| Name | Daily Close | Daily Change | Daily Change (%) |

|---|---|---|---|

| Dow | 45,400.86 | -220.43 | -0.48% |

| S&P 500 | 6,481.50 | -20.58 | -0.32% |

| Nasdaq | 21,700.39 | -7.31 | -0.03% |

| VIX | 15.18 | -0.12 | -0.78% |

| Gold | 3,639.80 | -13.5 | -0.37% |

| Oil | 61.97 | 0.1 | 0.16% |

OVERVIEW OF THE US MARKET

Wall Street is heading into Friday’s jobs report with mounting evidence that the U.S. labor market is cooling, reinforcing expectations of Federal Reserve rate cuts and fueling a rally in both equities and bonds. Fresh data showed jobless claims climbing to their highest since June, while ADP reported only 54,000 private-sector payroll additions in August, far below expectations. Challenger, Gray & Christmas also noted hiring plans fell to their weakest August level on record. Consensus forecasts point to nonfarm payroll growth of just 75,000 and an uptick in the unemployment rate to 4.3%, its highest since 2021.

Markets reacted swiftly. The S&P 500 gained nearly 1% to another record, while two-year Treasury yields dropped to their lowest in a year as traders priced in a near-certain September rate cut, with at least two reductions seen by year-end. Analysts warned, however, that the quality of Friday’s data matters: modest deceleration could support the “Goldilocks” scenario of easing without recession risk, but sharper deterioration might stoke concerns about stagnation or stagflation.

Federal Reserve officials are signaling readiness to act. Governor Christopher Waller, among the most vocal proponents of cuts, said labor demand may be on the edge of a sharp decline. New York Fed President John Williams echoed that easing will become appropriate “over time.” Meanwhile, President Trump’s nominee for the Fed Board, Stephen Miran, emphasized central bank independence while stressing the Fed’s core mandate to prevent depressions and hyperinflation.

Elsewhere, U.S. service-sector activity showed resilience, expanding at the fastest pace in six months, suggesting consumer-driven demand remains intact despite labor market strains. Still, political and legal drama added tension: the Justice Department launched a criminal probe into Fed Governor Lisa Cook over alleged mortgage fraud, intensifying Trump’s efforts to reshape the central bank.

In corporate developments, Broadcom offered a bullish outlook, Tesla rolled out its robotaxi app to the public, and Microsoft moved closer to resolving an EU antitrust case. Boeing escalated its strike standoff by hiring replacements, while American Eagle surprised with strong sales. Commodities were mixed, with gold easing slightly after recent highs and oil prices slipping on OPEC+ supply concerns.

Overall, investors remain focused on Friday’s payrolls as the decisive catalyst. Softer-than-expected numbers would reinforce the bond rally and strengthen the case for imminent Fed cuts, but a sharper downturn risks unsettling markets. For now, equities, bonds, and rate expectations are aligned around the view that policy easing is coming — the question is how fast and how far.

OVERVIEW OF THE AUSTRALIAN MARKET

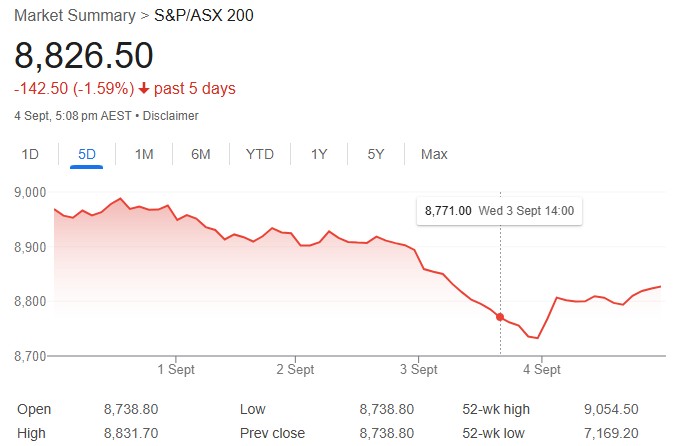

Australia’s share market rebounded on September 4, 2025, clawing back some of the losses from the previous day’s sharp decline, as easing pressures in global bond markets provided relief to interest rate-sensitive sectors. The S&P/ASX 200 climbed 87.7 points, or 1.0%, to close at 8,826.5, while the broader All Ordinaries added 81.3 points, or 0.9%, to 9,091.4. The session marked a reversal from Wednesday’s 1.8% slump in the ASX 200, which had been driven by a spike in bond yields amid concerns over persistent inflation and potential delays in global rate cuts.

Nine of the 11 sectors finished higher, with financials leading the charge at +1.71%, followed by consumer discretionary (+1.39%), information technology (+1.28%), and health care (+1.11%). Real estate and consumer staples also advanced, up 1.07% and 1.03% respectively. The big banks powered the financials sector, with Commonwealth Bank, Westpac, and NAB each gaining over 2%, alongside Macquarie Group. In IT, Xero surged 4.8% to $157, recovering from a more than 6% drop the day before, though Megaport slid 6.3% and NextDC dipped 2.4%. Real estate benefited from rebounds in Goodman Group, Scentre, and Vicinity Centres.

Materials edged down slightly by 0.02%, despite gains in Fortescue and Rio Tinto as iron ore futures topped $US104 per tonne, but BHP fell 0.7%. Gold miners weakened as the metal retreated from an overnight peak of $US3,578 per ounce to around $US3,537, with the sector reflecting broader defensive positioning. Energy stocks eked out a 0.13% gain after an initial dip, with Santos up 0.3% offsetting Woodside’s 0.7% decline amid a 3% drop in oil prices tied to expected OPEC production increases. Consumer staples were buoyed by Woolworths’ 1.7% rise to $27.67, while Wesfarmers lifted consumer discretionary with a 2.5% advance to $90.91.

Among notable movers, MTM Critical Metals jumped 20.4% after announcing a former US Deputy Assistant Secretary of Defense joining its advisory board, aligning with its uptrend. Sunrise Energy Metals rose 19.8% ahead of a trading halt, and Brazilian Rare Earths gained 17.5% on continued momentum from securing a rare earth pilot plant permit. On the downside, Lotus Resources tumbled 20.0% following an equity raising presentation, Catalyst Metals dropped 13.0% after a broker downgrade, and several gold-related names like Falcon Metals (-12.0%) and Meeka Metals (-10.5%) fell without specific news.

The Australian dollar strengthened slightly to 65.24 US cents from 65.11 cents the previous afternoon, trading near the upper end of its recent range against the greenback. Market breadth improved markedly, with advancers outpacing decliners 190 to 83 in the ASX 300, mirroring the prior session’s reversal. Several companies, including BHP Group and Amcor, commenced ex-dividend trading.