| Name | Price | Change | % Chg |

|---|---|---|---|

| Dow | 44,484.49 | 229.71 | 0.52% |

| S&P 500 | 6,297.36 | 33.66 | 0.54% |

| Nasdaq | 20,885.65 | 155.16 | 0.75% |

| VIX | 16.52 | -0.64 | -3.73% |

| Gold | 3,345.60 | 0.30 | 0.01% |

| Oil | 67.55 | 0.01 | 0.01% |

OVERVIEW OF THE US MARKET

US stocks advanced on Thursday, July 17, 2025, as investors welcomed a strong Philly Fed Business Index and robust retail sales data, overshadowing Trump’s persistent 30% tariff threats on EU and Mexico goods due August 1. Treasury yields rose slightly, and the dollar held firm, with markets eyeing tomorrow’s housing starts data.

The S&P 500 climbed 0.54% to 6,297.36, and the Nasdaq Composite gained 0.75% to 20,885.65, driven by broad sector strength. Financials surged 0.92%, with Information Technology up 0.89%, led by Nvidia’s 0.95% rise to $173.00 on 160.7 million shares. Lucid Group (LCID) soared 36.24% to $3.12 on 940.0 million shares, likely boosted by EV sector news. Health Care lagged, down 1.18%, amid tariff concerns on pharmaceuticals.

Yesterday’s data showed retail sales up 0.6% month-over-month against a 0.1% forecast, and the Philly Fed Index jumped to 15.9 from -4, signaling industrial recovery. Initial jobless claims fell to 221,000 from 227,000, easing labor market fears. With import prices dropping 0.2% year-over-year, inflation pressures eased, reinforcing expectations for a September rate cut, with two cuts priced by year-end.

OVERVIEW OF THE AUSTRALIAN MARKET

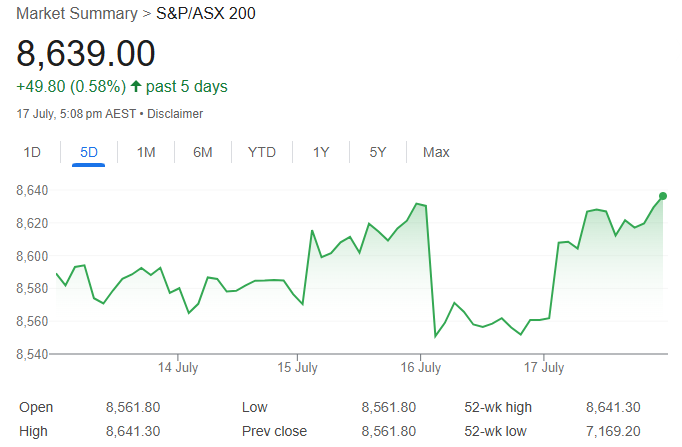

The ASX 200 hit its 10th record high of 2025, rallying 0.90% to 8,639.0 on Thursday, July 17, 2025, as weak employment data spurred rate cut hopes, despite a 0.64% drop in the Australian dollar to 0.6487. The market’s resilience shone through, supported by Prime Minister Anthony Albanese’s China visit, which bolstered trade optimism amid global tariff tensions.

Industrials (+1.43%) and Financials (+1.33%) led gains, with the Big Four banks rebounding—CBA up 1.8% to $180.80, Westpac 1.2%, and ANZ and NAB both 1.1%. Real Estate rose 1.31%, with Mirvac jumping 3.2% to $2.24 on rate-sensitive optimism. Materials edged up 0.18%, though Newmont fell 5.7% post-CFO resignation. Tech gained 1.02%, reflecting broad strength.

Yesterday’s employment data, showing only 2,000 jobs added versus 20,000 expected and unemployment rising to 4.3% from 4.1%, triggered a 0.2% late rally and lifted August rate cut odds to 94%. Albanese’s China talks offer trade stability, but the AUD’s decline reflects tariff and data concerns.