| Name | Price | Change | % Chg |

|---|---|---|---|

| Dow | 45,757.90 | -125.55 | -0.27% |

| S&P 500 | 6,606.76 | -8.52 | -0.13% |

| Nasdaq | 22,333.96 | -14.79 | -0.07% |

| VIX | 16.36 | 0.67 | 4.27% |

| Gold | 3,731.80 | 6.7 | 0.18% |

| Oil | 64.59 | 0.07 | 0.11% |

OVERVIEW OF THE US MARKET

Wall Street traders paused a record-breaking rally on September 16, 2025, as solid retail sales data tempered expectations for aggressive Federal Reserve rate cuts. The S&P 500 slipped 0.13% to 6,606.76, the Nasdaq Composite fell 0.07% to 22,333.96, and the Dow Jones Industrial Average dropped 0.27% to 45,757.90. Energy led sectors with a 1.73% gain amid supply disruption fears, while utilities lagged at -1.81%. Actives included Opendoor Technologies down 6.06% on high volume, BigBear.ai up 16.70%, and Snap rising 3.75%.

Retail sales rose 0.6% in August, beating estimates of 0.2% and signaling resilient consumer spending despite labor market concerns. Industrial production edged up 0.1%, against forecasts of a 0.1% decline. The data fueled debate over the Fed’s impending move, with markets pricing in a 25 basis-point cut on September 17, though some speculate on 50 basis points to support jobs. President Trump filed a $15 billion defamation suit against The New York Times, and TikTok’s US operations neared acquisition by a consortium including Oracle.

Treasury Secretary Scott Bessent expressed disappointment in trade talks over China’s Nvidia antitrust ruling, while adding the US and China may extend tariff discussions. Strategists at Morgan Stanley noted consumer strength as positive for growth but potentially limiting Fed easing. Bank of America surveys showed fund managers overweight equities at a net 28%, with improved growth optimism. Citadel Securities warned of near-term turbulence from valuations and seasonal volatility, but sees AI spending lifting stocks into year-end.

OVERVIEW OF THE AUSTRALIAN MARKET

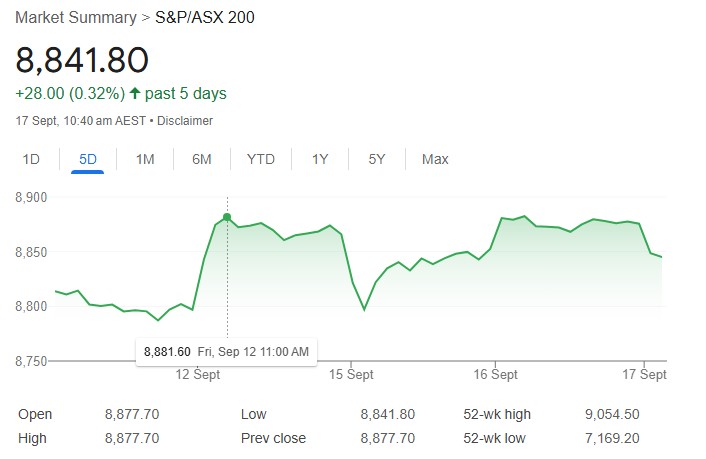

Australian shares ended higher on September 16, 2025, buoyed by gains in energy and resources sectors amid positive developments in uranium and iron ore markets. The S&P/ASX 200 rose 0.28% to 8,877.7, while the broader All Ordinaries climbed 0.33% to 9,151.2. Energy led the sectors with a 0.94% increase, driven by uranium stocks surging on news of a US-UK agreement to accelerate nuclear power approvals and plans to boost US uranium stockpiles. Bannerman Energy jumped 11.6%, Deep Yellow 9.2%, and Nexgen Energy 8.7%. Resources also advanced 0.8%, with iron ore majors BHP up 0.5%, Rio Tinto 1.9%, and Fortescue 1.1% supporting the move.

Small caps showed strength, particularly in mining, with advancers outpacing decliners 184 to 88 in the ASX 300. Top gainers included Sunrise Energy Metals up 29.9% on a US EXIM letter of interest, Avita Medical 28.5% following CE Mark approval, and Race Oncology 27.8% on a breakthrough IP discovery. On the downside, Falcon Metals fell 18.2% after mixed drill results, and LTR Pharma dropped 13.0%. Health care lagged with a 0.33% decline, weighed by CSL slipping 1.3% on a $760 million investment in Dutch biotech VarmX.

The market’s modest gains came ahead of key data releases, including August employment figures due Thursday, where economists expect 21,000 jobs added and unemployment steady at 4.2%. Traders are also eyeing the Federal Reserve’s rate decision overnight, which could influence global sentiment. The AUD/USD edged down 0.07% to 0.6665, reflecting caution amid US data strength.