| Name | Daily Close | Daily Change | Daily Change (%) |

|---|---|---|---|

| Dow | 47,207.12 | 472.51 | 1.01% |

| S&P 500 | 6,791.69 | 53.25 | 0.79% |

| Nasdaq | 23,204.87 | 263.07 | 1.15% |

| VIX | 16.37 | -0.93 | -5.38% |

| Gold | 4,126.60 | -11.2 | -0.27% |

| Oil | 61.44 | -0.06 | -0.10% |

OVERVIEW OF THE US MARKET

Wall Street rallied to fresh highs on October 24, 2025, as cooler-than-expected inflation data reinforced bets on Federal Reserve rate cuts, overshadowing mixed earnings and an oil dip. The S&P 500 climbed 0.8%, briefly topping 6,800 for a new all-time peak, while the Nasdaq Composite rose 1.2% and the Dow Jones Industrial Average gained 1%. Information technology led with a 1.6% advance, boosted by Intel’s upbeat outlook despite challenges, but energy fell 1% as crude slipped 0.6%. Communication services added 1.3%, financials rose 1.1%, but consumer staples and materials declined over 0.4%.

The September core CPI rose 0.2% monthly—below the poll’s 0.3%—and 3% annually, down from the expected 3.1%, with the headline up 0.3%, signalling contained pressures despite tariffs, according to Goldman Sachs’ Lindsay Rosner, who noted little to spook the Fed. Consumer sentiment fell to a five-month low of 53.6 on persistent high prices, per University of Michigan, yet S&P Global PMIs showed business activity pickup, underscoring economic resilience. Beyond Meat extended its losses, down 23.1% amid volatility, while Ford surged 12.2% on signals of supplier recovery, and Opendoor jumped 13.4%. Procter & Gamble beat sales on resilient demand, GM raised guidance but cut jobs, and Target restructured with 8% corporate cuts.

Trade talks progressed as US and Chinese officials met in Kuala Lumpur to avert escalation ahead of Trump-Xi summit, with Trump highlighting fentanyl, Taiwan, and Hong Kong’s Jimmy Lai. Interactive Brokers’ Jose Torres saw investors grabbing the bull by the horns for rate cuts, while Glenmede’s Jason Pride noted easing path if jobs risks outweigh inflation. eToro’s Bret Kenwell viewed data as not derailing cuts, with strong earnings like 87% beats supporting mild inflationary growth. Citadel Securities’ Scott Rubner eyed year-end rally from seasonality, buybacks, and retail demand.

With swaps pricing quarter-point cuts October 29 and December, Janus Henderson’s John Kerschner said CPI aids narrative of contained inflation, backing further easing into 2026. Strategists like Pacific Investment Management’s Tiffany Wilding noted modest tariff passthrough due to retail pressures, keeping expectations anchored.

OVERVIEW OF THE AUSTRALIAN MARKET

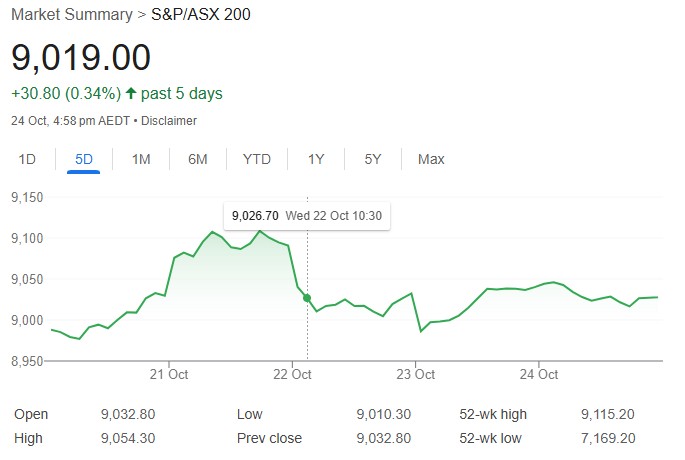

The Australian share market ended slightly lower on October 24, 2025, in a subdued session amid US CPI anticipation, with the S&P/ASX 200 down 0.2% at 9,019 and the All Ordinaries off 0.1% at 9,317.2, yet holding weekly gains of 0.3% after Tuesday’s record close. Information technology rose 1.3% on Nasdaq leads, with Weebit Nano up 6.7% and Wisetech Global gaining 3%, while materials added 0.4% amid lithium bounce. Financials fell 0.5% with ANZ down 1%, health care slipped 1.2%, and consumer staples dropped 0.8%.

Fund flows were muted pre-CPI, with risk-off vibe but technicals showing inflows to ASX stocks, as CVS’s Fiona Clark noted political concerns over Trump-Xi and Canada talks weighing. Energy edged 0.3%, resources up 0.8% with lithium like Core up 14.3% on holder notice, Pilbara 9.1% on quarterly, and Liontown implied strength. Stakk surged 27.5% on revenue growth, Latrobe Magnesium jumped 19.4% on offer, but Mount Gibson plunged 26.6% on operations update, Astron fell 15.3% amid critical minerals weakness.

October manufacturing PMI at 49.7—contraction from 51.4—offset by services rise to 53.1 and composite 52.6, signaling uneven growth per S&P Global. Investors eye local CPI, RBA’s Bullock speech, and global rates next week amid tariff risks and China stimulus hopes lifting metals.