| Name | Price | Change | % Chg |

|---|---|---|---|

| Dow | 44,193.12 | 81.38 | 0.18% |

| S&P 500 | 6,345.06 | 45.87 | 0.73% |

| Nasdaq | 21,169.42 | 252.87 | 1.21% |

| VIX | 16.77 | -1.08 | -6.05% |

| Gold | 3,434.90 | 1.5 | 0.04% |

| Oil | 64.42 | 0.07 | 0.11% |

OVERVIEW OF THE US MARKET

Wall Street closed higher on August 6, 2025, as a tech-led rally offset concerns over trade uncertainties and mixed economic signals. The S&P 500 climbed 45.87 points, or 0.73%, to 6,345.06, driven by strong performances in technology and consumer discretionary sectors. The Nasdaq Composite surged 252.87 points, or 1.21%, to 21,169.42, buoyed by Apple’s 5.1% jump following reports of a $100 billion U.S. manufacturing pledge aimed at sidestepping potential tariffs. The Dow Jones Industrial Average rose modestly by 81.38 points, or 0.18%, to 44,193.12, reflecting cautious optimism amid tariff-related volatility.

Sector performance was mixed, with Consumer Discretionary (+2.51%) and Information Technology (+1.34%) leading gains, while Energy (-0.91%), Health Care (-1.52%), and Real Estate (-0.82%) lagged. Standout movers included Opendoor Technologies, which plummeted 24.60% on high volume, and Snap Inc., down 17.15% after reporting ad revenue challenges. Ainos Inc. soared 39.91%, driven by speculative trading. Investors shrugged off weaker-than-expected ISM Non-Manufacturing PMI data at 50.1 for July, below the Reuters poll of 51.5, focusing instead on robust corporate earnings and dip-buying opportunities.

President Trump’s tariff rhetoric, including a new 25% levy on Indian goods over Russian energy purchases, kept markets on edge. However, his announcement of potential peace talks with Russia and Ukraine next week lifted sentiment, signaling possible de-escalation of global tensions. Investors are closely watching tomorrow’s Initial Jobless Claims data, expected at 221,000 for the week of August 2, and the Federal Reserve’s next moves, with markets pricing in a 60% chance of a 25-basis-point rate cut in September.

OVERVIEW OF THE AUSTRALIAN MARKET

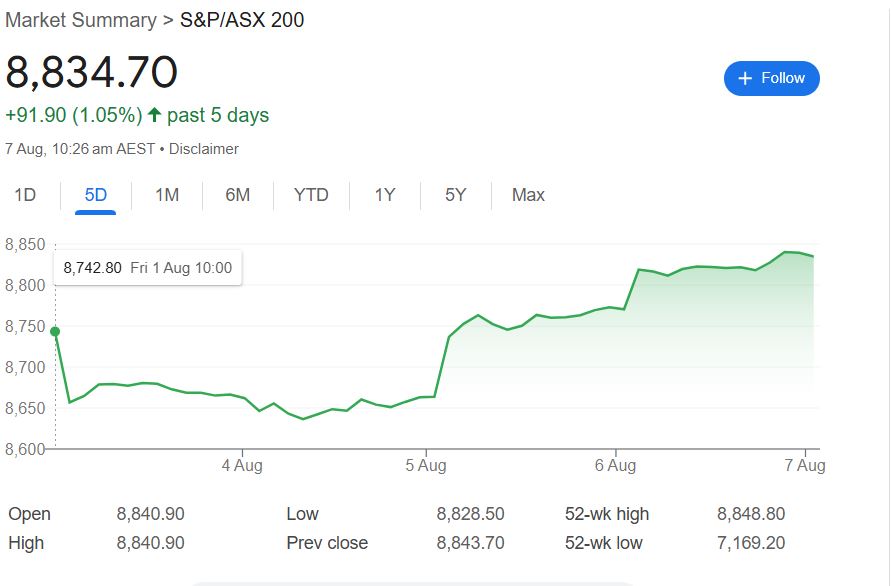

The Australian share market soared to new heights on August 6, 2025, with the S&P/ASX 200 index climbing 73.3 points, or 0.84%, to close at a record 8,843.7, just shy of its intraday peak of 8,848.8. The broader All Ordinaries index outperformed, gaining 82.3 points, or 0.91%, to a new high of 9,111.1. Market breadth was robust, with advancers outpacing decliners 223 to 56 in the S&P/ASX 300, marking a second consecutive day of strong momentum. Despite global uncertainties, including U.S. tariff threats and a lackluster U.S. services sector, Australian equities shrugged off concerns, buoyed by optimism around potential rate cuts and solid corporate earnings.

The Gold Sub-sector (XGD) led the charge, surging 3.3%, driven by gold prices holding near $US3,432 an ounce, supported by expectations of lower global interest rates. Resources (XJR, +1.2%) and Energy (XEJ, +1.3%) rebounded strongly, with iron ore prices hitting their highest since May and coal imports to Asia ticking up. Standout performers included Pinnacle Investments, which rallied 9.5% to $25.21 after a 50% jump in full-year net profit, and REA Group, up 6.9% on double-digit earnings growth. Large-cap miners like Fortescue (+1.3%) and Rio Tinto (+1.0%) also contributed, while Commonwealth Bank (+1.0%) anchored financials, which gained 0.8% despite lofty valuations.

Global headwinds, including U.S. President Donald Trump’s comments on CNBC’s Squawk Box about impending tariffs on semiconductors, pharmaceuticals, and India, failed to dent local sentiment. Investors instead focused on domestic strengths, such as Australia’s stable banking sector and resilient mining industry, positioning the market as a relative safe haven. The S&P Global Services PMI for Australia rose to 54.1 in July, signaling robust growth in the services sector, further boosting confidence. However, AMP’s Shane Oliver cautioned that high valuations could leave the market vulnerable if global risks materialize.