| Name | Daily Close | Daily Change | Daily Change (%) |

|---|---|---|---|

| Dow | 39,669.39 | -699.57 | -1.73% |

| S&P 500 | 5,275.70 | -120.93 | -2.24% |

| Nasdaq | 16,307.16 | -516.01 | -3.07% |

| VIX | 32.64 | 2.52 | 8.37% |

| Gold | 3,365.90 | 19.5 | 0.58% |

| Oil | 62.94 | 0.47 | 0.75% |

US MARKET

The calm has been broken. It was a Jerome Powell speech at the Economic Club of Chicago that triggered the main moves of the day. The key comment from Jerome Powell, and it was exactly when the market started to sell off, was when the Fed said it may have a problem with it’s dual mandate this year. Specifically, he stated that the economy will likely be “moving away” from both of its goals “probably for the balance of this year.” That is, higher inflation and higher unemployment (a stagflation scenario, and was written all over the conversation) and which would put the Fed between a rock and a hard place. He also stated that there is uncertainty about tariffs would lead to a one-off price impact or that the price impact would be more persistent. And finally, he reiterated that, with the current employment and inflation levels, the Fed is in no rush to move on rates. So, forget any Fed put, at least in the short term.

The sell-off accelerated in the last 2 hours (up to the last 10 minutes) and coinciding with the start of the Powell conversation and it was relatively broad based. By close, the S&P 500 Index was down 2.2%, the Nasdaq 100 down 3.0%, the Dow Jones Industrial Average down 1.6%, and the Russell 2000 Index down 1.0%. The tech sector led the sell-off. Nvidia got smashed, down 10%, and the semiconductor index down 6% after Nvidia and AMD stated Trump’s administration had curbed the export of their chips. Here’s the lesson from this sell-off if people didn’t already know it – go low beta stocks and markets if seeking relative shelter. And the US is the highest beta market globally.

But the range of outcomes is narrowing slightly, and as evident by the VIX back in the low 30s. Treasuries continue to rally, with 10-year yields now down 5 basis points on the day. That’s while the USD Index is down 0.6% on the day. In other words, we’re not seeing the stocks down/dollar down/Treasuries down pattern that sparked concerns last week. Treasuries are acting as you would normally expect when stocks are having a bad day: They’re up. The flight-to-safety bids had been missing last week when some fast-money traders were deleveraging. From that perspective, it’s a good sign — the market is functioning.

On the macro front, US retail sales rose substantially in March on a jump in car purchases and other goods such as electronics, suggesting consumers were scrambling to get ahead of tariffs. The value of retail purchases, not adjusted for inflation, increased 1.4%, the most in over two years. Excluding autos, sales climbed 0.5%. So, US consumers are bringing forward purchases. But that will lead to a subsequent ‘vacuum’.

Several surveys of consumer sentiment have plunged as Trump presses forward with tariffs, which are also causing some measures of inflation expectations to soar and tanking Americans’ perception of their financial situations. With low-income consumers already facing hardships and wealthier ones being hit by a recent stock-market selloff, that’s clouding the outlook for spending and adding to recessions fears. It’s a case of when the soft data becomes the hard data.

On the M&A front, while the US is down, Europe and Asia-Pacific are actually doing quite well. And a lot of the transactions are cross border. Another flight from US theme. PE hold periods are already well above a circa 6-year hold period, so LPs aren’t getting their money back.

