| Name | Price | Change | % Chg |

|---|---|---|---|

| Dow | 46,381.54 | 66.27 | 0.14% |

| S&P 500 | 6,693.75 | 29.39 | 0.44% |

| Nasdaq | 22,788.98 | 157.5 | 0.70% |

| VIX | 16.1 | 0.65 | 4.21% |

| Gold | 3,780.70 | 5.6 | 0.15% |

| Oil | 62.64 | -0.04 | -0.06% |

OVERVIEW OF THE US MARKET

Wall Street advanced on September 22, 2025, with tech powering records as Nvidia’s $100 billion OpenAI pledge rekindled AI bets, though calls for a breather grow amid $15 trillion rally since April and tariff drags. The S&P 500 rose 0.44% to 6,693.75—its 28th 2025 record—the Nasdaq Composite climbed 0.70% to 22,788.98, and the Dow Jones Industrial Average added 0.14% to 46,381.54. Information technology surged 1.74%, utilities 0.92%, and industrials 0.38%, while consumer staples lagged -0.89%. Actives saw Opendoor Technologies down 12.43%, Nvidia up 3.93%, and Snap 4.53%.

Broad gains came despite muted bonds ahead of Friday’s PCE, forecast at 0.2% core MM—easing from 0.3%—offering Fed room for labor focus, per TD’s Oscar Munoz on moderating spending. Nvidia’s 4% rally highlighted AI optimism, but Goldman’s Tony Pasquariello warned against fighting mega-cap tech amid tactical risks. St. Louis Fed’s Alberto Musalem sees limited cut space with elevated inflation, contrasting Governor Stephen Miran’s aggressive easing push to avert job losses. Cleveland’s Beth Hammack urges caution against overheating.

Goldman’s David Kostin hiked S&P targets to 6,800 three-month, 7,000 six-month, citing 15% median returns post-non-recessionary cuts. RGA’s Rick Gardner notes bucking September weakness via cuts, earnings, growth, but E*Trade’s Chris Larkin eyes Goldilocks data—soft but not recessionary—for volatility avoidance near highs. Morgan Stanley’s Michael Wilson shifts focus to Fed’s 2026 inflation tolerance amid “run it hot” administration, potentially boosting earnings. UBS’s Mark Haefele sees S&P at 6,800 by June 2026 base, 7,500 bull, but consolidation likely post-run. Deutsche’s Parag Thatte flags climbing positioning without extremes, while Silvant’s Michael Sansoterra buys tech like Broadcom, betting slowdown needed to rattle expectations. CFRA’s Sam Stovall flags 5.5% average year-end gains post-20 records, though October bumps loom.

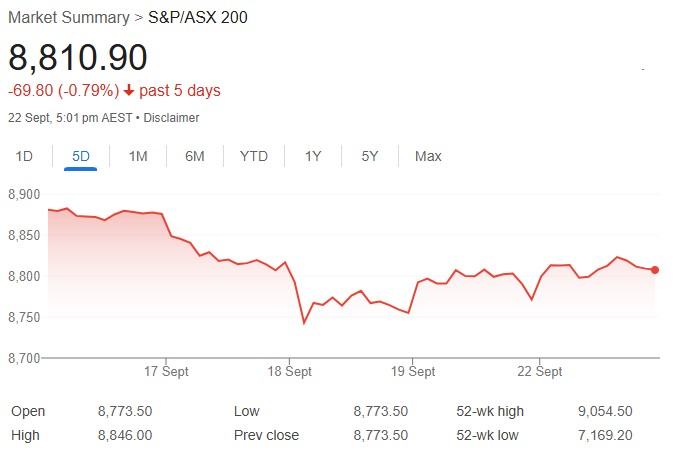

OVERVIEW OF THE AUSTRALIAN MARKET

Australian shares climbed on September 22, 2025, led by a surge in materials as commodity prices buoyed miners, gold, and uranium plays, offsetting softer sectors amid choppy trade and ahead of Wednesday’s CPI data. The S&P/ASX 200 rose 0.43% to 8,810.9, while the broader All Ordinaries gained 0.45% to 9,102.1. Materials jumped 2.60%, with iron ore giants Fortescue up 3.2%, Rio Tinto 2.6%, and BHP 1.0% amid China’s trader urging mills to avoid a BHP product. Gold miners shone with Genesis Mining rocketing 13.7%, Northern Star 8.2%, and Evolution 6.3%, as bullion hit $3,720 an ounce. Uranium names like Silex Systems 3.8%, Paladin 4.6%, and Boss Energy nearly 7% tracked price gains.

Decliners edged advancers 141 to 136 in the ASX 300, reflecting indecision with the benchmark at its session midpoint. Energy slipped 0.70% despite Santos edging 0.4% on Barossa first gas, weighed by Viva Energy down 8.1% on leadership changes and Woodside off 1.0%. Real estate lagged 0.73% with Goodman Group lower. Top gainers included Island Pharmaceuticals up 12.6% sans news, Peninsula Energy 12.5% amid uranium strength, and Energy Transition Minerals 12.3%. Decliners featured Regis Healthcare down 26.2% on funding and FY26 outlook, Focus Minerals 9.3% post-rally pullback, and Torque Metals 9.1%.

The early spike faded, per IG’s Tony Sycamore, with ASX underperformance potentially attracting month-end rebalancing. August’s labor miss lingers, but Wednesday’s weighted CPI YY expected at 2.9%—up from 2.8%—may test RBA’s November cut odds at 80%. The AUD/USD dipped 0.04% to 0.6591, as greenback recovery and tariff talks per Bessent’s 90-day extension option weigh.