| Name | Daily Close | Daily Change | Daily Change (%) |

|---|---|---|---|

| Dow | 42,343.65 | 740.58 | 1.78% |

| S&P 500 | 5,921.54 | 118.72 | 2.05% |

| Nasdaq | 19,199.16 | 461.96 | 2.47% |

| VIX | 19.06 | 0.1 | 0.53% |

| Gold | 3,314.40 | 14 | 0.42% |

| Oil | 61.52 | 0.63 | 1.03% |

US MARKET

Wall Street halted its rebound just hours ahead of the highly anticipated results from Nvidia Corp. (after market) — the last of the “Magnificent Seven” megacaps to report. Following a solid rally in the previous session, the S&P 500 retreated, but is now down 5 days out of the last 6. The S&P 500 fell 0.2%. The Nasdaq 100 was little changed. The Dow Jones Industrial Average lost 0.3%. The yield on 10-year Treasuries rose 5 bps to 4.50%. The 30-year rose 5 bps, and is back at the psychologically important 5.0% level. A dollar gauge added 0.2%.

Wednesday’s Nvidia earnings report is pivotal not just for Nvidia but for the entire stock market, as it can rejuvenate investor optimism across the board and help investors to focus on the power of AI and less on headlines out of Washington on tariffs and taxes. It’s hard to recall a time when so many investors were so focused on the earnings outcome of a single stock. The chipmaker’s surge from its April lows hasn’t been accompanied by high volumes, suggesting some investors might have missed out on the rally. An upbeat earnings report would bode well for US stocks as investors have about $7 trillion parked in cash funds.

The EU’s trade chief, Maros Sefcovic, plans to speak to US Commerce Secretary Howard Lutnick and US Trade Representative Jamieson Greer Thursday, seeking to fast-track negotiations to reach a deal before a July 9 deadline. The base case is that pragmatism will ultimately prevail over confrontation.

The S&P 500 is back into positive territory for the year, and just 3.6% off the all-time high recorded on February 19. The market’s belief in the TACO theory – “Trump always chickens out” – grows stronger than ever.

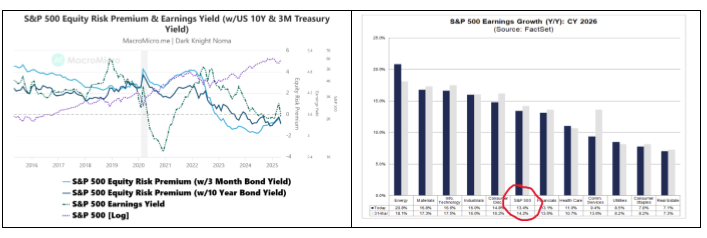

Nothwithstanding the more recent pause, the rally since April 9 has pushed the equity risk premium on the S&P 500 – the difference between the market’s earnings yield (currently 3.54%) and the risk-free 10-year bond yield (currently 4.21%) to -0.91%, the lowest level since October 2009 (bar December 2024 – January 2025). Over the last ten years up until mid 2022, the equity risk prmium was averaging a little over 2%. Investors are still expecting S&P 500 earnings will grow by between 9% and 10% in 2025, and between 13% and 14% across 2026 and 2027. That suggests that returns on equity and profit margins, already at historically high levels, will actually improve from here.

But investors should surely ask themselves how likely it is that US companies can continue to deliver the greatest returns in history and the fastest margins they’ve ever seen, in an environment where tariffs will be higher than they’ve been in a century – even allowing for TACO.

Let’s examine Figure 2 below. Consumer discretionary forward EPS growth for CY2026 of 14.8%!!!! Hello. Information technology EPS growth of 16.6% – some exceptionally strong companies, no doubt, but at what point does the law of very large numbers kick in regarding YoY growth figures?

![]()

Investors are also gearing up for the Federal Reserve’s preferred inflation measure, the US personal consumption expenditures (Core PCE) price index excluding food and energy, which will be released Friday. The April reading is forecast to rise 0.1% based on consensus expectations.

OVERVIEW OF THE AUSTRALIAN MARKET

Profit-taking in the big banks on Wednesday drove the sharemarket lower, erasing earlier gains that were spurred by a rally on Wall Street. After eeking out a marginal 0.1% gain by 10:30am and hitting its highest intraday level since February 19, the S&P/ASX 200 Index then proceeded to slide for the remainder of the trading day, closing down 0.5%. Five of the 11 sectors were trading in the red with financials leading the losses.

Banks shed earlier gains with index heavyweight CBA off 0.6% and MBL down 0.3%, paring its early 1% advance. ASX technology stocks tracked their US counterparts, buoyed by NextDC and TechnologyOne, up 2.5% and 2% respectively. Block rose 4.8%. Iron ore miners were tracking lower after Singapore’s benchmark iron ore contract fell to $US94.90 a tonne, its lowest level in a month. BHP dropped 0.8%. Web Travel Group shares surged 14% after the travel services provider reported strong full-year earnings despite broader macroeconomic headwinds.

Trump said overnight that he was encouraged to hear that European negotiators were accelerating talks with the US. Investor sentiment was further lifted by a Conference Board report showing renewed optimism among US consumers that topped expectations.

On the macro front, the rise in the CPI for April held at 2.4% year-on-year from the previous month (and the previous month) and slightly higher and more ‘sticky’ than expected. Market consensus was for it to slow to 2.3%. Trimmed mean inflation, the RBA’s preferred measure of underlying inflation, inched up to 2.8% in April from 2.7% in March. The RBA’s own forecast has the trimmed mean at 2.6% by Q2. So, inflation is at the very upper end of the RBA’s target band. While it is wise not to read too much into a one month print, we are getting the sense that the pace and quantum of RBA cuts may be less than the market is currently pricing in.

On stickiness of inflation, some global companies are thinking of spreading the additional costs incurred in relation to importing goods into the US across their global networks so as to reduce price rises in the US market. If so, Australia may not be as immune to Trump’s tariffs as initially thought.

The sharemarket was little changed after the new data from the ABS showed April inflation held at the same pace as the prior month. The ABS is due to publish monthly retail sales figures on Friday, which will help gauge the strength of the Australian consumer.

Meanwhile, MST Marquee Australia’s sharemarket is on the precipice of a near-20% collapse as a downturn in company earnings delivers a brutal reality check to sky-high valuations and complacent investors who have been riding the wave of passive money flowing into the ASX. It is the latter point we are most interested in because it is having a significant impact on certain ASX shares, with CBA being the poster child. MST makes the point that over the last two years the Australian equity markets has been carried higher by a combination of buoyant global economic activity, large superannuation inflows and little equitisation, referring to the lack of IPOs pushing more investor money into bigger stocks.

Passive investors, including index funds and benchmark-conscious managers, have poured $US2.2 billion ($3.4 billion) into Australian exchange-traded funds this year, according to JPMorgan. Inbound flows spiked to nearly $US800 billion in April, after Trump announced sweeping tariffs on “liberation day”. An outsized portion of that money has flowed through to the ASX giants, including the banks, helping to explain the strong rally in stocks such as CBA and Wesfarmers, which have both hit record highs this month.