| Name | Daily Close | Daily Change | Daily Change (%) |

|---|---|---|---|

| Dow | 42,305.48 | 35.41 | 0.08% |

| S&P 500 | 5,935.94 | 24.25 | 0.41% |

| Nasdaq | 19,242.61 | 128.85 | 0.67% |

| VIX | 18.36 | -0.21 | -1.13% |

| Gold | 3,389.50 | -7.7 | -0.23% |

| Oil | 62.95 | 0.43 | 0.69% |

OVERVIEW OF THE US MARKET

A solid month for stocks is ending on a weak note as Trump said Beijing “totally violated” a tariff agreement, with the market briefly extending its slide after a news report the US plans to broaden restrictions on China’s technology sector. Following a rally that put the S&P 500 on track for its best May since 1990, the index fell as much as 1.2% before paring losses. By close and after a slight rally into the close, the S&P 500 fell 0.1%. The Nasdaq 100 fell 0.3%. The Dow Jones Industrial Average ended up gaining 0.2%. Big tech got hit, with Nvidia Corp. down 3.5%. Action was muted in bonds, though Treasuries were set for their first monthly drop this year. The dollar barely budged, while heading toward a fifth straight month of declines – the longest losing run since 2020.

On the economic front, US consumers hit the brakes in April while goods imports plummeted by a record as companies adjusted to higher tariffs. Inflation-adjusted personal spending rose 0.1% after rising 0.7% a month earlier. Separate data showed an almost 20% slump in imports, leading to a massive narrowing in the US merchandise-trade deficit in April. Meanwhile, the Federal Reserve’s preferred price gauge remained tame. The personal consumption expenditures (PCE) price index, excluding food and energy, increased 0.1% from a month earlier. Compared with a year earlier, the core inflation gauge rose 2.5% from April 2024 — the smallest annual advance in more than four years.

The figures reflect an undercurrent of anxiety among many American consumers about the economy after the weakest quarter for spending in nearly two years. Higher duties on imports had yet to show up more broadly in higher goods prices, as sentiment slumped and the outlook for personal finances stood at a record low. However, in April US businesses pulled back significantly on imports after months of pulling forward economic activity to avoid tariff policy. But here’s the irony, because of the way GDP is calculated, the April slump in imports of goods after months of front loading will likely give a boost to GDP in the second quarter. The Atlanta Fed’s GDPNow forecast pencilled in a 3.8% increase for the second quarter, which would mark a bounceback from the 0.2% drop last quarter.

