| Name | Daily Close | Daily Change | Daily Change (%) |

|---|---|---|---|

| Dow | 41,603.07 | -256.02 | -0.61% |

| S&P 500 | 5,802.82 | -39.19 | -0.67% |

| Nasdaq | 18,737.21 | -188.53 | -1.00% |

| VIX | 22.29 | 2.01 | 9.91% |

| Gold | 3,331.50 | -34.3 | -1.02% |

| Oil | 61.31 | -0.22 | -0.36% |

US MARKET

Very much a risk-on market with sectors such as consumer discretionary and technology performing strongly. There was also very broad breadth in the upwards move. The positive market was driven by three key factors: developments in the Japanese bond market, the release of strong US consumer confidence data, and the EU speeding up negotiations on trade. At the close, the S&P 500 rose 2%. The Nasdaq 100 climbed 2.3%. The Dow Jones Industrial Average added 1.5%. Nvidia rallied 3.3% on the eve of its results while Apple Inc. halted its longest selloff in more than three years. The yield on 10-year Treasuries fell 7 bps to 4.44%. The Bloomberg Dollar Spot Index rose 0.4%. Buy equities, buy bonds, buy the dollar – buy US.

Global bonds rallied as Japanese authorities signaled they are considering adjusting their debt plan after a selloff that drove the nation’s long-term borrowing costs to the highest levels in decades. Worries about the ability of governments to cover massive budget deficits weighed on developed-market debt in recent days and, by extension, equities markets.

Meanwhile on the murky world of US economic data currently and what to make of it. Bookings for all durable goods — items meant to last at least three years — fell 6.3%, on a pullback in orders for commercial aircraft. The report underscores caution among businesses as they assess the outlook for demand and focus on cost-cutting in the wake of President Donald Trump‘s trade policy. The value of core capital goods orders, a less-volatile proxy for investment in equipment that excludes aircraft and military hardware, decreased 1.3% last month.

Conversely, US consumer confidence rebounded sharply in May from a near five-year low as the outlook for the economy and labor market improved amid a truce on tariffs. The Conference Board’s gauge of confidence increased by 12.3 points to 98, marking the biggest monthly gain in four years. The figure exceeded all estimates of economists. The cutoff for the survey was May 19, after the US and China agreed to temporarily reduce high levies on each other’s goods while they negotiate a trade deal. About half the responses were collected after the agreement was reached on May 12.

The gauge’s improvement may be an indication that worries about tariffs — a key source of anxiety in the previous surveys — abated in recent weeks. This is likely a slightly confused survey result given timing issues noted above. Friday’s personal consumption expenditures (Core PCE) price index will provide greater clarity on what consumers are actually doing rather than simply saying what they think.

Views of the present job market were more mixed, however. While more respondents said jobs were plentiful in May, there was also a larger share that said jobs were currently hard to get. The difference between these two — a metric closely followed by economists to gauge the job market — narrowed for a fifth month.

A key event this week will be Nvidia Corp.’s results on Wednesday. The chip-making giant is seen as a bellwether for so called growth stocks and the sustainability of the artificial intelligence boom. Its outlook will be crucial given macro risks and tariff uncertainty.

Investors are also gearing up for the Federal Reserve’s preferred inflation measure, the US personal consumption expenditures (Core PCE) price index excluding food and energy, which will be released Friday. The April reading is forecast to rise 0.1% based on consensus expectations.

To keep it really simple, in this environment: What are the Bulls Saying? They’re saying, look, earnings growth this quarter, 13% compared to the same quarter last year, and the Fed is still interested in cutting rates, so it’s okay. And what are the Bears Saying? High valuations and coupled with rising yields that becomes more worrisome. Slowing growth. We started the year at 54 on the PMI composite, now we’re at 51. We all know the soft data’s cratered, so slowing growth and continued geopolitical uncertainty.

OVERVIEW OF THE AUSTRALIAN MARKET

The sharemarket crept higher on Tuesday afternoon, with a rise in US futures and expectations for a soft inflation reading on Wednesday helping to boost sentiment. The S&P/ASX 200 Index lifted 0.3% after having see-sawed in the morning session. Eight of 11 sectors were in the green, led by energy. The All Ordinaries edged up 0.3%.

Australian technology shares extended Monday’s advance and tracked a rise in futures contracts for the technology-heavy Nasdaq. WiseTech rose 1.9% and TechnologyOne was up 2%. Utilities were dragged lower by Origin Energy, which retreated 0.8%. The stock was heavily sold on Monday after it informed investors earnings from its stakes in Australia Pacific LNG and Octopus Energy would be lower than expected.

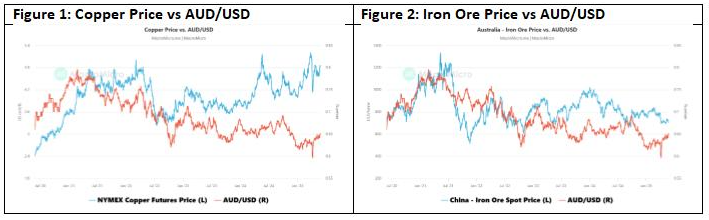

Iron ore miners edged lower while a sell-off in the metal’s price rumbled on Tuesday. BHP was off 0.7% and Fortescue Metals down 0.8%. Copper stocks were some of the index’s best performers following reports an offshore suitor is closing in on Mac Copper – marking the third such bid for an ASX-listed copper stock in the past month. Mac’s shares are in a trading halt. Capstone Copper rose 6.2% and Sandfire rose 2.2%. Higher prices also boosted sentiment, with copper futures in London rising 1.2% to $US9610 a tonne on Monday.

In corporate news, REA Group retreated 1.2% after news emerged the ACCC is looking at whether the News Corp-controlled real estate listings giant has been misusing its market dominance to hike prices unreasonably.

As an aside and as somewhat evident in Figures 1 & 2, both copper and iron ore prices have a high correlation with the AUD, specifically 0.81 and 0.76, respectively.