| Name | Daily Close | Daily Change | Daily Change (%) |

|---|---|---|---|

| Dow | 44,922.27 | 10.45 | 0.02% |

| S&P 500 | 6,411.37 | -37.78 | -0.59% |

| Nasdaq | 21,314.95 | -314.82 | -1.46% |

| VIX | 15.57 | 0.58 | 3.87% |

| Gold | 3,356.90 | -1.8 | -0.05% |

| Oil | 62.64 | 0.29 | 0.47% |

OVERVIEW OF THE US MARKET

Wall Street closed mixed on August 19, 2025, as a surge in housing starts bolstered sentiment but tech selloffs amid valuation concerns weighed, with the Nasdaq snapping a streak amid broader market caution. The S&P 500 fell 0.59% to 6,411.37, the Nasdaq Composite dropped 1.46% to 21,314.95, and the Dow Jones Industrial Average rose 0.02%, or 10.45 points, to 44,922.27. Consumer staples led with a 1.00% gain, followed by real estate (+1.80%) and health care (+0.62%), while information technology lagged at -1.88%, communication services -1.15%, and industrials +0.19%.

Large-cap stocks declined, mid-caps flat, small-caps edged up. Growth fell 1.20%, blend -0.59%, value +0.02%. Actives included Opendoor Technologies (-4.23% to $3.62), Intel (+6.97% to $25.31), NVIDIA (-3.50% to $175.64), Palantir Technologies (-9.35% to $157.75), and Laser Photonics (+59.35% to $3.92).

July housing starts surprised at 1.428 million (above 1.29 million poll), signaling construction strength despite rates, countering industrial weakness. Investors watch tomorrow’s Philly Fed Index (poll 7) and S&P Global PMIs for manufacturing/services. FCC Chair Brendan Carr’s push to abolish TV ownership caps—potentially enabling Nexstar’s $6.2 billion Tegna acquisition—sparks debate, with opponents claiming Congress must decide, amid Trump’s media deregulation favoring broadcasters vs. Big Tech.

Treasury Secretary Scott Bessent highlighted ongoing tariff truce talks with China, noting a 90-day extension option under Trump, though muted reactions underscore deal fatigue. A Journal of Financial Economics study notes P/E spreads 75% driven by expected returns over growth, emphasizing discount rates/mispricing—timely as high multiples prompt diversification.

With Fed at 4.25%-4.5%, autumn cut signals sought as Powell faces labor dissent. HSBC, Morgan Stanley, UBS strategists bullish on earnings, tariffs, AI. Goldman’s chief warns tariffs erode prices despite pacts, urging diversification amid recession dodge and valuations.

OVERVIEW OF THE AUSTRALIAN MARKET

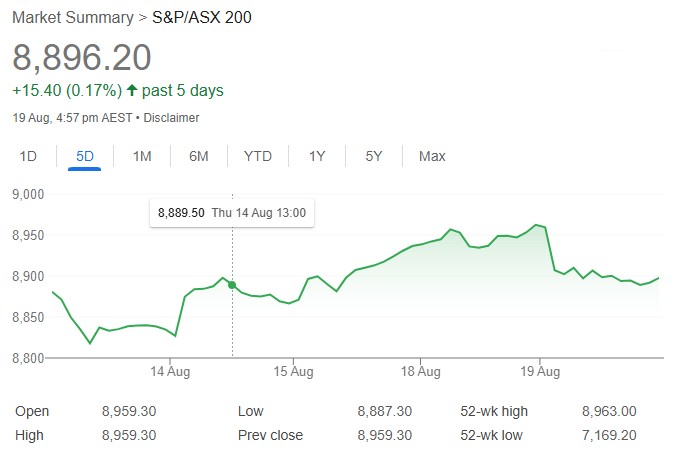

Australia’s share market slipped from records on August 19, 2025, as CSL’s sharp post-earnings plunge dragged health care amid broader earnings scrutiny, though financials and tech provided offsets in a mixed session. The S&P/ASX 200 fell 0.70%, or 63.1 points, to 8,896.2—the steepest drop since August 1—while All Ordinaries declined 0.65% to 9,173.8. Decliners edged advancers 139 to 129 on S&P/ASX 300.

Seven sectors rose, led by communication services (+0.72%), information technology (+0.57%), and financials (+0.37%). Health care crashed -8.73%, energy -2.20%, industrials -0.84%. Health: CSL (-16.9% to $227.79) on job cuts/vaccine spin-off despite solid results. Energy: Woodside (-2.8%) profit drop, Santos/Whitehaven lower. Financials: NAB (+2.7% to $40.23) on update, CBA (+1.2% to $170.19) rebound, though ANZ -1.5%. Communication: Seek (+8.0%) revenue boost. Materials +0.34%: BHP (+1.6%) on $US9 billion profit.

Gainers: Dateline Resources (+12.5%) on breccia targets, Centuria Capital (+10.0%) FY25 results, Macmahon (+9.7%). Losers: Strike Energy (-12.5%) on impairment, Minerals 260 (-7.7%), Falcon Metals (-7.7%) pullback.

July data (wages 3.4% yearly slight beat, employment +24.5k) aligns RBA easing post-3.60% cut. Aussie flat at 64.92 US cents. Ord Minnett’s David Lane notes volatility from earnings reactions, high bar for records with BHP, CSL tomorrow.

AMP’s Oliver easing bullish sans recession, volatility from valuations/Trump wars. Journal study: P/E 75% returns-driven, urging discount focus as ASX corrects.