| Name | Price | Change | % Chg |

|---|---|---|---|

| Dow | 45,295.81 | -249.07 | -0.55% |

| S&P 500 | 6,415.54 | -44.72 | -0.69% |

| Nasdaq | 21,279.63 | -175.92 | -0.82% |

| VIX | 17.17 | 1.81 | 11.78% |

| Gold | 3,597.10 | 4.9 | 0.14% |

| Oil | 65.6 | 0.01 | 0.02% |

OVERVIEW OF THE US MARKET

U.S. stocks fell to start September after renewed inflation and debt concerns sparked a global bond selloff.

The tech-heavy Nasdaq composite led declines, closing down 0.8% after losing nearly 2% earlier in the day. The S&P 500 was 0.7% lower, while the Dow Jones Industrial Average dropped 249 points, or 0.5%.

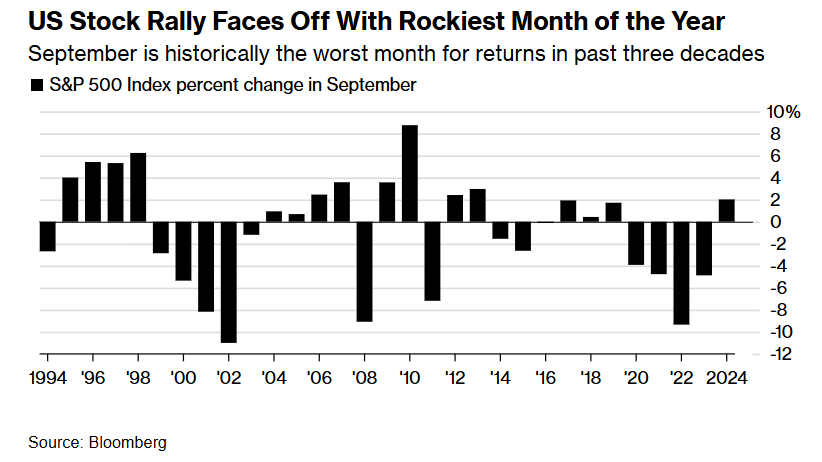

It was a fitting start to September, which has been the worst-performing month for the S&P 500 over the past decade with an average loss of 2%, according to UBS.

Markets entered September under pressure, with gold hitting record highs, bond yields climbing, and equities softening as investors grew more cautious. The surge in gold reflects expectations of Federal Reserve rate cuts and unease over the central bank’s independence. Long-dated bond yields, including U.K. gilts at their highest since 1998, signaled mounting concerns over fiscal sustainability and inflation risks.

Geopolitics also featured prominently. Russia’s Gazprom announced a long-awaited pipeline deal with China and plans to expand other delivery routes, bolstering Moscow’s strategic partnership with Beijing and marking a political win for the Kremlin. In the corporate sphere, Nestlé’s dismissal of CEO Laurent Freixe after only a year, due to an undisclosed affair, underscored instability at the world’s largest food company, sending its shares lower. Tesla’s expansion into India disappointed, with just over 600 cars ordered since its July launch, raising doubts about its growth outlook. Meanwhile, U.S. Treasury Secretary Scott Bessent floated the possibility of declaring a national housing emergency, an issue likely to resonate with voters ahead of midterm elections.

Markets face a pivotal stretch, with jobs data, inflation readings, and the Fed’s September policy meeting all due within the next two weeks. September is historically the weakest month for stocks, but so far, momentum remains intact. Despite dipping at the end of last week, the S&P 500 is up nearly 10% year-to-date, having gained 30% since April lows. Volatility is subdued, with no 2% pullback in 91 sessions — the longest streak since July 2024.

Investors appear reassured that trade frictions and labor market cooling are not derailing growth. Instead, expectations of Fed easing have reinforced confidence in the economy’s resilience. Charles Schwab’s Omar Aguilar noted that tariffs’ impact looks less damaging than feared, and stronger fundamentals are helping sustain optimism. Still, with central bank decisions and political risks looming, September could prove decisive for the market’s direction.

