| Name | Daily Close | Daily Change | Daily Change (%) |

|---|---|---|---|

| Dow | 45,544.88 | -92.02 | -0.20% |

| S&P 500 | 6,460.26 | -41.6 | -0.64% |

| Nasdaq | 21,455.55 | -249.61 | -1.15% |

| VIX | 15.36 | 0.93 | 6.44% |

| Gold | 3,516.40 | 42.1 | 1.21% |

| Oil | 64.01 | -0.59 | -0.91% |

OVERVIEW OF THE US MARKET

Wall Street closed lower on August 29, 2025, amid tech-led declines following mixed earnings and in-line inflation data, capping a volatile end to the month. The S&P 500 slipped 0.64% to 6,460.26, ending a choppy session that saw it retreat from recent highs, while the Nasdaq Composite fell 1.15% to 21,455.55 and the Dow Jones Industrial Average dipped 0.20% to 45,544.88. Seven of eleven S&P 500 sectors advanced, led by Health Care (+0.73%), Consumer Staples (+0.64%), and Real Estate (+0.55%), while Information Technology plunged 1.63% and Consumer Discretionary dropped 1.14%.

Actives highlighted Opendoor Technologies (+4.22%) on heavy volume, NVIDIA (-3.32%), Lucid Group (-4.35%), Marvell Technology (-18.60%) after earnings miss, and Nukkleus (+31.98%). Weekly, the Morningstar US Market Index fell 0.03%, with Energy up 2.41% and Financial Services gaining 0.67%, while Utilities slid 1.95% and Consumer Defensives dropped 1.73%. Top weekly gainers included EchoStar (+108.55%), MongoDB (+44.07%), Snowflake (+21.26%), Tilray Brands (+20.00%), and Fortrea Holdings (+18.18%). Losers featured Keurig Dr Pepper (-17.21%), Etsy (-15.40%), Malibu Boats (-15.28%), Marvell Technology (-13.88%), and Hormel Foods (-13.03%).

For August, the S&P 500 gained 1.9%—its best monthly performance since May—amid resilient corporate results and easing Fed concerns, though tariff uncertainties and political pressures tempered gains. The Dow climbed 3.2%, reflecting broader cyclical strength, while the Nasdaq‘s tech-heavy tilt saw more muted advances amid AI volatility.

Personal consumption expenditures data met expectations, with core PCE MM at 0.3% and YY at 2.9% for July, reinforcing soft-landing hopes but highlighting persistent inflation. Investors are monitoring President Trump’s ongoing Fed pressure, including the attempt to fire Governor Lisa Cook over unproven claims, adding to worries about central bank independence amid tariff wars and a swelling budget deficit from recent tax cuts.

Trump’s efforts to influence the Fed, including public criticisms of Chair Jerome Powell for not slashing rates faster, raise alarms about higher long-term inflation and eroded investor trust in US assets, as noted by global managers. This politicization, coupled with the BLS head’s firing, risks undermining data credibility and market stability.

In earnings, Marvell Technology tumbled despite meeting guidance, with revenue up 58% to $2.01 billion; we view the dip as a buying opportunity, maintaining a $90 fair value amid strong AI prospects in custom accelerators and optics, though lumpy orders cloud short-term visibility.

Strategists from HSBC, Morgan Stanley, and UBS maintain bullish long-term outlooks, citing robust earnings, tariff clarity, and AI tailwinds to drive stocks higher into 2026, despite stretched valuations.

Goldman Sachs’ chief global equity strategist warns tariffs could still bite equities even with trade deals, advising diversification as the US dodges recession but faces high valuations.

