| Name | Daily Close | Daily Change | Daily Change (%) |

|---|---|---|---|

| Dow | 44,323.07 | -19.12 | -0.04% |

| S&P 500 | 6,305.60 | 8.81 | 0.14% |

| Nasdaq | 20,974.17 | 78.52 | 0.38% |

| VIX | 16.65 | 0.24 | 1.46% |

| Gold | 3,399.60 | -6.8 | -0.20% |

| Oil | 66.6 | -0.6 | -0.89% |

OVERVIEW OF THE US MARKET

The start of a busy week for Corporate America saw stocks giving up most of their gains, with traders looking for signs of resilience in earnings amid tariff risks. Treasury yields fell alongside the dollar.

While the S&P 500 closed above 6,300 for the first time, the gauge rose just 0.1%. Energy shares joined a decline in oil. Chipmakers almost erased their advance as Nvidia Corp. slipped. Fellow megacaps Tesla Inc. and Alphabet Inc. will kick off the group’s earnings season this week. The stakes will again be high as investors look for updates on artificial-intelligence spending.

Investors also kept a close eye on tariff headlines. President Donald Trump may issue more unilateral tariff letters before Aug. 1, White House Press Secretary Karoline Leavitt said. More trade deals may also be reached before the deadline, she added.

Verizon’s results headlined Monday’s market action, with the telecom firm’s stock rallying 4% after it raised its earnings forecast. Shares of Cleveland-Cliffs rose 12% after the steel producer posted a smaller-than-expected quarterly net loss and said it hired JPMorgan to explore the sale of plants, including three it recently idled in Illinois and Pennsylvania.

Strong earnings also helped power stocks to records last week, with tariff-driven market volatility boosting profits at banks and brokerages. Of the S&P 500 companies that had reported as of Friday, 83% posted higher-than-expected earnings per share, according to FactSet. This week, more than 100 companies in the index are reporting, with Alphabet and Tesla kicking off results from the Magnificent Seven.

OVERVIEW OF THE AUSTRALIAN MARKET

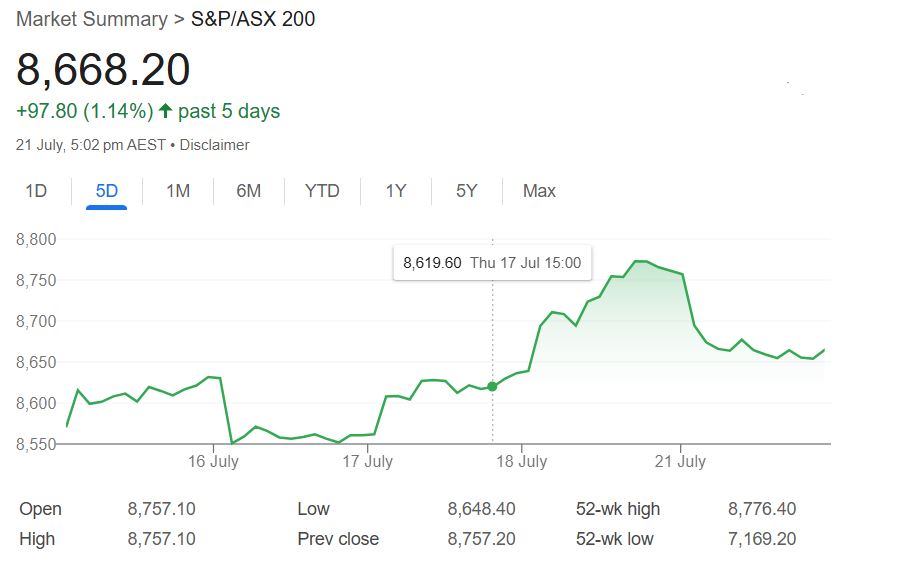

The ASX 200 slid 1.02% to 8,668.2 on Monday, July 21, 2025, as financials bore the brunt of valuation concerns, overshadowing gains in energy and materials sectors amid a choppy session. The Australian dollar edged up 0.08% to 0.6512, supported by steady US futures, with the S&P 500 up 0.13% to 6,343.25.

Financials (-2.26%) led the decline, with banks under pressure—Westpac fell 3.6%, Commonwealth Bank 2.5%, ANZ 2.5%, and National Australia Bank 2.4%—amid stretched valuations. AMP bucked the trend, surging 9.8% to $1.69, a five-month high, after strong Q2 results and positive superannuation inflows. Materials (+0.32%) showed resilience, with Fortescue Metals up 1.7%, Rio Tinto 1.2%, and BHP 0.4% higher as iron ore futures jumped 3.3% to $US104.10 on China’s hydropower project news. Energy gained 1.19%, though breadth remained negative with only two sectors higher.

Takeover activity drew attention, with Insignia Financial dropping 5.8% amid ongoing $3.4 billion talks with CC Capital, though no firm offer is assured. Markets now eye tomorrow’s Australian PMI flash data and US existing home sales at midnight AEST.