| Name | Daily Close | Daily Change | Daily Change (%) |

|---|---|---|---|

| Dow | 47,085.24 | -251.44 | -0.53% |

| S&P 500 | 6,771.55 | -80.42 | -1.17% |

| Nasdaq | 23,348.64 | -486.09 | -2.04% |

| VIX | 19 | 1.83 | 10.66% |

| Gold | 3,956.20 | -4.3 | -0.11% |

| Oil | 60.2 | -0.36 | -0.59% |

OVERVIEW OF THE US MARKET

Wall Street closed sharply lower on November 4, 2025, as warnings from top bank CEOs about potential market pullbacks amplified concerns over stretched valuations, triggering a broad selloff led by technology stocks. The S&P 500 tumbled 1.17% to 6,771.55, marking its biggest one-day drop since October 10, while the Nasdaq Composite slid 2.04% to 23,348.64 and the Dow Jones Industrial Average fell 0.53% to 47,085.24. Information Technology plunged 2.27%, with Nvidia down 3.96% and Palantir sinking 7.94% despite raising its outlook, amid Michael Burry’s disclosed bearish puts on both. Hertz surged 36.23% on cost cuts, but Pfizer dipped 1.46%. Super Micro fell after missing estimates, Amgen rose on raised guidance, and Uber dropped 5.1% on legal charges overshadowing growth.

ISM services PMI is due November 5, expected at 50.8, offering labor insights amid the ongoing government shutdown’s data void. Fed divisions deepened, with Powell noting strong differing views on December easing, Goolsbee leery of cuts amid sticky inflation, and Miran pushing for deeper reductions. Senate efforts to reopen government stalled for the 14th time, with Democrats demanding ACA tax credits.

Treasury Secretary comments were absent, but Trump’s pressure on Republicans to end the shutdown and threats to food aid highlighted impasse risks. Wall Street CEOs like Goldman’s Solomon and Morgan Stanley’s Pick flagged 10-20% drawdowns as healthy, echoing Capital Group’s Gitlin on fair-to-full valuations despite strong earnings. Bespoke noted concerns but less scary details, while BMO’s Lyngen, Hartman, and Choi saw sympathy for consolidation amid narrow leadership.

Strategists from Evercore ISI and FHN Financial warned of vulnerability from AI narrative wobbles and unpredictable corrections. Piper Sandler’s Johnson favored buying pullbacks, BTIG’s Krinsky eyed 6,400-6,500 support, and Truist’s Lerner cited historical upside in bull markets past year three, averaging 4.7% November-December gains when up over 15% through October.

OVERVIEW OF THE AUSTRALIAN MARKET

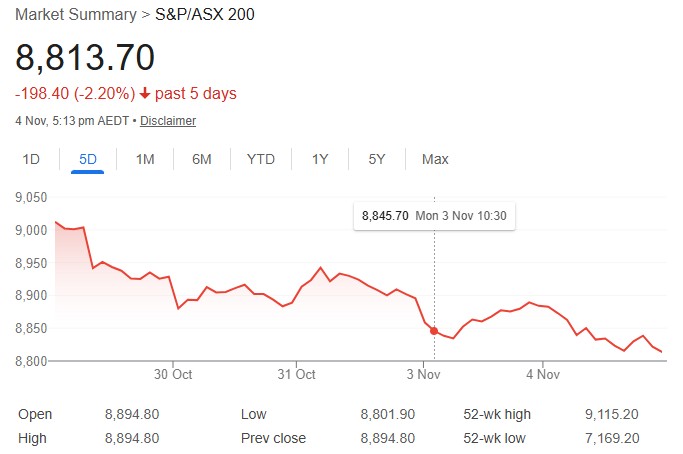

The Australian share market closed sharply lower on November 4, 2025, extending losses to a six-week low as the Reserve Bank held rates at 3.6% with a hawkish tone on persistent inflation, amplifying global risk-off sentiment and commodity weakness. The S&P/ASX 200 dropped 0.91% to 8,813.7, while the All Ordinaries fell 0.92% to 9,098.2, with breadth weak at 61 advancers to 219 decliners. Materials tumbled 1.83% on softer iron ore, copper, and lithium futures down over 5%, dragging BHP 1.9%, Rio Tinto 2.6%, and Fortescue 2.7%. Utilities plunged 2.78% after the government’s free electricity scheme announcement, hitting Origin 3.8% and AGL 3.7%. Health Care edged up 0.04%, buoyed by CSL’s 0.9% gain offsetting losses elsewhere.

RBA Governor Bullock emphasized data-driven caution post-September inflation surge, with forecasts now seeing trimmed mean at 3.2% by June 2026, up from 2.6%, dimming cut hopes. S&P Global services PMI finalized at 53.1 and composite at 52.6, beating polls, signaling expansion. Balance of goods due November 6, expected at A$1.825 billion surplus versus A$4 billion poll, after September exports plunged 7.8%.

Capital.com’s Rodda noted RBA’s concern over inflation above target longer, with Vanguard’s Feng seeing limited 2026 cuts amid full capacity. Standouts included Droneshield up 8.6% on options update, Core Lithium gaining 8.0%, but Novonix down 10.6% on offtake termination and G8 Education off 13.0% on FY25 update.