| Name | Price | Change | % Chg |

|---|---|---|---|

| Dow | 44,130.98 | -330.3 | -0.74% |

| S&P 500 | 6,339.39 | -23.51 | -0.37% |

| Nasdaq | 21,122.45 | -7.23 | -0.03% |

| VIX | 16.72 | 1.24 | 8.01% |

| Gold | 3,343.60 | -5 | -0.15% |

| Oil | 69.36 | 0.1 | 0.14% |

OVERVIEW OF THE US MARKET

On July 31, 2025, U.S. stock markets closed lower, reversing early gains amid pressure on health care stocks. The S&P 500 fell 0.4% to 6,339.39, while the Dow Jones Industrial Average dropped 0.7% to 44,130.98. The Nasdaq Composite slipped marginally by 0.1%, ending at 21,122.45, and the Russell 2000 declined 0.9%, closing at 2,211.65 1.

The downturn was largely driven by a White House initiative urging major pharmaceutical companies to reduce drug prices within 60 days, which weighed heavily on health care stocks. Despite the broader market decline, Meta Platforms surged after reporting earnings that exceeded Wall Street expectations, fueled by aggressive investments in artificial intelligence 1.

For the week, the S&P 500 and Dow were down 0.8% and 1.7%, respectively, while the Nasdaq edged up 0.1%. Year-to-date, the S&P 500 has gained 7.8%, the Dow is up 3.7%, and the Nasdaq leads with a 9.4% increase. In contrast, the Russell 2000 has declined 0.8% in 2025 1.

The US equity market sector performance was mixed, with notable divergence across industries:

• Health Care was the weakest performer, dragged down by a White House directive urging pharmaceutical companies to cut drug prices within 60 days. This policy pressure led to broad declines in major health care stocks 1.

• Technology showed strength, particularly due to Meta Platforms, which surged after beating earnings expectations and highlighting aggressive AI investments 1.

• Financials continued their strong run, supported by robust earnings and positive growth estimates 2.

• Consumer Staples was the only sector to post negative returns for the month, reflecting weaker demand and margin pressures 2.

• Other sectors like Industrials, Energy, and Consumer Discretionary posted modest gains, buoyed by resilient corporate earnings and optimism around trade negotiations.

Overall, 10 out of 11 S&P 500 sectors delivered positive returns in July, with the broader market showing signs of resilience despite policy headwinds and investor caution. The S&P 500 notched multiple record highs during the month, though momentum slowed toward the end as investors weighed tariff risks and awaited further earnings results

During the session, several major U.S. companies released earnings reports, offering a snapshot of corporate health amid macroeconomic uncertainty:

Big Tech Highlights

• Apple (AAPL) and Amazon (AMZN) reported earnings after market close. While exact figures weren’t disclosed, both were expected to post strong revenue: Apple at $89.17B and Amazon at $162.11B 1.

• Meta Platforms had previously reported better-than-expected results, driven by AI investments 2.

Health & Pharma

• AbbVie (ABBV) and CVS Health (CVS) were among the key health care firms reporting. CVS was forecasted to generate $94.51B in revenue 1.

• Bristol-Myers Squibb (BMY) and Biogen (BIIB) also released earnings, reflecting mixed performance amid regulatory pressures.

Finance & Payments

• Mastercard (MA) posted strong results, with forecasted EPS of $4.03 and revenue of $7.93B 1.

• Cigna (CI) reported robust earnings, expected to hit $62.66B in revenue.

Energy & Industrials

• Shell (SHEL) and Chevron (CVX) were among energy giants reporting, with Shell forecasted at $62.52B in revenue.

• Toyota (TM) and First Solar (FSLR) also featured, reflecting global industrial trends.

OVERVIEW OF THE AUSTRALIAN MARKET

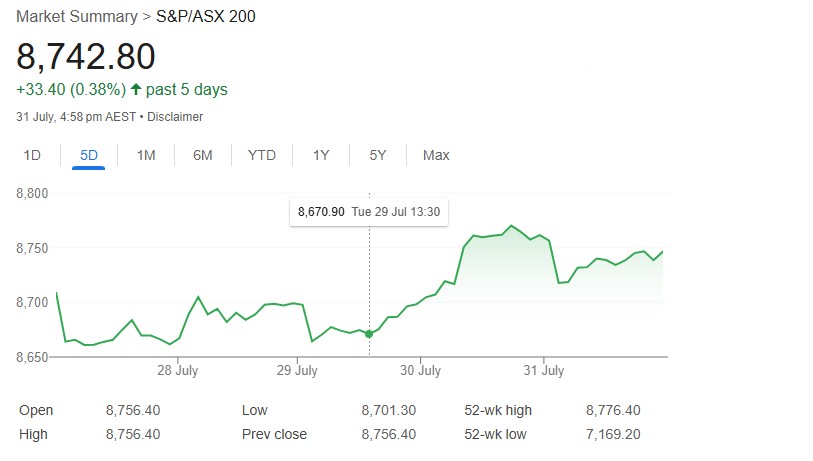

The Australian equity market closed lower on July 31, 2025, as a sharp sell-off in resources weighed on broader indices. The S&P/ASX 200 (XJO) shed 13.6 points to finish at 8,742.8, down 0.16%, trading 0.48% above its session low but just 0.16% shy of its high. The broader S&P/ASX 300 (XKO) reflected a cautious mood, with decliners outpacing advancers by 142 to 127.

The market’s performance was shaped by a reversal in the recent rally for Resources (XJR, -2.56%) and Energy (XEJ, -0.46%), which had gained traction in July but faltered this week. The XJR’s 2.2% drop today, marked by a long black candle, signaled renewed investor caution, driven by softer commodity prices, including iron ore and base metals. Meanwhile, Technology (XIJ, +1.34%) and Consumer Discretionary (XDJ, +1.11%) led gains, continuing a rotation trend observed before the month-long July rally in resources. Standout performers included Life360 (360, +3.2%, +149.0% over 1 year) and Aristocrat Leisure (ALL, +2.4%), buoyed by strong tech sentiment and positive US futures (Nasdaq, +1.32%).

Financials (XFJ, +0.47%) also held firm, with National Australia Bank (NAB, +1.1%) and Suncorp Group (SUN, +1.0%) among the blue-chip winners, supported by expectations of RBA rate cuts following Wednesday’s softer inflation data. The Q2 2025 CPI of 2.1% and RBA Trimmed Mean CPI of 2.7% kept markets optimistic about an August rate cut. However, today’s stronger-than-expected economic releases, including Building Approvals (+11.9% vs. 2% expected) and Retail Sales (+1.2% vs. 0.4% expected), tempered some enthusiasm, hinting at economic resilience that could delay aggressive easing.

Global trade concerns lingered, with US-China trade talks yielding no major breakthroughs and Trump’s proposed 20-25% tariffs on India adding uncertainty for Australian exporters. The AUD/USD rose 0.56% to 0.6469, reflecting cautious optimism but also sensitivity to global risk sentiment.