| Name | Daily Close | Daily Change | Daily Change (%) |

|---|---|---|---|

| Dow | 44,627.59 | 71.25 | 0.16% |

| S&P 500 | 6,144.15 | 14.57 | 0.24% |

| Nasdaq | 20,056.25 | 14.99 | 0.07% |

| VIX | 15.27 | -0.08 | -0.52% |

| Gold | 2,949.60 | 0.6 | 0.02% |

| Oil | 72.18 | 0.33 | 0.46% |

US MARKET

The S&P 500 remained little changed in afternoon trading, hovering near record highs, while the Dow Jones and Nasdaq each declined more than 0.3%. Investors assessed the possibility of an end to the Ukraine war following the first top-level negotiations between the US and Russia since the 2022 invasion.

Weakness in consumer discretionary and communication services, including a 3.7% drop in Meta Platforms and a 2% decline in Amazon, pressured the broader market. In contrast, energy stocks outperformed, with Exxon Mobil rising 2.2% and Energy Transfer gaining 1.3%. Meanwhile, market participants closely monitored policy developments from the Fed and the White House, particularly regarding tariffs and interest rates.

Treasury yields climbed, with the benchmark 10-year yield reaching 4.54%, as traders sought clarity on the Fed’s rate trajectory. Earnings season also remained in focus, with upcoming reports from Baidu and Alibaba adding to uncertainty over the global economic outlook. The Bloomberg Dollar Spot Index rose 0.2%.

The S&P 500 has gone mostly nowhere this year. Global stocks have become the most-popular asset class with investors, who are showing the biggest willingness to take risk in 15 years, according to a survey by Bank of America Corp. Fund managers’ cash levels fell to the lowest since 2010, while 34% of participants said they expect world equities to be the best-performing asset in 2025, the survey showed. A net 11% indicated they were underweight bonds. Effectively, investors are long stocks, short everything else. But there is a bigger theme here in relation to equities – a diversification trade. And that is not just geography, but sector as well. But it is not – yet – moving into small caps.

Bank of America issued a note showing that while 4Q earnings definitively beat EPS estimates, earnings guidance has generally been weak. You could read this in several ways. Of course, it could reflect a fundamental outlook but, in our view, there is more than a degree of an uncertainty risk premium here – new administration, Trump uncertainty, Tariff uncertainty.

Australian Market Wrap

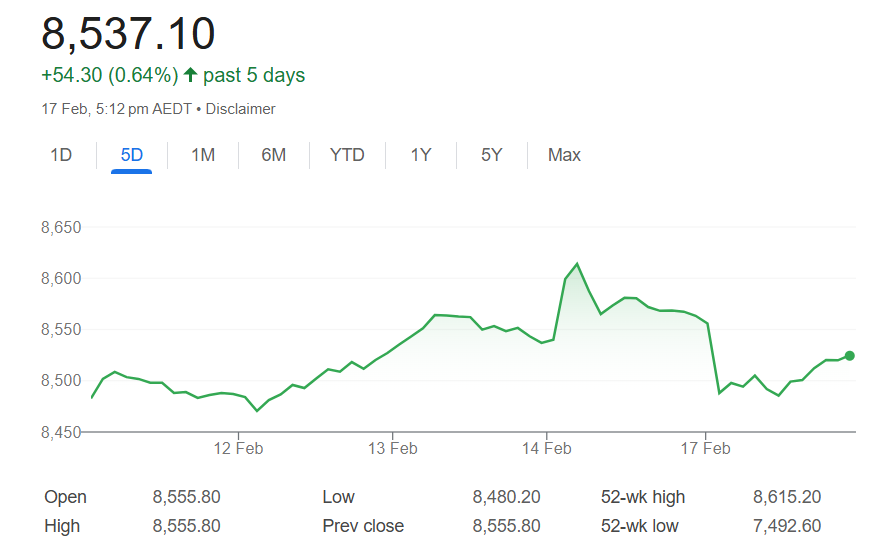

The S&P/ASX 200 Index dropped 0.66% to close at 8,481 on Tuesday, sliding for the second straight session after the RBA lowered its cash rate by 25 basis points to 4.1%, as widely expected. However, the central bank signalled a more cautious approach to further policy easing in case the disinflation process stalls. Hard to think of a more hawkish cut. To emphasis the point, the 10-year and, more importantly, the policy sensitive 2-year yield all rose, and materially. On February 5 the expectation of a cut to 3.85% was 39%. Now its 21%. Longer term, markets are pricing a shallow easing cycle, forecasting a cash rate of 3.6% by September or two more quarter point rate cuts.

In corporate news, BHP Group saw increased volatility after the iron ore miner slashed its dividend following a decline in profits. Financial stocks led the market downturn, with losses from Commonwealth Bank (-1.4%), Westpac Banking (-3%), NAB (-2.5%), and ANZ Group (-1.8%). There has been a distinct cooling of analyst sentiment towards the banking sector. Energy and lithium stocks also suffered, including Woodside Energy (-1.5%) and Pilbara Minerals (-5.4%).

ASX futures are pointing up 4 points or 0.1% to 8437. NAB is set to provide a first quarter trading update this morning, with results pending from, among others, Santos, Goodman Group, James Hardie, Cleanaway, Iluka Resources and Stockland.