OVERVIEW OF THE AUSTRALIAN MARKET

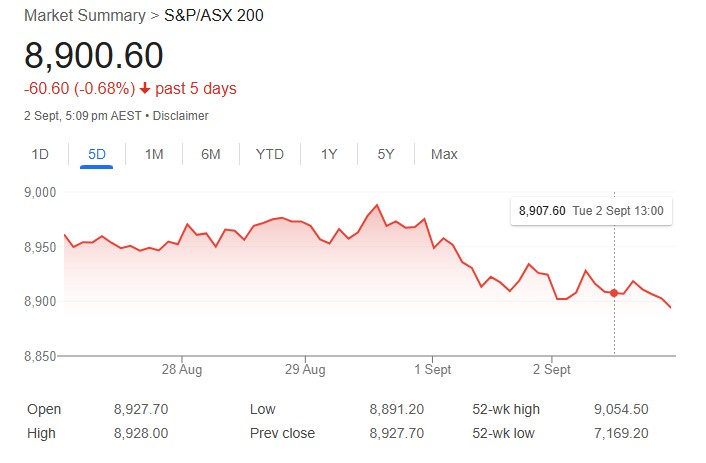

The Australian share market fell modestly on September 2, 2025, hampered by ex-dividend drags on major retailers and weak breadth amid a US holiday lull, though financials and gold provided some support. The S&P/ASX 200 dropped 0.30% to 8,900.6, 0.31% from its high and 0.11% from the low, while the broader All Ordinaries declined 0.31% to 9,168.0. Small-caps slipped with the Small Ords down 0.36%, and breadth was poor as advancers lagged decliners 98 to 180 in the ASX 300.

Financials led with a 0.42% gain, buoyed by big banks: CBA (+0.9%), NAB (+1.0%), Westpac (+0.8%), though ANZ dipped 0.3%. Information Technology rose 0.35%, but Consumer Discretionary plunged 1.89% as ex-divs hit, Wesfarmers (-2.9% ex $1.11), Domino’s Pizza (-0.8% ex $0.215). Consumer Staples fell 1.66% with Woolworths (-3.1% ex $0.45), Endeavour (-2.9% ex $0.063). Real Estate dropped 1.18%, Communication Services -1.12%, Health Care -0.83%. Materials flat at -0.01%, but gold shone amid $US3,578 record high post-Trump’s inflation claims, lifting Evolution Mining (+0.8%), Ramelius Resources (+2.7%), Northern Star (-1.2%).

Standout movers included DUG Technology (+25.3%) on SaaS/HPCaaS award, Invictus Energy (+22.2%) after national project status, Cettire (+16.9%) on director buy, Felix Gold (+15.4%), LTR Pharma (+15.2%), Aeris Resources (+13.6%), West Wits Mining (+13.4%), Dateline Resources (+13.0%), Omega Oil & Gas (+12.8%), Falcon Metals (+10.5%), Polynovo (+10.3%) on Medicare proposal, Nanoveu (+10.0%). Laggards featured Coronado Global Resources (-9.6%), Dorsavi (-9.4%), Gateway Mining (-9.3%), Caprice Resources (-8.7%), Lion Rock Minerals (-8.2%), Waratah Minerals (-7.7%), Novonix (-6.9%), Decidr Ai Industries (-6.7%), Austin Engineering (-6.6%), Peninsula Energy (-5.7%), Kaili Resources (-5.5%).

The AUD/USD fell 0.19% to 0.6541. Q2 current account deficit narrowed to -13.7B (better than -16B poll), net exports contributed +0.1% (vs 0%), signaling external strength ahead of tomorrow’s GDP (0.5% QQ expected). US ISM Manufacturing at 48.7 (below 49 poll) points to contraction.

For August, the ASX 200 rose 2.64%, its strongest month since May, driven by earnings resilience and sector rebounds amid global volatility, though ex-divs and tariff risks cloud September outlook.

Investors eye escalating Ukraine-Russia tensions delaying ceasefires, boosting gold as a haven, while Trump’s Fed pressures and tariff extensions add uncertainty.

Strategists from HSBC, Morgan Stanley, and UBS hold bullish views, citing earnings, tariff clarity, and AI to fuel gains, despite valuations.

Goldman Sachs warns tariffs could sting equities despite deals, suggesting diversification as recession risks fade but premiums rise.