.1%) on Wednesday, reversing earlier losses. This modest improvement aligns with Wall Street’s cautious gains, where the S&P 500 closed up 0.1% as investors await key US inflation data. Iron ore prices rose 1.9% overnight to $US100.88 per tonne, extending Tuesday’s rally, which could provide support for Australian mining stocks. However, Brent crude fell 1.2% to $US80.06 per barrel, potentially weighing on the energy sector. Broader sentiment is influenced by expectations of continued disinflation in the US, with weaker-than-expected producer price data adding to optimism, potentially creating a supportive environment for Australian markets.