| Name | Price | Change | % Chg |

|---|---|---|---|

| Dow | 44,632.99 | -204.57 | -0.46% |

| S&P 500 | 6,370.86 | -18.91 | -0.30% |

| Nasdaq | 21,098.29 | -80.29 | -0.38% |

| VIX | 15.98 | 0.95 | 6.32% |

| Gold | 3,327.30 | 3.3 | 0.10% |

| Oil | 69.17 | -0.04 | -0.06% |

OVERVIEW OF THE US MARKET

Wall Street closed lower on July 29, 2025, as mixed corporate earnings and economic data weighed on investor sentiment. The S&P 500 ended its six-day record streak, slipping 0.3%, while the Nasdaq and Dow fell 0.4% and 200 points respectively. Boeing beat earnings expectations, but Spotify, Merck, and UnitedHealth disappointed. UPS dropped over 9% after withholding guidance, and Royal Caribbean fell 8% despite raising its annual outlook.

Consumer confidence rose slightly, but job market concerns persisted. Investors are watching the Federal Reserve’s policy meeting and upcoming Big Tech earnings, with hopes for a rebound later in the year.

Treasury Secretary Scott Bessent said that the US and China will continue talks over maintaining a tariff truce before it expires in two weeks and that Trump will make the final call on any extension. Adding an extra 90 days is one option, Bessent said.

Just as it happened after the US tariff deal with the European Union, the underwhelming market reaction to signs of progress in China talks illustrates the steady decline in the ability of those initiatives to spur big moves on Wall Street.

With the Fed’s benchmark rate holding at a target range of 4.25% to 4.5% since December, the business world is looking for any clue that officials are moving toward a rate reduction in the fall. Fed Chair Jerome Powell could face dissent from one or more colleagues arguing it’s time for the central bank to provide more support to a slowing labor market.

Strategists from HSBC Holdings Plc, Morgan Stanley and UBS Group AG are maintaining their long-term bullish views even as concerns build that valuations have become stretched at the moment. They see strong corporate earnings and economic data, growing clarity around tariffs and the tailwind of artificial intelligence propelling stocks higher into next year.

The chief global equity strategist at Goldman Sachs Group Inc. says it’s possible that tariffs bite hard enough to hurt equity prices even as Washington agrees on deals with key trading partners. And while the US might dodge a recession, valuations are high enough that it’s prudent to keep diversifying into other markets.

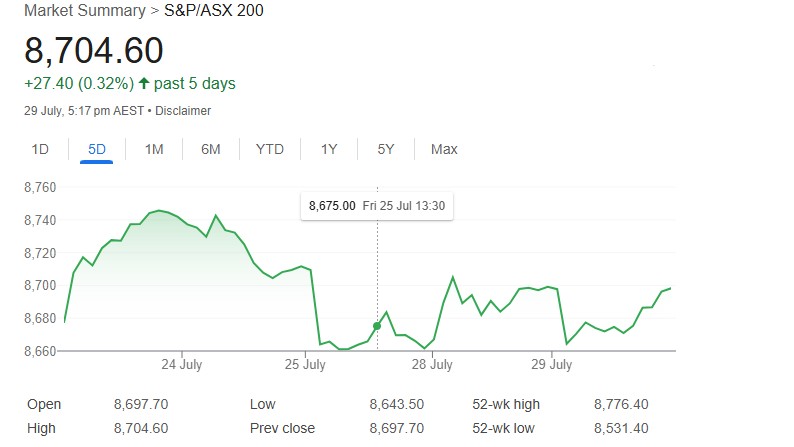

OVERVIEW OF THE AUSTRALIAN MARKET

The S&P/ASX 200 finished slightly higher despite mixed sector performance, as gains in energy and health care offset weakness in real estate and materials.

The broad index rose 0.08% to 8,704.6, recovering modestly from recent volatility. The All Ordinaries edged up 0.04% to 8,966.7, while the All Tech Index gained 0.20% to 4,241.1, showing tech resilience. The Australian dollar weakened 0.21% to 0.6507, reflecting softer commodity sentiment, though US futures rose, with the Nasdaq up 0.25% to 23,550.0

Investors processed market moves on Tuesday, with energy leading gains as Santos rose 2.1% and Woodside 1.6% after solid quarterly reports. Health care added 0.33%, with Pro Medicus up 0.9%, Cochlear 0.8%, and CSL 0.5%, continuing a strong four-week trend. Materials dipped 0.05%, with South32 down 0.99% and BHP steady,

while uranium stocks like Boss Energy fell 5.51% amid waning sector confidence. Lithium stocks stabilized, with Pilbara Minerals down 1.47% but off its low, amid volatile Chinese futures. Focus shifts to Today’s Australian CPI data and US Q2 GDP advance.