OVERVIEW OF THE AUSTRALIAN MARKET

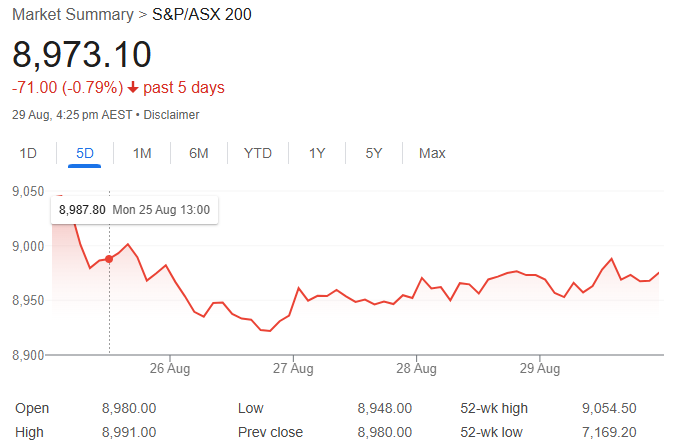

The Australian share market edged modestly lower on August 29, 2025, concluding a volatile earnings season with gains in tech and resources offsetting broader weakness, as investors digested mixed corporate results and awaited global catalysts. The S&P/ASX 200 slipped 0.08% to 8,973.1, mid-range after a 0.28% dip from its low and 0.20% from the high, while the broader All Ordinaries inched up 0.02% to 9,243.0. Small-caps outperformed with the Small Ords rising 0.84%, and breadth favored advancers 157 to 119 in the ASX 300. For the week, the index eked out a 0.06% gain, but August marked a robust 2.6% monthly advance—its strongest since May’s 3.8% surge—driven by resilient earnings amid global tariff uncertainties and U.S. policy risks, though stretched valuations and September seasonality pose correction threats.

Information Technology led sectors with a 3.07% surge, buoyed by NextDC rocketing 17.4% to $16.50 after FY25 revenue beat guidance at $350.2 million, highlighting AI and cloud demand scaling. Energy rose 0.99% and Materials added 0.24%, fueled by battery metals resurgence—lithium stocks like Pilbara Minerals (+6.5%), Liontown Resources (+6.2%), Mineral Resources (+1.4%), and uranium plays including Boss Energy (+7.7%) on FY25 results, Paladin Energy (+7.8%), Deep Yellow (+6.1%), and NexGen Energy (+5.2%) amid supply constraints. Consumer Staples gained 0.42% with Woolworths up 1.6%, but Financials fell 0.57% as big banks weakened—CBA -1.8%, Westpac -1.0%, NAB -0.4%, ANZ -0.1%—despite Morgan Stanley ranking NAB top amid lending rebound. Real Estate lagged at -0.87%.

Notable movers included 4DMedical (+18.8%) on FY25 results, Invictus Energy (+17.2%), St George Mining (+15.4%), Austal (+15.1%) after revenue jumped 24.1% and profit sixfold, Viridis Mining and Minerals (+13.5%), Smartgroup Corporation (+12.0%), Meteoric Resources (+12.0%), Duratec (+11.8%), Harvey Norman (+11.5%) soaring to all-time high on 47% profit rise to $518 million, Falcon Metals (+11.2%), Energy Transition Minerals (+10.5%), Lindian Resources (+10.0%), Eagers Automotive (+9.5%), McMillan Shakespeare (+9.3%), Artrya (+9.2%), Bubs Australia (+9.1%), Caprice Resources (+9.1%), Peak Minerals (+8.8%), American Rare Earths (+8.6%), Arafura Rare Earths (+8.3%), Lotus Resources (+8.1%), Vection Technologies (+8.0%), Bisalloy Steel Group (+7.7%), Qoria (+7.2%), Metals X (+6.7%), Barton Gold (+6.5%), Australian Finance Group (+6.5%), Brazilian Rare Earths (+6.4%), Galan Lithium (+6.3%), Electro Optic Systems (+5.6%), BetaShares Global Uranium ETF (+5.5%). Laggards featured Clinuvel Pharmaceuticals (-15.0%) on investor presentation, Bioxyne (-13.8%), Mesoblast (-9.9%), Pexa Group (-9.3%), Broken Hill Mines (-7.8%), Kaiser Reef (-7.3%), Kaili Resources (-7.0%), Clarity Pharmaceuticals (-6.3%), Lynas Rare Earths (-5.8%) after $750 million placement.

The AUD/USD dipped 0.03% to 0.6531. U.S. PCE data met expectations—core MM +0.3%, YY +2.9%; headline MM +0.2%, YY +2.6%—reinforcing soft landing bets but sparking a Wall Street tech rout, with Nasdaq down 1.2%, S&P 500 -0.6%, Dow -0.2%. Investors eye potential September volatility from U.S. tariffs, debt risks, and Fed policy amid Trump’s central bank pressures.