OVERVIEW OF THE AUSTRALIAN MARKET

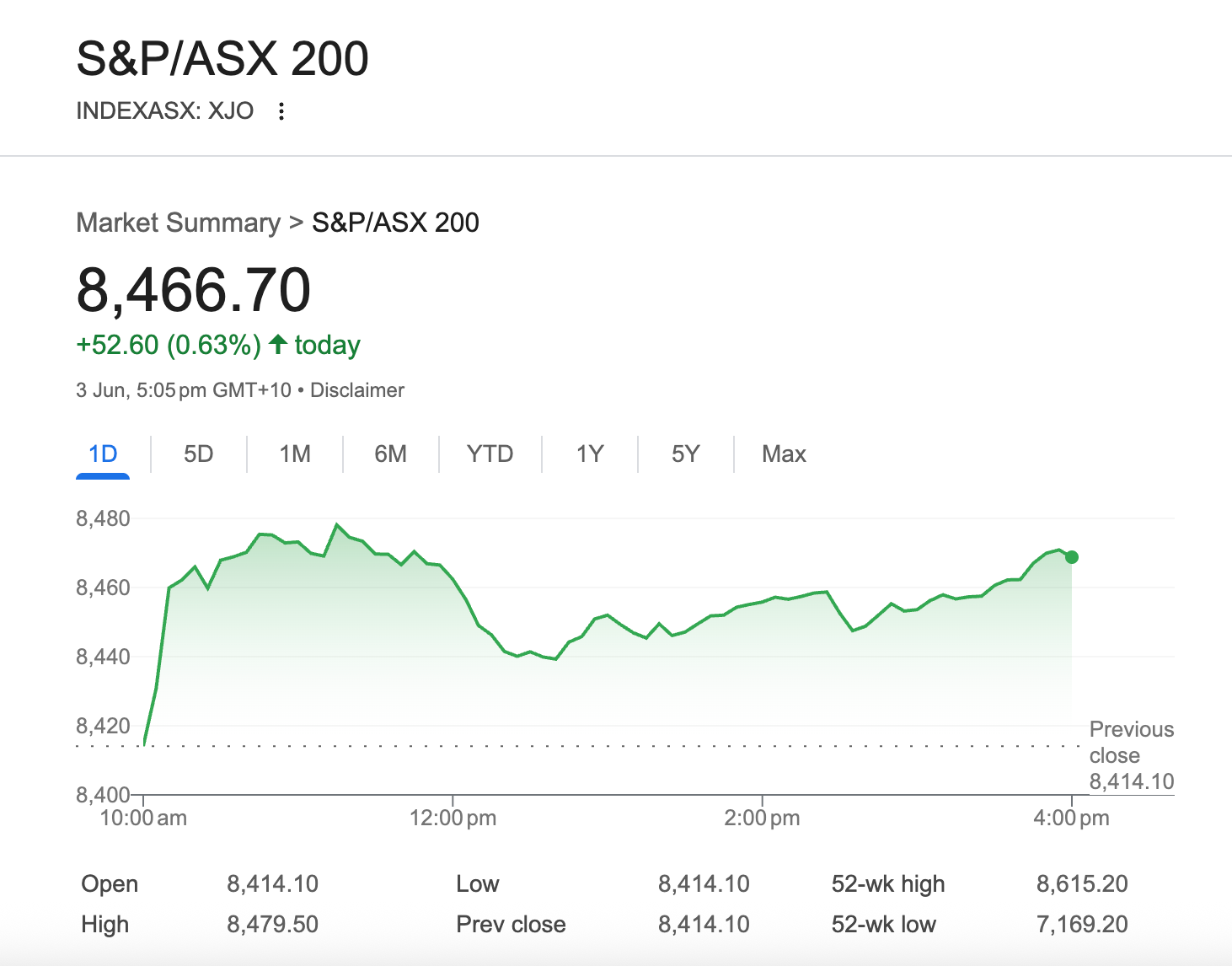

The Australian sharemarket rose for the second consecutive month after a US court blocked American President Donald Trump’s tariffs, adding to hopes that global trade tensions will simmer down. The S&P/ASX 200 Index rose 0.3% on Friday with seven of 11 sectors in the green, led by utilities. The benchmark rallied 3.8% in May, recording its best month since January. The All Ordinaries rose 0.3% on Friday, notching its eighth consecutive weekly gain. During the course of the day however, the S&P/ASX 200 swung between gains and losses before defensive consumer and utilities stocks helped lift the benchmark index. Bank stocks were broadly higher – CBA edged up 0.9% and NAB gained 1.3%. Technology stocks were heavily sold, with WiseTech off 1.5% and Megaport down 3.1%. Energy stocks were dragged lower by Woodside Energy and Santos, which both tracked a steep decline in oil prices. Woodside fell 2.1% and Santos retreated 0.9%.

A surprise fall in retail sales, down 0.1% in April, sent government bond yields plunging 10 bps and helped spur optimism that the RBA will step up interest rate cuts. Retail turnover ended its 2025 run of gains falling -0.1%mth in April to be 3.8%yr higher. The weakness was centred on clothing & footwear and department stores, which the ABS attributed to warmer weather delaying purchases. Retail trade rebounded in Qld (1.4%mth) following weather-related impacts last month. Excluding Qld would have resulted in a -0.5%mth fall in retail turnover. Meanwhile, NSW posted its sharpest decline in over a year. The suspicion is the April read has also been impacted by holiday-related disruptions. Supporting this, the weekly Westpac-DataX Card Tracker showed significant disruptions from the late timing of Easter and its proximity to the ANZAC Day public holiday, spending only stabilising in mid-May.

Meanwhile, the ASX’s quarterly rebalance will be announced next Friday and take effect a fortnight later. Gold stocks have been identified as significant inclusions. For example, Evolution Mining is expected to headline a flurry of changes to the ASX’s biggest indices as gold producer stocks soar amid investor interest in the precious metal as a haven from broader market turmoil. Evolution, which has mines around the country, is set to join the S&P/ASX 50 index in the quarterly rebalance.

Markets are now turning their attention to Q1 GDP figures released next week. Consensus is for growth to slow from 0.6% in Q4 2024 to 0.2% in Q1 2025, largely owing to slower household consumption