| Price | Change | % Chg | |

|---|---|---|---|

| Dow | 44,938.31 | 16.04 | 0.04% |

| S&P 500 | 6,395.78 | -15.59 | -0.24% |

| Nasdaq | 21,172.86 | -142.1 | -0.67% |

| VIX | 15.69 | 0.12 | 0.77% |

| Gold | 3,389.60 | 1.1 | 0.03% |

| Oil | 63.14 | 0.79 | 1.27% |

OVERVIEW OF THE US MARKET

Asian equities were set for a subdued start on Thursday, with Japan’s futures slightly lower while Chinese and Australian benchmarks inched higher. The cautious tone followed a choppy Wall Street session where bonds outperformed stocks ahead of the Federal Reserve’s annual Jackson Hole gathering.

The S&P 500 fell 0.2% and the Nasdaq 100 dropped 0.6%, dragged by technology stocks, while Treasuries rallied, pushing the 10-year yield two basis points lower. A gauge of US-listed Chinese shares gained, bucking broader weakness.

The dollar was little changed, the yen held steady, and oil prices rose after data showed a drawdown in US stockpiles. Traders largely dismissed inflation concerns highlighted in the Fed’s July meeting minutes, maintaining bets on a September rate cut. However, investors are cautious as Fed Chair Jerome Powell’s upcoming Jackson Hole remarks could challenge dovish expectations. Analysts warned that Powell may reiterate hawkish signals, potentially cooling optimism.

The Fed minutes showed most policymakers viewed inflation risks as outweighing labor market concerns, underscoring divisions within the committee as tariffs and political pressures mount. Officials acknowledged weakening employment but stressed vigilance on price stability. Evercore’s Marco Casiraghi noted the Fed remains “well positioned” to act if conditions deteriorate, with a rate cut in September likely unless inflation accelerates unexpectedly.

Political tensions also loomed, with President Trump continuing attacks on Powell and calling for Governor Lisa Cook’s resignation over mortgage fraud allegations, which she rejected.

Meanwhile, US equities faced renewed pressure from the “Magnificent Seven” megacap tech firms, whose fourth straight day of declines weighed on the Nasdaq and dragged the S&P 500 into its fourth consecutive loss. Analysts warned that tech weakness threatens broader market stability, with some strategists suggesting rotation may ultimately push investors toward cash rather than other sectors.

OVERVIEW OF THE AUSTRALIAN MARKET

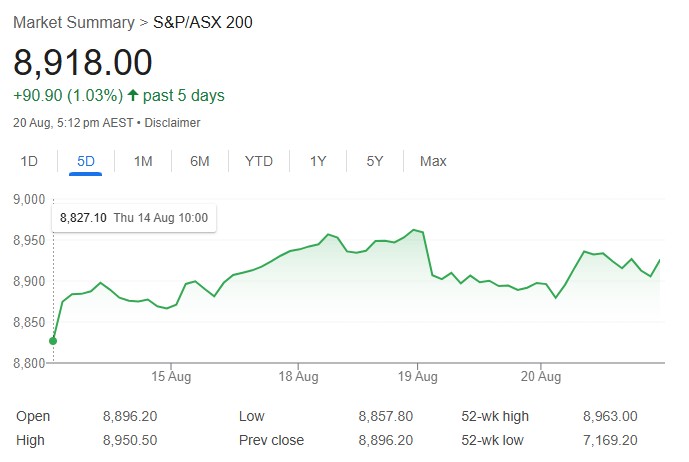

Australia’s share market edged higher on August 20, 2025, rebounding from an early slide as interest rate-sensitive sectors like Consumer Discretionary and Real Estate drew inflows amid lower rate expectations, offsetting drags from resources and health care in a rotation toward defensives. The S&P/ASX 200 rose 0.25%, or 21.8 points, to 8,918.0, while the broader All Ordinaries gained 0.04% to 9,177.4. Advancers outnumbered decliners 139 to 129 on the S&P/ASX 300, though breadth was muted.

Seven of 11 sectors advanced, led by Consumer Discretionary (+1.93%), Real Estate (+1.80%), and Financials (+1.43%). Materials slumped 2.32%, Health Care -1.23%, and Information Technology -1.28%. Consumer Discretionary: Lottery Corporation surged on results. Financials: big banks higher. Materials: James Hardie Industries plunged -27.8% on weak sales, critical minerals hit hard—Pilbara Minerals -7.9%, Lynas Rare Earths -7.4%—amid lithium futures drop. Health Care: continued weakness.

Standouts: Lynch Group (+24.0%) on FY25 results, HMC Capital (+17.7%) rebound post-downgrade, Centuria Capital Group (+11.6%). Decliners: Strike Energy (-12.5%) on impairment, Step One Clothing (-25.5%) FY25 miss, Arafura Rare Earths (-13.6%) on placement.

August flash PMIs showed expansion: Manufacturing at 52.9 (up from 51.3), Services 55.1, Composite 54.9, bolstering soft landing views post-RBA’s 3.60% cut. Aussie dollar flat at 64.92 US cents. US housing starts beat at 1.428 million (vs. poll 1.29 million), signaling strength.

Moomoo’s Michael McCarthy notes tech shield from US selloff, consumer confidence high since February 2022 feeding buys, but high bar for earnings justifying records with BHP, Woodside tomorrow. AMP’s Oliver sees easing positive sans recession, but volatility from valuations/Trump wars. Journal study: P/E spreads 75% returns-driven, urging discount focus as ASX corrects.