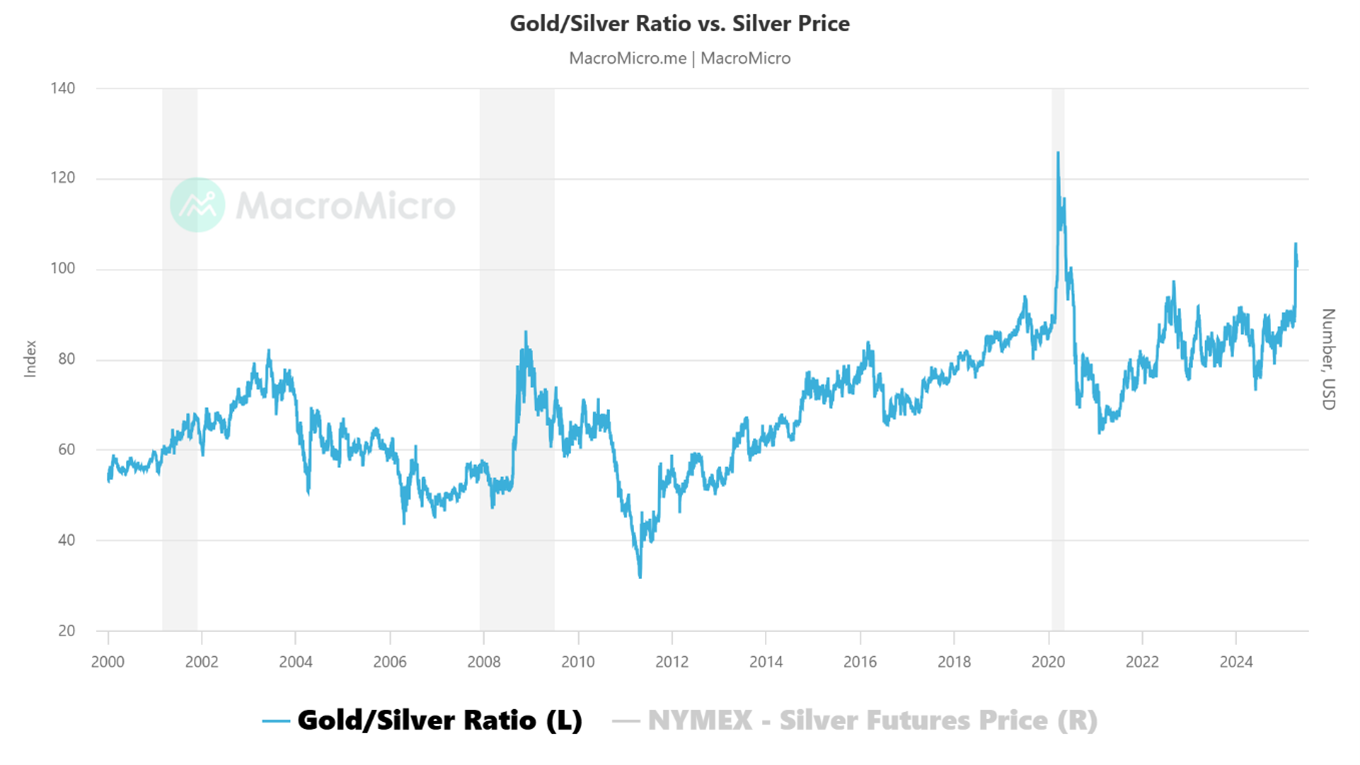

Finally, the gold-to-silver ratio quantifies the ounces of silver required to purchase one ounce of gold. At approximately 100:1 as of April 2024, this metric has only breached triple digits three times in the past century: in 1991, March 2020, and April 2024. Historically, the ratio averaged 15:1 during ancient monetary systems and 50:1 over the last 50 years, but modern market forces—including central bank policies and industrial demand—have reshaped its relevance. The ratio’s extremes often signal macroeconomic stress or shifts in investor sentiment. In 1980, after the Hunt brothers’ attempt to corner the silver market, the ratio narrowed to 16:1 as silver peaked near $50/oz. By 1991, an 11-year bear market in silver pushed the ratio to 100:1, marking a generational buying opportunity ahead of a 60% price surge over the next two years. Similarly, the COVID-19 pandemic-driven ratio of 126:1 in March 2020 preceded a 140% silver rally within months.

|

Figure 1: Gold to Silver Ratio is Sending an Ominous Warning Unless You are Long Gold |

|

LOCAL MARKET

The Australian sharemarket held its modest advance after the White House said it was open to a trade deal with China, although fears about the global economic outlook persist as China shows not only no signs of playing ball but has imposed its own counter-measures (as per rare earths). The S&P/ASX 200 Index was up 0.3%, or 20.4 points to 7782. Six of 11 sectors were in the green, led by financials.

The news did little to settle investor caution. US futures pointed lower after Wall Street drifted on a rare quiet day in financial markets. A slew of banks cast a gloomy outlook for the economy: Bank of America’s survey showed investor sentiment had hit a three-decade low, with many reducing US equities exposure as a result.

On the ASX 200, the banks – boosted by positive reporting in the US – tussled with losses from energy and mining names. Westpac advanced 1.8% and Commonwealth Bank 1%. Utilities, communications and consumer staples – typically considered defensive stocks in times of market stress – rose.

Elsewhere, gold miners rallied after spot prices neared $US3200. Genesis Minerals posted the biggest gain on the ASX 200, up 9.1%. Oil and gas explorers Woodside and Santos drove energy stocks lower, dropping 2.6% and 2.3%, respectively. That was after Brent crude extended a decline after the International Energy Agency slashed its oil demand forecast.

