| Name | Daily Close | Daily Change | Daily Change (%) |

|---|---|---|---|

| Dow | 45,400.86 | -220.43 | -0.48% |

| S&P 500 | 6,481.50 | -20.58 | -0.32% |

| Nasdaq | 21,700.39 | -7.31 | -0.03% |

| VIX | 15.18 | -0.12 | -0.78% |

| Gold | 3,639.80 | -13.5 | -0.37% |

| Oil | 61.97 | 0.1 | 0.16% |

OVERVIEW OF THE US MARKET

Wall Street ended lower on September 5, 2025, after a weaker-than-expected jobs report heightened concerns over economic slowdown and amplified calls for Federal Reserve rate cuts. The Dow Jones Industrial Average fell 0.48% to 45,400.86, the S&P 500 slipped 0.32% to 6,481.50, and the Nasdaq Composite edged down 0.03% to 21,700.39. Communication services rose 0.55%, while energy tumbled 2.06% and financials dropped 1.84%. Actives included Opendoor Technologies up 11.58% on high volume, Nvidia down 2.70%, and Kenvue falling 9.35%.

Non-farm payrolls rose just 22,000 in August, well below the 75,000 forecast, with unemployment steady at 4.3%, the highest since 2021. The data solidified expectations for a September rate cut, with markets pricing in a potential 50 basis-point move. For the week, the Morningstar US Market Index gained 0.42%, with communication services up 3.64% and energy down 3.13%.

Top gainers featured Ionis Pharmaceuticals surging 45.16% on strong performance, Macy’s up 30.09%, and SanDisk rising 24.61%. Losers included Endava down 30.65%, Lululemon Athletica falling 17.01% after cutting guidance amid tariff impacts, and Tilray Brands dropping 13.77%. Gold miners hit all-time highs, with the NYSE Arca Gold Miners Index closing at 1,856.98, driven by gold prices near $3,610.50 an ounce, up 35% year-to-date amid trade anxiety and Fed independence threats.

Treasury Secretary Scott Bessent indicated ongoing US-China talks on extending the tariff truce, with a possible 90-day addition under consideration, as Trump weighs decisions. Broadcom rose in premarket after announcing AI accelerator work with OpenAI, while Lululemon sank 18% on margin warnings from import rule changes.

Analysts from VanEck and Veritas highlighted gold miners’ strong margins and earnings growth, with Newmont up over 100% in earnings last year and Agnico Eagle favoured for execution. Despite the rally, the sector trades at a discount to the S&P 500. HSBC, Morgan Stanley, and UBS maintain bullish long-term views on equities, citing AI tailwinds and tariff clarity, though Goldman Sachs warns of potential hits from trade policies.

OVERVIEW OF THE AUSTRALIAN MARKET

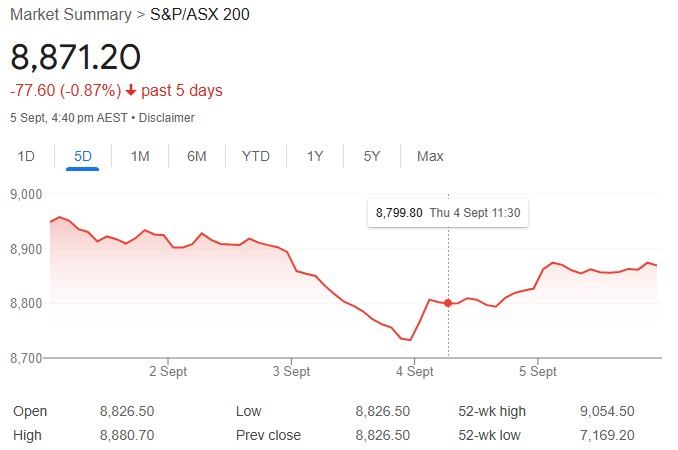

Australia’s share market closed higher on September 5, 2025, buoyed by gains in interest rate-sensitive sectors amid softer bond yields and a positive lead from overseas markets. The S&P/ASX 200 rose 0.51% to 8,871.2, while the broader All Ordinaries climbed 0.54% to 9,140.5. Real estate led the advance with a 1.37% gain, followed by consumer discretionary at 1.33% and information technology at 1.18%. Energy and consumer staples lagged, falling 0.28% and 0.31% respectively. For the week, the ASX 200 ended down 1.1%, reflecting post-earnings profit-taking and a mid-week sell-off tied to global bond market volatility.

Top performers included Peak Rare Earths, up 25.4% after an increased scheme consideration, and Gateway Mining, rising 21.2% in line with its uptrend. Other notable gainers were Vertex Minerals at 18.5% and 4DMedical at 17.9%, both continuing positive momentum from recent announcements. On the downside, Tamboran Resources dropped 8.3%, Chalice Mining fell 7.4%, and Native Mineral Resources declined 6.7%, with no specific news driving the moves.

Gold miners showed strength, with Ora Banda Mining up 9.6% and Catalyst Metals gaining 9.2%, amid broader sector gains as spot gold hovered near its all-time high. The financials sector added 0.47%, helping offset weakness in materials, which rose just 0.28% despite mixed performances from majors like BHP.

The Australian dollar strengthened 0.26% to 0.6535 against the US dollar, supported by a weaker greenback ahead of key US jobs data. Investors are eyeing the upcoming Reserve Bank of Australia meeting for clues on rate cuts, with recent data showing a Q2 GDP growth of 0.6% quarter-on-quarter, beating expectations, and a current account surplus narrower than forecast at -13.7 billion AUD.

Strategists at Capital.com noted mediocre earnings overall but highlighted resilience in tech and real estate, suggesting the pullback was overdue after recent highs. With trade tensions lingering and geopolitical risks from the Middle East and Ukraine, some see gold-related stocks as a hedge, though valuations remain stretched in parts of the market.