| Name | Price | Change | % Chg |

|---|---|---|---|

| Dow | 46,121.28 | -171.5 | -0.37% |

| S&P 500 | 6,637.97 | -18.95 | -0.28% |

| Nasdaq | 22,497.86 | -75.62 | -0.33% |

| VIX | 16.18 | -0.46 | -2.76% |

| Gold | 3,781.30 | 13.2 | 0.35% |

| Oil | 64.81 | -0.18 | -0.28% |

OVERVIEW OF THE US MARKET

Wall Street paused its recent rally on September 24, 2025, as investors digested mixed corporate news and awaited key economic data amid concerns over labor market slowdown and persistent inflation. The S&P 500 fell 0.28% to close at 6,637.97, ending a streak of near-record highs, while the Nasdaq Composite dropped 0.33% and the Dow Jones Industrial Average declined 0.37%. Energy stocks led gains with a 1.23% rise, buoyed by higher oil prices, but materials tumbled 1.59% and information technology slipped 0.52%.

Lithium Americas Corp. surged 95.77% on reports the Trump administration is pursuing a stake in the company, while Intel gained 6.41% amid talks of investment from Apple. Micron Technology sank despite an upbeat forecast, and Snap fell 2.38%. Traders are eyeing upcoming releases like durable goods orders and GDP final on September 25, with economists forecasting a -0.5% drop in durables and 3.3% GDP growth, alongside initial jobless claims expected at 235,000.

Bank of America strategists noted the S&P 500 trading at expensive levels on 19 of 20 metrics but argued the index’s higher-quality composition supports valuations, suggesting a “new normal” rather than a bubble. Nomura’s Charlie McElligott warned of downside risks from maximum exposures and AI euphoria, while Piper Sandler’s Craig Johnson called for a timeout as momentum fades. Federal Reserve Chair Jerome Powell’s comments on fairly high equity valuations added to caution, though BofA’s Savita Subramanian highlighted potential for a sales and earnings boom to justify multiples.

OVERVIEW OF THE AUSTRALIAN MARKET

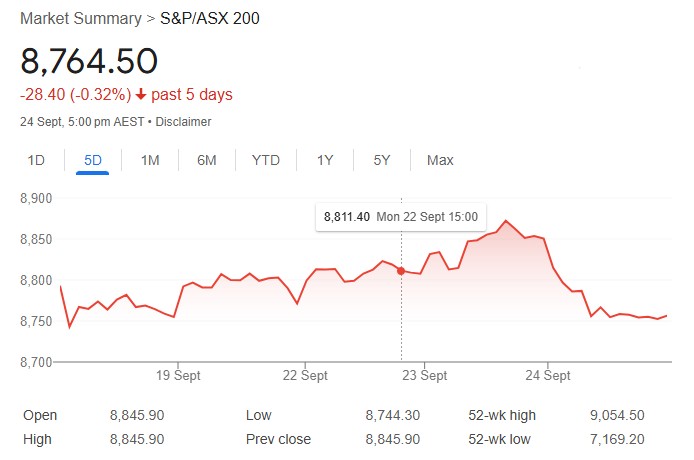

Australian shares snapped a three-day winning streak on September 25, 2025, local time, as hotter-than-expected inflation data dashed hopes for imminent rate cuts and echoed cautious Fed commentary overnight. The S&P/ASX 200 dropped 0.92% to 8,764.5, its worst day since September 3, while the All Ordinaries fell 0.88%. Financials led losses with a 1.76% decline, hit by falls in the big four banks from CBA’s 1.4% drop to Westpac’s 3.2%, but utilities rose 0.53% and energy gained 0.26%.

Lithium and critical minerals stocks shone amid US news on Lithium Americas, with Ioneer up 18.5%, Anson Resources climbing 14.3%, and Pilbara Minerals advancing 5.3%. Gold miners were mixed as prices hit new highs above $3,800 an ounce, while Droneshield jumped 6.2% on Trump’s hawkish UN remarks. The August weighted CPI rose 3.0% year-over-year, beating the 2.9% poll, pushing back RBA cut expectations—Betashares sees no move next week, and NAB now forecasts May 2026.

Resources bucked the trend with a 0.1% gain, supported by BHP and Fortescue edging higher. Earlier PMI flashes showed manufacturing at 51.6, services at 52, and composite at 52.1 for September, indicating expansion but slower than prior readings. Analysts like Capital.com’s Kyle Rodda noted neutral Fed language adding to global caution, with oil’s rise on geopolitical tensions providing some offset.