Having a bad month in the markets?? Well, some of the courntry’s best known fund managers have been cruxified. Regal is notable. Their Atlantic Absolute Return fund is down 35% in March alone. If they don’t turn April around . . . . and good luck with that. The head stock is down 50% 2025 ytd. Listed equities managers – fancy triple beta?? Anyways, Regal won’t be bidding on any more listed fund managers anytime soon.

On the topic of LICs, the WAM Income Maximiser initial public offering from Wilson Asset Management. The AFR reports that Wilson Asset Management brought in roughly $150 million for its new ASX-listed vehicle – a valiant effort considering the bookbuild collided with a 14% decline in the S&P/ASX 200 from peak to trough and Trump’s trade chaos, but a far cry from the $510 million target sought in the prospectus. If Geoff Wilson can’t get a successful IPO off, probably no one can.

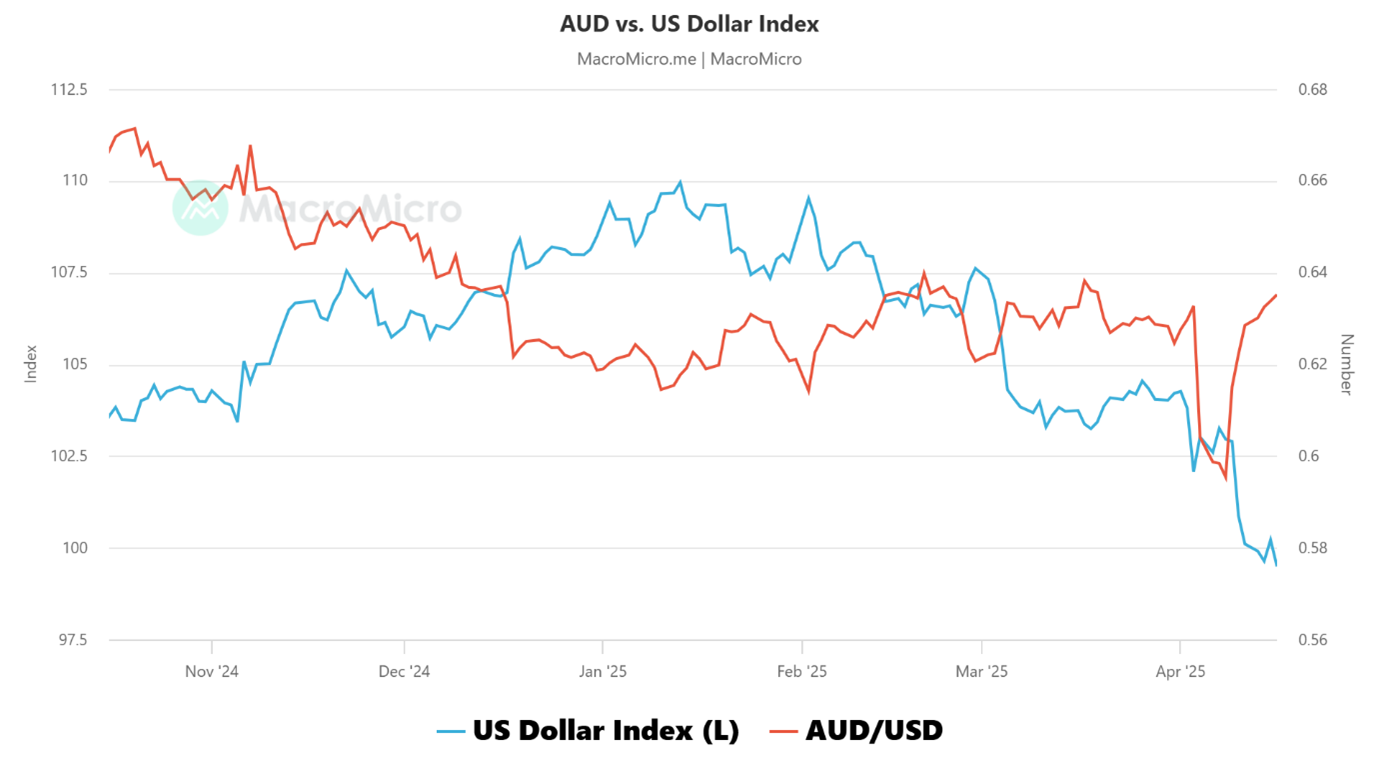

Finally, is there buying in the AUD or just selling in the USD. Whatever the case, the AUD is back at levels pre ‘Liberation Day’.

|

Figure 2: AUD vs USD Index |

|